New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

introducing accounting

Introducing Accounting For AS 2nd Edition Ian Harrison - Solutions

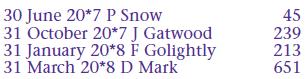

Darryl has discovered that the three debtors shown below are unable to settle their debts. He has therefore decided to write them off as bad debts in the year ended 31 December 20*8.RequiredPrepare the bad debts account for the year ended 31 December 20*8. Biff Treados Ltd Victor 451 159 52

Umberto has discovered that the debtors listed below are unable to clear their debts. He has decided to write them off as bad debts in the year ended 30 September 20*8.Required Prepare the bad debts account for the year ended 30 September 20*8. Ghuster plc Jamie Sally 1,436 39 392

Equipment costing £30,000 has been depreciated at 50% per annum using the reducing balance method. It was sold after three years of use for £3,700.RequiredPrepare a disposal account for the equipment.

Umair wishes to maintain a provision for doubtful debts in his general ledger.RequiredPrepare the provision for doubtful debts account for each year. Provision for doubtful debts Year 1 400 Year 2 420 Year 3 500

Sheila wishes to maintain a provision for doubtful debts in her ledger at 31 December.RequiredPrepare the provision for doubtful debts account for each year. Provision for doubtful debts 20*6 610 20*7 660 20*8 740

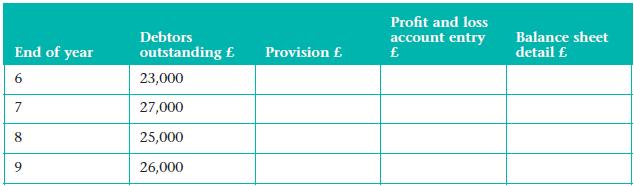

Mee has her financial year-end on 31 August. She provides the following information:In each year there have been a number of bad debts which have yet to be written off.Mee wishes to make provision for doubtful debts of 5% of debtors outstanding at each year-end (work to nearest whole

Robin has his financial year-end on 31 January. He provides the following information:■ £700 is to be written off as a bad debt in the year ended 31 January 20*6.■ £200 is to be written off as a bad debt in the year ended 31 January 20*8.■ Robin wishes to make provision for doubtful debts

Try to fill the spaces for the next four years:To summarise:■ The amount needed to increase the provision for doubtful debts is entered as an expense on the profit and loss account.■ The amount needed to decrease the provision for doubtful debts is entered as an ‘income’ on the profit and

Pat provides the following information from his sales ledger:All the debtors are bad and need to be written off.RequiredPrepare the bad debts account for Pat. Dr Balance b/d Dr Balance b/d Defius Ltd 154 Gordon 87 Cr Cr Dr Balance b/d Dr Balance b/d Ralph 345 Iain 620 Cr Cr

Doug informs you that there is no possibility of recovering any cash from the following outstanding debts:RequiredPrepare the bad debts account to record writing off the debts. Trish Glaster Ltd Rotrest Ltd Chiter and sons 435 455 113 712

A business has made a gross profit of £126,734 and a net profit of £64,211.Debtors amount to £32,967 before bad debts of £467 have been written off.A provision for doubtful debts of 4% is required.RequiredSelect the correct answer:The provision for doubtful debts is calculated as 4% of:A.

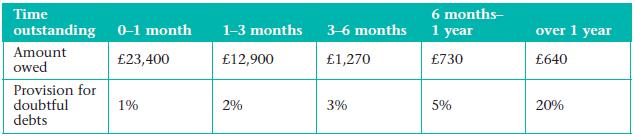

Willie uses an age profile of debtors to calculate his provision for doubtful debts.He provides the following information for the year ended 31 May 20*8, on which to base the calculation.Requireda) Calculate the provision for doubtful debts.b) Prepare a balance sheet extract showing how the

At 31 March 20*8 Morgan has debtors amounting to £40,000. She wishes to make a provision for doubtful debts of 2.5%.Requireda) Calculate the provision for doubtful debts.b) Prepare a balance sheet extract to show how the provision is treated.

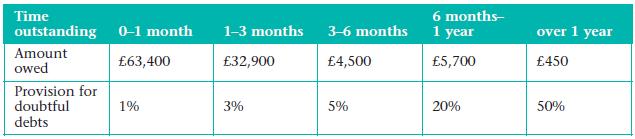

Hayton uses an age profile of debtors to calculate his provision for doubtful debts.He provides the following information for the year ended 31 October 20*8, on which to base the calculation.Requireda) Calculate the provision for doubtful debts.b) Prepare a balance sheet extract showing how the

Trudy McDuff maintains a provision for doubtful debts equal to 2.5% of outstanding debtors at the end of each financial year. The following information is available:The following bad debts have been written off during the year:RequiredPrepare the necessary general ledger accounts to record the

At 30 June 20*8 Kingsley has debtors amounting to £68,000. He wishes to make a provision for doubtful debts of 5%.Requireda) Calculate the provision for doubtful debts.b) Prepare a balance sheet extract to show how the provision is treated.

Maureen Gill maintains a provision for doubtful debts equal to 5% of outstanding debtors at the end of each financial year. The following information is available:Bad debts not yet written off at 31 December 20*8Requireda) Prepare the necessary general ledger accounts to record the entries. Show

Glad Thomson provides the following information for the year ended 31 October 20*8. She maintains a provision for doubtful debts of 5%, based on outstanding debtors at the end of each financial year.Bad debts not yet written off at 31 October 20*8During the year £246 was received from Broadbent.

Ryder provides the following information for the year ended 30 April 20*8. He maintains a provision for doubtful debts based on 2.5% of debtors outstanding at his financial year-end.Bad debts not yet written off at 30 April 20*8During the year £197 was received from Tickell. This amount had been

During the year a trader receives £288 from Geot Ltd. This amount had been written off as a bad debt some years previously.RequiredPrepare the ledger accounts necessary to record the recovery of the bad debt.

Jessie receives £761 from Prodo Ltd. Jessie had written the amount off as a bad debt some years ago.RequiredPrepare the ledger accounts necessary to record the recovery of the bad debt.

