New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

managerial accounting

Cornerstones of Managerial Accounting 3rd Edition Mowen, Hansen, Heitger - Solutions

In activity-based budgeting, flexible budget formulas are created a. using only unit-level drivers. b. using only nonunit-level drivers. c. using both unit-level and nonunit-level drivers. d. using only direct labor hours. e. all of the

Activity flexible budgeting makes it possible to a. predict what activity costs will be as activity output changes. b. improve traditional budgetary performance reporting. c. enhance the ability to manage activities. d. all of the above.

In activity-based budgeting, costs are classified as variable or fixed with respect to a. the activity driver. b. only the units produced. c. only the units sold. d. only the direct labor hours. e. none of the above.

Responsibility for the volume variance usually is assigned to a. the purchasing department. b. the receiving department. c. the shipping department. d. the manufacturing department. e. none of the above.

An unfavorable volume variance can occur because a. too much finished goods inventory was held. b. the company overproduced. c. the actual output was less than expected or practical capacity. d. the actual output was greater than expected or practical

Because of the nature of fixed overhead items, the difference between the actual fixed overhead cost and the budgeted fixed overhead is a. likely to be small. b. likely to be large. c. usually a major concern. d. often attributable to labor

The total fixed overhead variance can be expressed as the sum of a. the spending and efficiency variances. b. the spending and volume variances. c. the efficiency and volume variances. d. the flexible budget and the volume variances. e.

The total fixed overhead variance is a. the difference between actual and budgeted fixed overhead costs. b. the difference between budgeted and applied fixed overhead costs. c. the difference between budgeted fixed and variable overhead costs. d. the

In a performance report that details the spending and efficiency variances,which of the following columns will be found? a. A cost formula for each item b. A budget for actual hours for each item c. A budget of standard hours for each item d. All of

The total variable overhead variance can be expressed as the sum of a. the underapplied variable overhead and the spending variance. b. the efficiency variance and the overapplied variable overhead. c. the spending and efficiency variances. d. the

Because the calculation of both variances is based on direct labor hours, an unfavorable labor efficiency variance implies that a. the variable overhead efficiency variance will also be unfavorable. b. the variable overhead efficiency variance will be favorable. c.

A variable overhead spending variance can occur because a. prices for individual overhead items have increased. b. prices for individual overhead items have decreased. c. more of an individual overhead item was used than expected. d. less of an

The total variable overhead variance is the difference between a. the budgeted variable overhead and the actual variable overhead. b. the actual variable overhead and the applied variable overhead. c. the budgeted variable overhead and the applied variable

A firm comparing the actual variable costs of producing 10,000 units with the total variable costs of a static budget based on 9,000 units would probably see a. no variances. b. small favorable variances. c. small unfavorable variances. d. large

To help assess performance, managers should use a. a static budget. b. a master budget. c. an after-the-fact flexible budget. d. a before-the-fact flexible budget. e. none of the above.

To help deal with uncertainty, managers should use a. a static budget. b. a master budget. c. an after-the-fact flexible budget. d. a before-the-fact flexible budget. e. none of the above.

To create a meaningful performance report, actual costs and expected costs should be compared a. at the budgeted level of activity. b. weekly. c. at the actual level of activity. d. at the average level of activity. e. hourly.

For performance reporting, it is best to compare actual costs with budgeted costs using a. flexible budgets. b. static budgets. c. master budgets. d. short-term budgets. e. none of the above.

Pat James, the purchasing agent for a local plant of the Oakden Electronics Division, was considering the possible purchase of a component from a new supplier. The component’s purchase price, $0.90, compared favorably with the standard price of $1.10. Given the quantity that would be purchased,

Goodsmell Company produces a well-known cologne. The standard manufacturing cost of the cologne is described by the following standard cost sheet:Management has decided to investigate only those variances that exceed the lesser of 10 percent of the standard cost for each category or $20,000.

The maternity wing of the city hospital has two types of patients: normal and cesarean. The standard quantities of labor and materials per delivery for 2009 are:The standard price paid per pound of direct materials is $10. The standard rate for labor is $16. Overhead is applied on the basis of

Refer to the data provided in Exercise 10-35.Required: 1. Prepare a journal entry for the purchase of raw materials. 2. Prepare a journal entry for the issuance of raw materials. 3. Prepare a journal entry for the addition of labor to Work in Process. 4.

Refer to the data provided in Exercise 10-28.Required:Break down the total variance for materials into a price variance and a usage variance using the columnar and formula approaches.Data From Exercise 10-28:Bolsa Corporation produces high-quality leather belts. The company uses a standard cost

(Appendix) Which of the following is true concerning significantly large labor variances? a. They are prorated among Work in Process, Finished Goods, and Cost of Goods Sold. b. They are closed to Cost of Goods Sold. c. They are prorated among Materials, Work in

Which of the following items describes practices surrounding the recording of variances? a. All inventories are typically carried at standard. b. Unfavorable variances appear as debits. c. Favorable variances appear as credits. d. Immaterial variances

Responsibility for the labor efficiency variance typically is assigned to a. labor unions. b. personnel. c. production. d. engineering. e. outside trainers.

Responsibility for the labor rate variance typically is assigned to a. labor unions. b. labor markets. c. personnel. d. production. e. engineering.

Responsibility for the materials usage variance is usually assigned to a. production. b. marketing. c. purchasing. d. personnel. e. the CEO.

The materials price variance is usually computed a. when materials are purchased. b. when materials are issued to production. c. when goods are finished. d. after suppliers are paid. e. None of the above.

Responsibility for the materials price variance typically belongs to a. production. b. marketing. c. purchasing. d. personnel. e. the chief executive officer (CEO).

Investigating variances from standard is a. always done. b. done if the variance is outside of an acceptable range. c. not done if the variance is expected to recur. d. done if the variance is less than 10 percent of standard cost. e. none

The total (budget) variance is given by the equation a. (AP × AQ) - (SP × SQ)P. b. (SP × AQ) - (AP × SQ)P. c. (SP × AQ) - (SP × SQ)P. d. (AP × SP) - (AQ × SQ)P. e. None of the above.

The standard direct labor hours allowed is given by the equation a. Unit labor standard × Normal output. b. Unit labor standard × Practical output. c. Unit labor standard × Standard output. d. Unit labor standard × Actual output. e.

The standard quantity of materials allowed is computed by the equation a. Unit quantity standard × Standard output. b. Unit quantity standard × Actual output. c. Unit quantity standard × Practical output. d. Unit quantity standard × Normal

The underlying details for the standard cost