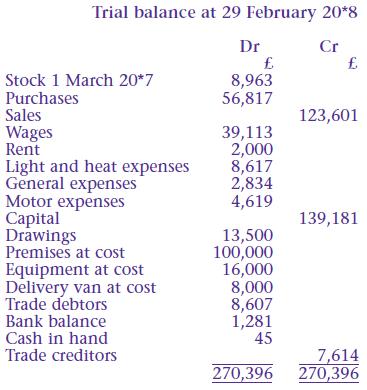

The following trial balance has been extracted from the books of Hanif Mohammed:Additional information at 29 February 20*8■ Stock was valued at £7,432.■ Rent owing £200.Requireda) Prepare a trading and profit and loss account for the year ended 29 February 20*8.b) Prepare a balance sheet at

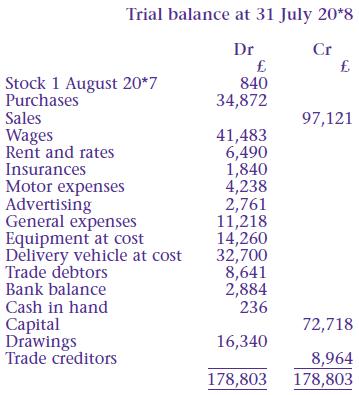

Siobhan Murgatroyd has extracted the following trial balance from her books of account:Additional information at 31 July 20*8■ Stock was valued at £1,166.■ Insurance paid in advance amounted to £315.Requireda) Prepare a trading and profit and loss account for the year ended 31 July 20*8.b)

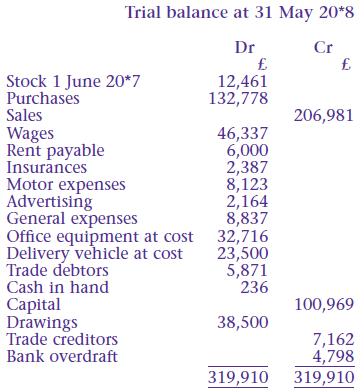

Hibo Ahmed has provided the following trial balance extracted from her books of account:Additional information at 31 May 20*8■ Stock was valued at £13,106.■ Wages owing £814.■ Insurance paid in advance £628.Requireda) Prepare a trading and profit and loss account for the year ended 31 May

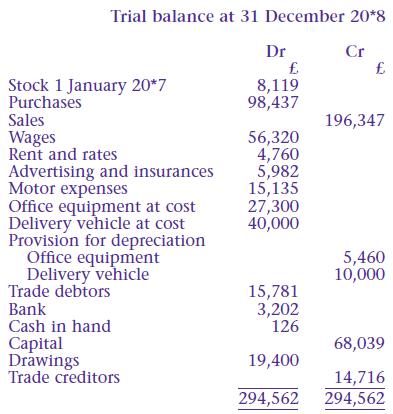

Helen Duff provides the following information:Additional information at 31 December 20*8■ Stock was valued at £9,003.■ Helen provides depreciation on office equipment at 10% per annum using the straight line method; she provides depreciation on her delivery vehicle at 25% per annum using the

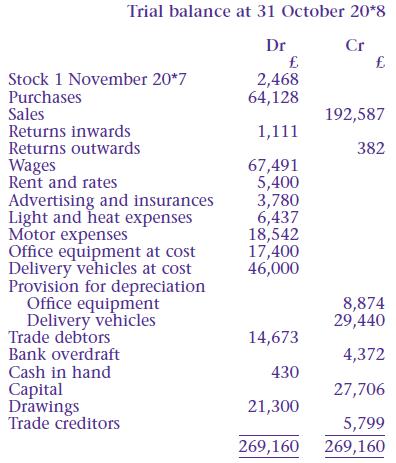

Lynn Parker provides the following information:Additional information at 31 October 20*8■ Stock was valued at £3,199.■ Lynn provides depreciation on all assets using the reducing balance method. The annual charges are: office equipment 20% (round up); delivery vehicles 40%.Requireda) Prepare a

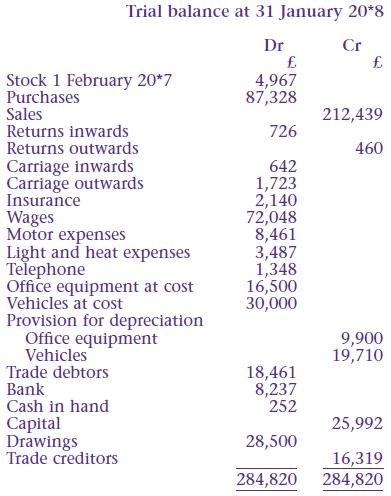

David Lycett provides the following information:Additional information at 31 January 20*8■ Stock was valued at £5,141.■ Wages owing £312.■ Light and heat expenses paid in advance £248.■ Depreciation on office equipment is calculated using the straight line method at 10% per annum.■

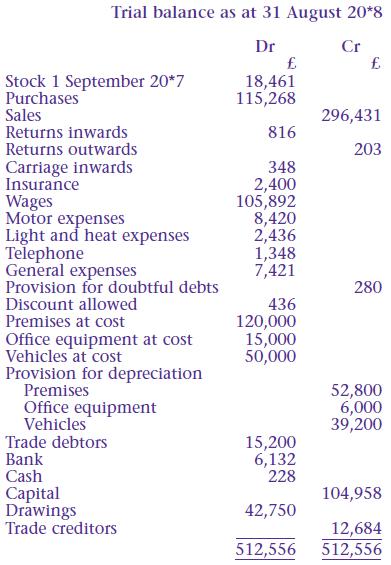

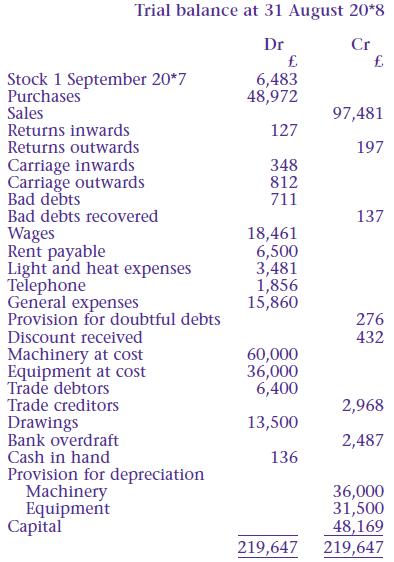

Gladys Jones provides the following information:Additional information at 31 August 20*8■ Stock was valued at £16,984.■ Insurance paid in advance £180.■ Telephone bill outstanding £351.■ Provision for doubtful debts to be maintained at 2% of debtors outstanding at the year-end.■

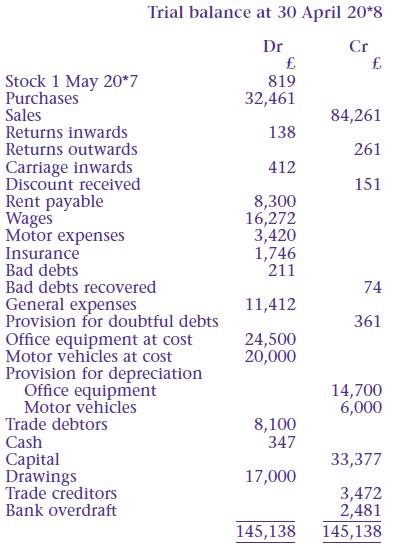

Tom Green provides the following information:Additional information at 30 April 20*8■ Stock was valued at £612.■ Motor expenses accrued amounted to £182.■ Insurance prepaid £132.■ Provision for doubtful debts is maintained at 5% of year-end debtors.■ Depreciation is provided at 10% on

Isadorah Boom provides the following information:Additional information at 31 August 20*8■ Stock was valued at £6,543.■ Wages owing amounted to £380.■ Rent paid in advance £500.■ Provision for doubtful debts is to be maintained at 5% of debtors outstanding at the year-end.■

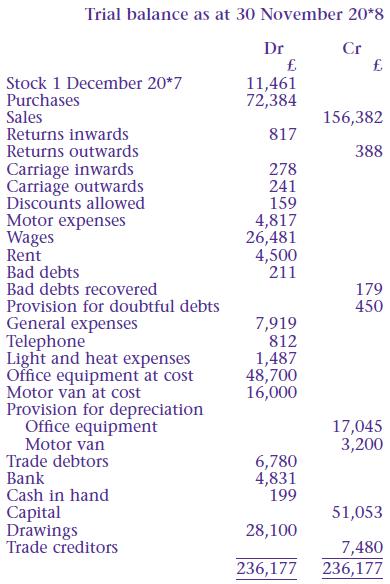

The following information is provided for Cindy Ash:Additional information at 30 November 20*8■ Stock was valued at £10,177.■ Motor expenses owing amounted to £130.■ Light and heat expenses had been prepaid £102.■ Cindy had withdrawn goods from the business for her private use

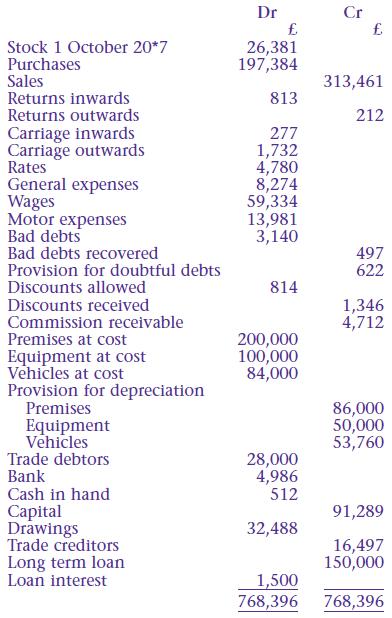

Jack Simms provides the following information:Additional information at 30 September 20*8■ Stock was valued at £27,492.■ Wages owing amounted to £853.■ Rates paid in advance £1,270.■ Jack had withdrawn goods from the business for personal use amounting to £2,500.■ Commission

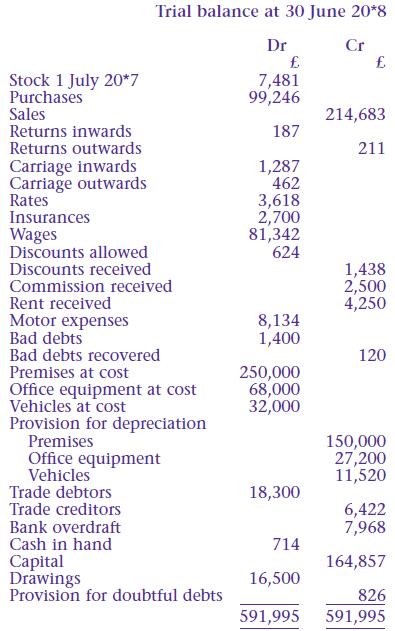

Annie Lim provides the following information:Additional information at 30 June 20*8■ Stock was valued at £9,284.■ Annie has taken goods from the business £1,750 for her personal use.■ Insurance prepaid £350.■ Motor expenses owing £299.■ Commission receivable owing to Annie £500.■

Sanaa Malik provides the following information relating to her business for the year ended 31 August 20*8:stock at 1 September 20*7 £13,579; stock at 31 August 20*8 £14,217; purchases £126,993; sales £203,741.Requireda) Prepare a trading account for the year ended 31 August 20*8 showing clearly

The business has just purchased a specialised piece of computerised manufacturing machinery for £240,000. It will be used for three years. It would certainly have no resale value because of its specialised nature. How should the machinery be valued? Name the accounting concept that will apply.■

Rent received for the year is £3,500. The tenant should have paid £4,000.The amount to be included in the profit and loss account is ………. . This is an example of using the ………………. concept.

Select the accounting concept to be used in the following circumstances:(a) Wages outstanding at the end of the financial year: £362.■ Accruals■ Consistency■ Materiality■ Going concern(b) A fixed asset costs £10,000. It is expected to have a life of 10 years with no residual

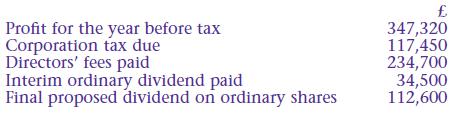

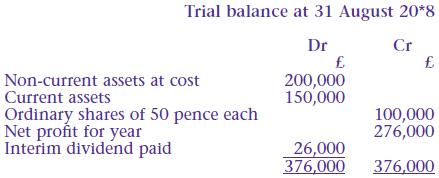

The following information relating to GraZeb Ltd for the year ended 31 March 20*8 is given:RequiredPrepare an extract from the income statement for the year ended 31 March 20*8. Profit for the year before tax Corporation tax due Directors' fees paid Interim ordinary dividend paid Final proposed

Accounting policies should be relevant, ……………….., comparable and understandable. (Fill the gap.)

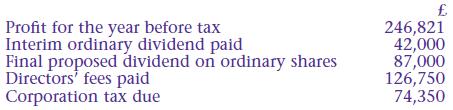

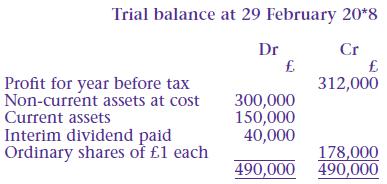

The information relating to Rutor Ltd for the year ended 31 December 20*8 is given:RequiredPrepare an extract from the income statement for the year ended 31 December 20*8. Profit for the year before tax Interim ordinary dividend paid Final proposed dividend on ordinary shares Directors' fees

Select the accounting concept to be used in the following circumstances:(a) Jim feels that the old ‘Olivetti’ typewriter valued at cost £47 on the balance sheet could fetch £350 at auction.■ Entity■ Objectivity■ Realisation■ Prudence(b) A new ‘Sellotape’ dispenser has been

The following information is given for Helaminge Ltd at 30 September 20*8:Authorised and issued share capital 800,000 ordinary shares of 25 pence each; premises at cost £80,000; machinery at cost £60,000; vehicle at cost £30,000; inventories £20,000; trade receivables £12,000; bank £6,000;

The summarised balance sheet of Duvase Ltd at 30 November 20*8 is shown.On 1 December 20*8 Duvase Ltd issued a further 200,000 ordinary shares at £1.60 per share.RequiredPrepare a summarised balance sheet at 1 December 20*8 as it would appear after the share issue has been completed. Non-current

The following information is given for Arbres Ltd at 30 April 20*8:Authorised share capital 500,000 ordinary shares of 50 pence each; issued share capital 300,000 ordinary shares 50 pence paid; machinery at cost £80,000; vehicle at cost £40,000; inventories £25,000; trade receivables £15,000;

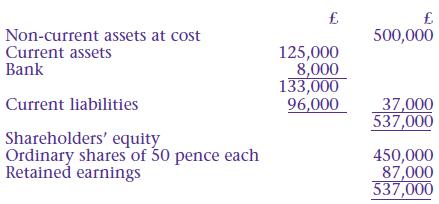

The summarised balance sheet of D Lilly Ltd at 31 March 20*8 is shown.On 1 April 20*8 D Lilly Ltd issued a further 400,000 ordinary shares at 80 pence per share.Immediately after the share issue the company purchased additional fixed assets of £300,000, paying by cheque.RequiredPrepare the balance

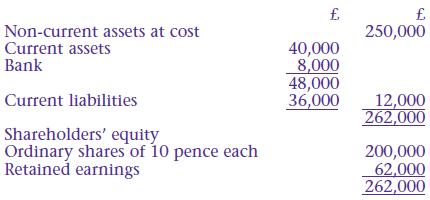

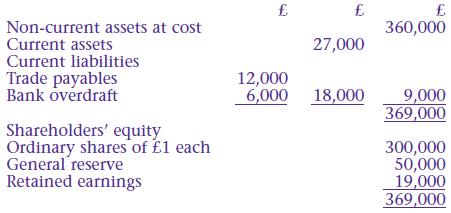

The summarised balance sheet of Ousby Ltd at 31 October 20*8 is given.The non-current assets were revalued at £400,000 on 1 November 20*8.RequiredPrepare the balance sheet of Ousby Ltd at 1 November 20*8 after the non-current assets were revalued. Non-current assets at cost Current

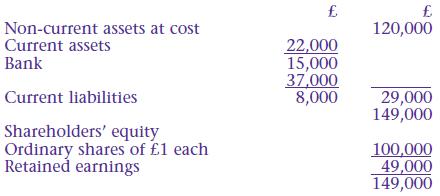

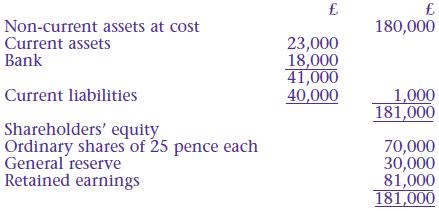

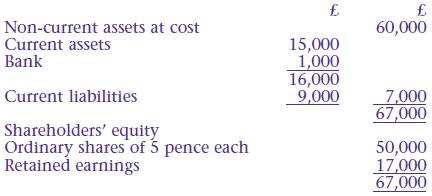

The summarised balance sheet of Graf Ltd at 29 February 20*8 is given.The non-current assets were revalued at £200,000 on 1 March 20*8.RequiredPrepare the balance sheet of Graf Ltd at 1 March 20*8 after the non-current assets were revalued. Non-current assets at cost Current assets Bank Current

Douglas Ltd supplies the following information after the first year of trading:Additional informationThe directors wish to transfer £50,000 to general reserve and recommend a final dividend of £60,000. They wish to provide for corporation tax due £82,000.Requireda) Prepare an extract from the

Donald Ltd provides the following information after the first year of trading:Additional informationThe directors wish to transfer £40,000 to general reserve and recommend a final dividend of £50,000. They wish to provide for corporation tax due £65,000.Requireda) Prepare an extract from the

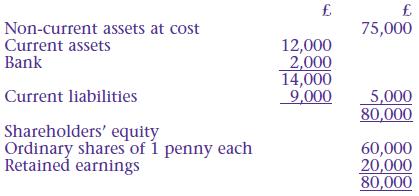

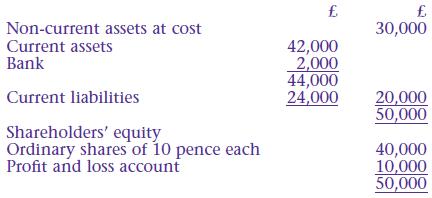

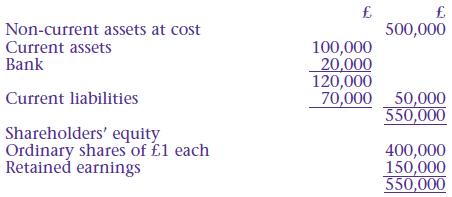

Hox Ltd provides the following summarised balance sheet at 31 May 20*8:The non-current assets were revalued at £300,000 on 1 June 20*8.RequiredPrepare a summarised balance sheet at 1 June 20*8 after revaluing the non-current assets. Non-current assets at cost Current assets Bank Current

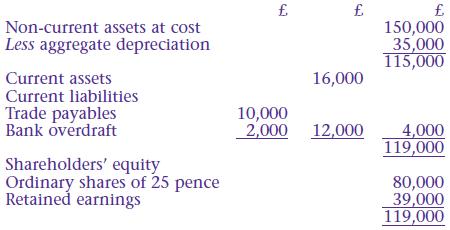

Wong Ltd provides the following summarised balance sheet at 31 December 20*8:The non-current assets were revalued on 1 January 20*9 at £210,000.RequiredPrepare a summarised balance sheet at 1 January 20*9 after revaluing the non-current assets. Non-current assets at cost Current

The summarised balance sheet of Norest Ltd at 31 January 20*8 is given.On 1 February 20*8 Norest Ltd issued a further 100,000 ordinary shares at a price of 30 pence per share.RequiredPrepare a summarised balance sheet at 1 February 20*8 after the new shares were issued. Non-current assets at

The summarised balance sheet of Trosh Ltd at 31 October 20*8 is given.On 1 November 20*8 Trosh Ltd issued a further 200,000 ordinary shares at £1.75 each.RequiredPrepare a summarised balance sheet at 1 November 20*8 after the new shares were issued. Non-current assets at cost Current

The summarised balance sheet of Smith-Patel Ltd at 31 March 20*8 is given.On 1 April 20*8 Smith-Patel Ltd issued a further 200,000 £1 ordinary shares at £1.50. On the same date the company revalued the non-current assets at £750,000.RequiredPrepare a summarised balance sheet at 1 April 20*8

The summarised balance sheet of Wiley-Fox Ltd at 30 November 20*8 is given.On 1 December 20*8 Wiley-Fox Ltd issued a further 100,000 ordinary shares at 40 pence per share. On the same date the company revalued the non-current assets at £200,000.RequiredPrepare a summarised balance sheet at 1

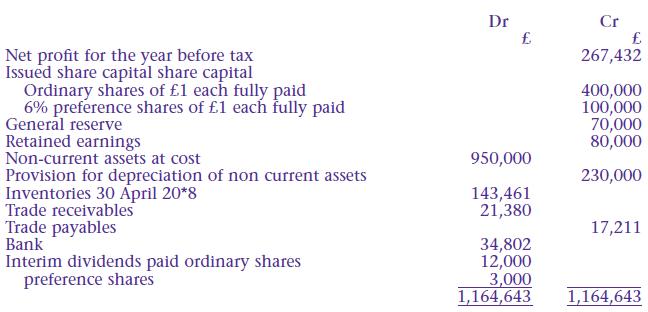

The following trial balance has been extracted from the books of Stephanie Hood Ltd on 30 April 20*8.Additional informationThe directors recommend:■ A transfer to general reserve £50,000■ A final ordinary dividend £26,000 be provided■ A final preference dividend be provided■ Provision for

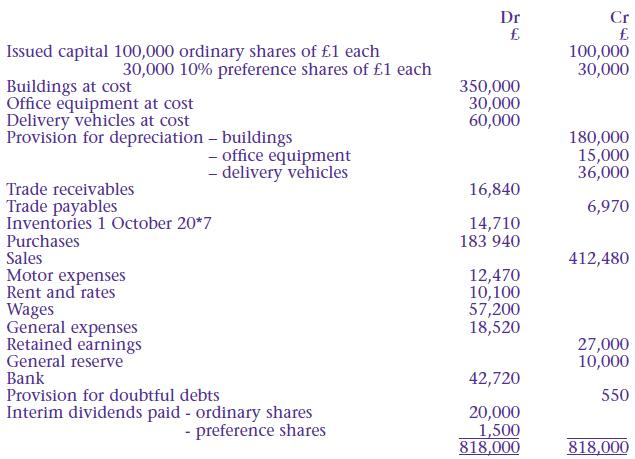

Pling Ltd has an authorised capital of 500,000 ordinary shares of £1 each and 250,000 10% preference shares of £1 each. The following trial balance has been extracted from the books of account at 30 September 20*8.Additional information at 30 September 20*8■ Inventories were valued at

The owner of a business is planning to include his premises as an asset in the end-of-year balance sheet at cost value of £200,000. However, the finance manager feels that this is too low a value and says that the premises should be included at £250,000, since this is what they could presently be

Outline one reason why accountants apply accounting concepts when preparing end-of-year financial statements.

Complete the following statements:■ Although the staff who work in a business are often regarded as one of its most valuable assets, they are not included in the business balance sheet. This is an example of the …………………….. concept.■ The petrol in the tank of the delivery van,

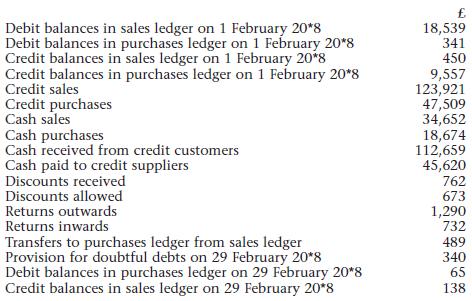

Ifor Jones supplies the following information for the month of February 20*8:Requireda) Prepare a sales ledger control account for the month of February 20*8.b) Prepare a purchases ledger control account for the month of February 20*8. Debit balances in sales ledger on 1 February 20*8 Debit

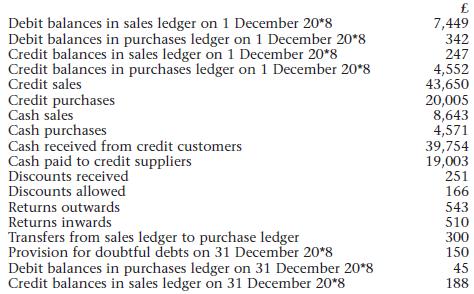

Rory McDuff supplies the following information for the month of December 20*8:Requireda) Prepare a sales ledger control account for the month of December 20*8.b) Prepare a purchases ledger control account for the month of December 20*8. Debit balances in sales ledger on 1 December 20*8 Debit

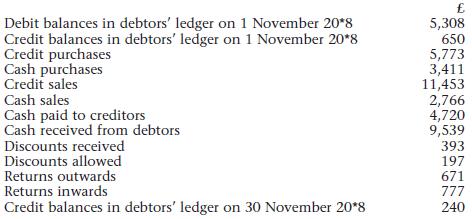

Melodie Clyde supplies the following information for November 20*8:RequiredPrepare a debtors’ ledger control account for the month of November 20*8. Debit balances in debtors' ledger on 1 November 20*8 Credit balances in debtors' ledger on 1 November 20*8 Credit purchases Cash purchases Credit

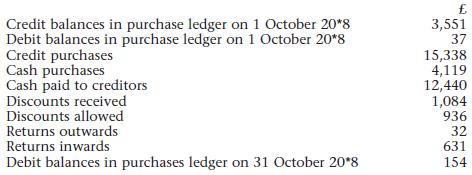

Xiu Jin supplies the following information for October 20*8:RequiredPrepare a purchases ledger control account for the month of October 20*8. Credit balances in purchase ledger on 1 October 20*8 Debit balances in purchase ledger on 1 October 20*8 Credit purchases Cash purchases Cash paid to

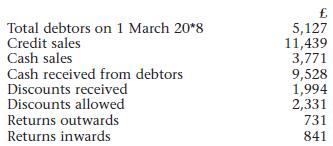

Dick Dresden supplies the following information for March 20*8:RequiredPrepare a debtors’ ledger control account for the month of March 20*8. Total debtors on 1 March 20*8 Credit sales Cash sales Cash received from debtors Discounts received Discounts allowed Returns outwards Returns

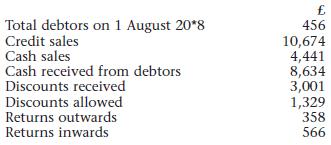

Claire Droy supplies the following information for August 20*8:RequiredPrepare a sales ledger control account for the month of August 20*8. Total debtors on 1 August 20*8 Credit sales Cash sales Cash received from debtors Discounts received Discounts allowed Returns outwards Returns

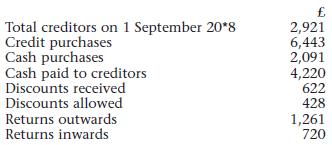

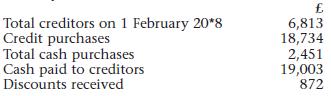

The following information is given for September 20*8 for Ted Brester:RequiredPrepare a purchases ledger control account for the month of September 20*8. Total creditors on 1 September 20*8 Credit purchases Cash purchases Cash paid to creditors Discounts received Discounts allowed Returns

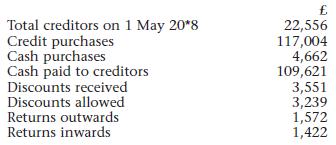

The following information is given for May 20*8 for Greg Trout:RequiredPrepare a purchases ledger control account for the month of May 20*8. Total creditors on 1 May 20*8 Credit purchases Cash purchases Cash paid to creditors Discounts received Discounts allowed Returns outwards Returns

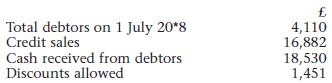

The following information relates to the debtors’ ledger of Martin Daley for the month of July 20*8:RequiredPrepare a debtors’ ledger control account for the month of July 20*8. Total debtors on 1 July 20*8 Credit sales Cash received from debtors Discounts allowed £ 4,110 16,882 18,530 1,451

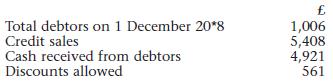

The following information relates to the sales ledger of Frew Niell for the month of December 20*8:RequiredPrepare a sales ledger control account for the month of December 20*8. Total debtors on 1 December 20*8 Credit sales Cash received from debtors Discounts allowed £ 1,006 5,408 4,921 561

The following information relates to the creditors’ ledger of Phillip Tyke for the month of February 20*8:RequiredPrepare a creditors’ ledger control account for the month of February 20*8. Total creditors on 1 February 20*8 Credit purchases Total cash purchases Cash paid to creditors Discounts

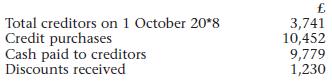

The following information relates to the purchase ledger of Tricia Clott for the month of October 20*8:RequiredPrepare a purchases ledger control account for the month of October 20*8. Total creditors on 1 October 20*8 Credit purchases Cash paid to creditors Discounts

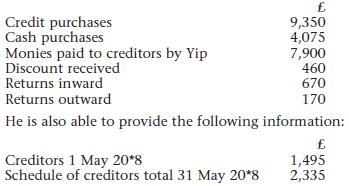

Yip provides the following information from his books of prime entry for May 20*8:Requireda) Prepare a purchase ledger control account for May 20*8.b) Explain what the control account reveals. Credit purchases Cash purchases Monies paid to creditors by Yip Discount

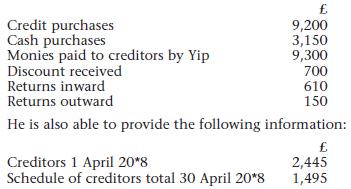

Yip provides the following information from his books of prime entry for April 20*8:RequiredPrepare a purchase ledger control account for the month of April 20*8. £ 9,200 3,150 9,300 700 610 150 Credit purchases Cash purchases Monies paid to creditors by Yip Discount received Returns

Petra provides the following information, which has been extracted from her books of prime entry on 31 August 20*8:The dishonoured cheque for £360 was originally part of the monies received and, because it has now been ‘returned’, should be entered on the debit side of the control

On 31 December 20*8 Tracy Beddow’s cash book showed a debit balance of £374.On the same date it was found that:■ Cheques amounting to £236 had not been presented at the bank for payment■ A direct debit for electricity £99 had not been entered in the cash book■ Bank overdraft interest

On 31 March 20*8 the cash book of Nancy Best showed a bank overdraft of £590.On the same date it was found that:■ Cheques amounting to £938 had not been presented at the bank for payment■ A standing order for loan interest £83 had not been entered in the cash book■ A direct debit for water

On 31 August 20*8 Bernard Drouin received his bank statement. It showed a credit balance of £210. The bank columns of his cash book showed a debit balance of £170.On the same date it was found that:■ A cheque paid into the bank account £109 had not been entered in the cash book■ A standing

On 30 April 20*8 Pat Nicholson received her bank statement. It showed a credit balance of £858.The bank columns of her cash book showed a debit balance of £180.On the same date it was found that:■ A cheque lodged in the bank £200 had not been entered in the cash book■ A cheque lodged in the

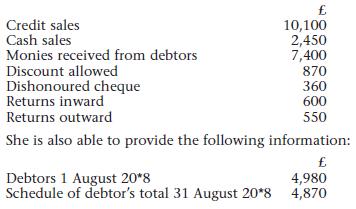

The bank columns of Matthew Carter are as follows:Required(a) Make any necessary adjustments to Matthew’s cash book.(b) Prepare a bank reconciliation statement at 31 October. Dr 1 Oct 3 Oct 7 Oct 15 Oct 31 Oct 31 Oct Balance b/d D Parker T Henley B Tain M Sand Balance c/d ANYTOWN BANK PLC Current

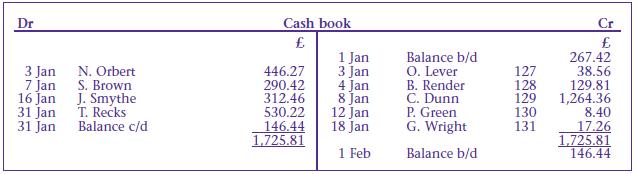

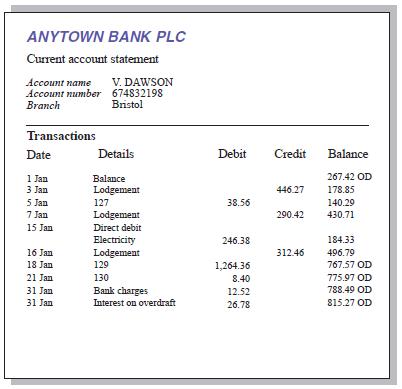

The bank columns of Vera Dawson’s cash book are as follows:Vera received her bank statement on 4 February.Make any adjustments to Vera Dawson’s cash book.Prepare a bank reconciliation statement at 31 January. Dr 3 Jan 7 Jan 16 Jan 31 Jan 31 Jan N. Orbert S. Brown J. Smythe T. Recks Balance

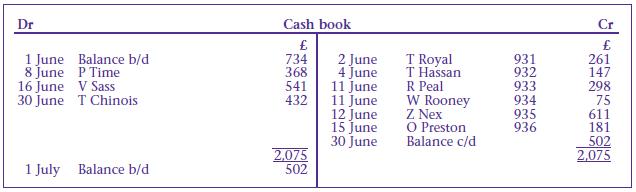

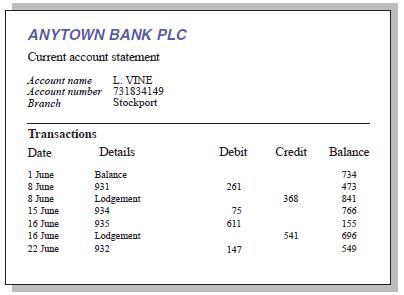

The bank columns of Leslie Vine’s cash book are as follows:Leslie received his bank statement on 4 July.Prepare a bank reconciliation statement at 30 June. Dr 1 June 8 June 16 June 30 June 1 July Balance b/d P Time V Sass T Chinois Balance b/d Cash book £ 734 368 541 432 2,075 502 2 June 4

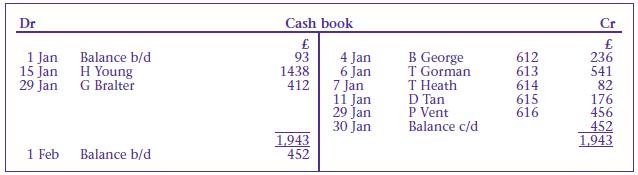

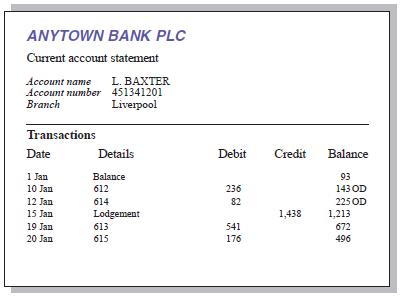

The bank columns of Lily Baxter’s cash book are as follows:Lily received her bank statement on 2 February,RequiredPrepare a bank reconciliation statement at 31 January. Dr 1 Jan 15 Jan 29 Jan 1 Feb Balance b/d H Young G Bralter Balance b/d Cash book £ 93 1438 412 1.943 452 4 Jan 6 Jan 7 Jan 11

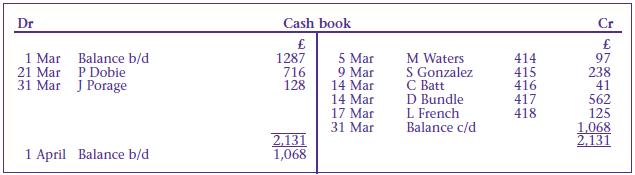

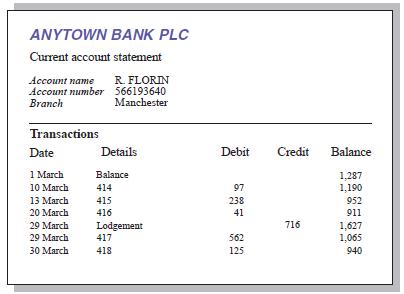

The bank columns of Rebecca Florin’s cash book are as follows:Rebecca received her bank statement on 2 April.RequiredPrepare a bank reconciliation statement at 31 March. Dr 1 Mar Balance b/d P Dobie 21 Mar 31 Mar J Porage 1 April Balance b/d Cash book 1287 716 128 2,131 1,068 5 Mar 9 Mar 14

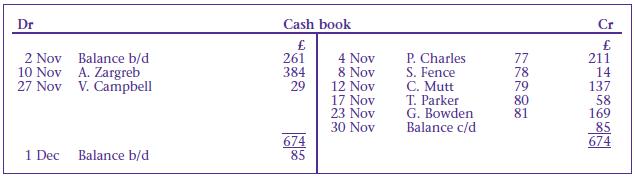

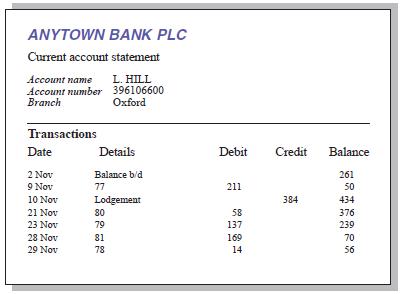

The bank columns of Lucy Hill’s cash book are as follows:Lucy received her bank statement on 4 December.RequiredPrepare a bank reconciliation statement at 30 November Dr 2 Nov Balance b/d 10 Nov A. Zargreb 27 Nov V. Campbell 1 Dec Balance b/d Cash book £ 261 384 29 674 85 4 Nov 8 Nov 12 Nov 17

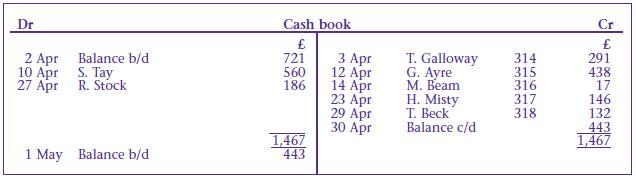

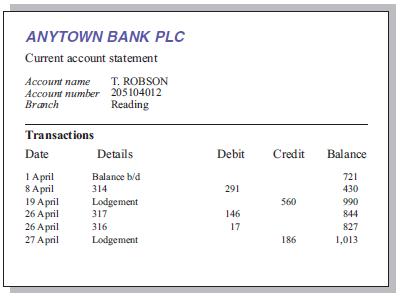

The bank columns of Tim Robson’s cash book are as follows:Tim Robson received his bank statement on 3 May.RequiredPrepare a bank reconciliation statement at 30 April. Dr 2 Apr 10 Apr 27 Apr Balance b/d S. Tay R. Stock 1 May Balance b/d Cash book 721 560 186 1,467 443 3 Apr 12 Apr 14 Apr 23 Apr 29

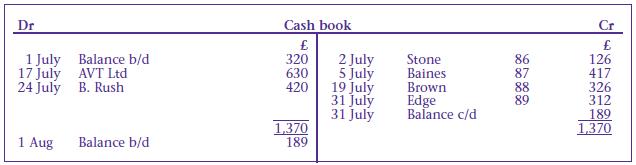

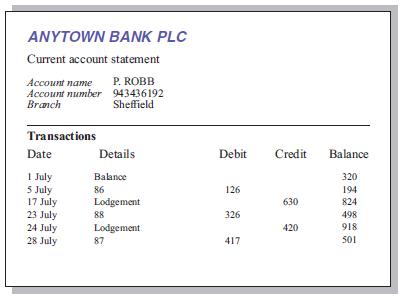

The bank columns of Philip Robb’s cash book are as follows:Philip receives his bank statement on 5 August:RequiredPrepare a bank reconciliation statement at 31 July. Dr 1 July 17 July 24 July 1 Aug Balance b/d AVT Ltd B. Rush Balance b/d Cash book £ 320 630 420 1,370 189 2 July 5 July 19 July 31

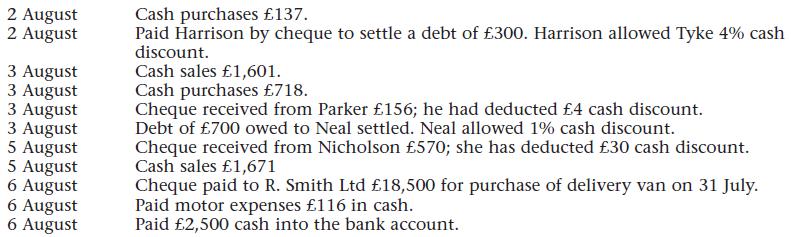

Bjorn Tyke had cash in hand £407 and a bank overdraft of £238 on 1 August.The following transactions took place during the first week in August:Requireda) Prepare Bjorn’s cash book for the period 1 August to 7 August.b) The entries in the cash book to the appropriate ledger accounts. 2 August 2

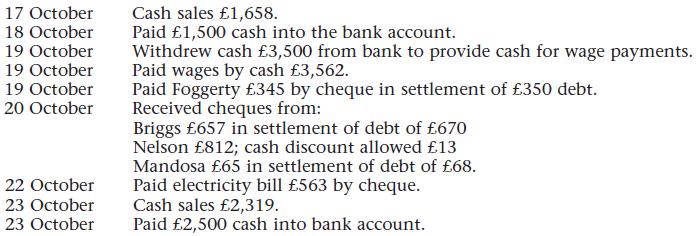

Arthur Mow had cash in hand £237 and a bank overdraft of £2,875 on 16 October.The following transactions took place the following week:Requireda) Prepare Arthur’s cash book for the week ended 23 October.b) Post the entries in the cash book to the appropriate ledger accounts. 17 October 18

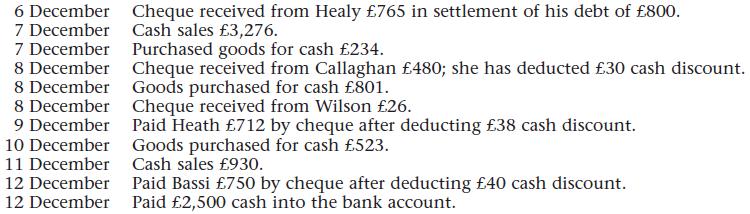

Roy Becker had cash in hand £281 and a balance at bank £834 on 6 December.The following transactions took place in December:Requireda) Prepare Roy’s cash book for the period 6 December to 12 December.b) Post the entries in the cash book to the appropriate ledger accounts. 6 December 7

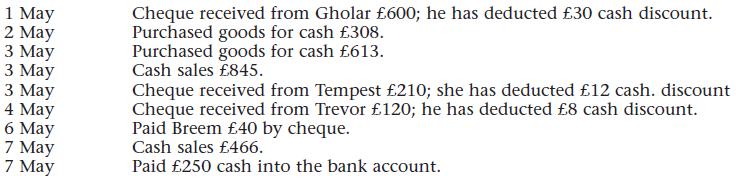

Sven David had cash in hand £88 and a balance at bank £376 on 1 May.The following transactions took place during May:Requireda) Prepare Sven’s cash book for the period 1 May to 7 May.b) Post the entries in the cash book to the appropriate ledger accounts. 1 May 2 May 3 May 3 May 3 May 4 May 6

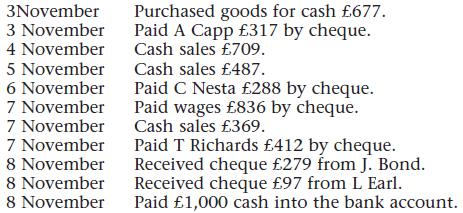

B Branden had cash in hand £861 and a balance at bank £1,307 at 1 November. The following transactions took place during November:Requireda) Prepare Branden’s cash book for the period 1 November to 8 November.b) Post the entries in the cash book to the appropriate ledger accounts. 3November 3

Tom Cunningham had cash in hand £217 and a balance at bank £1,132 at 1 February. The following transactions took place during February:Requireda) Prepare Tom’s cash book for the period 1 February to 5 February.b) Post the entries in the cash book to the appropriate ledger accounts. 1 February 1

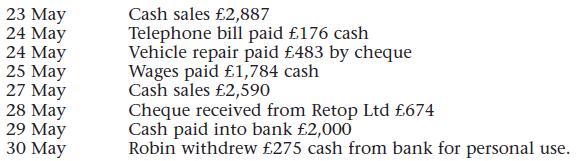

The following transactions relate to the business of Robin:Requireda) Enter the transactions in the cash book.b) Balance the cash book on 30 May. 23 May 24 May 24 May 25 May 27 May 28 May 29 May 30 May Cash sales £2,887 Telephone bill paid £176 cash Vehicle repair paid £483 by cheque Wages paid

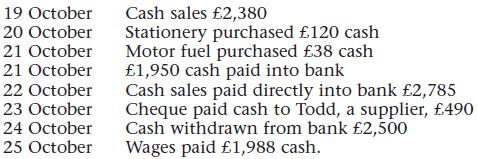

The following transactions relate to the business of York:Requireda) Enter the transactions in the cash book.b) Balance the cash book on 25 October. 19 October 20 October 21 October 21 October 22 October 23 October 24 October 25 October Cash sales £2,380 Stationery purchased £120 cash Motor fuel

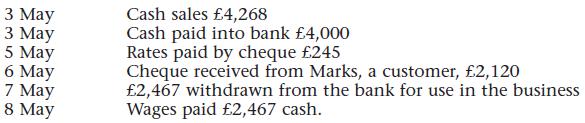

The following transaction relate to the business of Dublin:Requireda) Enter the transactions in the cash book.b) Balance the cash book on 8 May. 3 May 3 May 5 May 6 May 7 May 8 May Cash sales £4,268 Cash paid into bank £4,000 Rates paid by cheque £245 Cheque received from Marks, a customer,

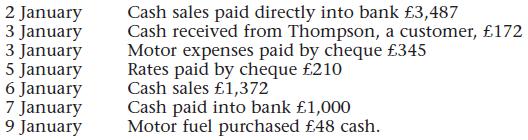

The following transactions relate to the business of Golightly:Requireda) Enter the transactions in the cash book.b) Balance the cash book on 9 January. 2 January 3 January 3 January 5 January 6 January 7 January 9 January Cash sales paid directly into bank £3,487 Cash received from Thompson, a

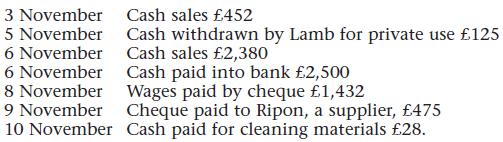

The following transactions relate to the business of Lamb:Requireda) Enter the transactions in the cash book.b) Balance the cash book on 10 November. 3 November 5 November 6 November 6 November 8 November 9 November 10 November Cash sales £452 Cash withdrawn by Lamb for private use £125 Cash

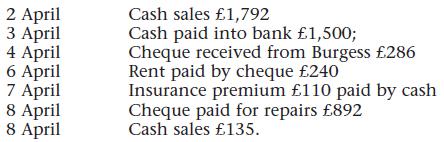

The following transactions relate to the business of Hunter:Requireda) Enter the transactions into the cash book.b) Balance the cash book on 8 April. 2 April 3 April 4 April 6 April 7 April 8 April 8 April Cash sales £1,792 Cash paid into bank £1,500; Cheque received from Burgess £286 Rent paid

The following transactions relate to the business of Silver:Requireda) Enter the transactions in the cash book.b) Balance the cash book on 9 October. 3 October 4 October 7 October 8 October 8 October 8 October 9 October Cheque received £540 from Benedict Cash sales £469 Cash received £591 from

Showing 300 - 400

of 535

1

2

3

4

5

6

Step by Step Answers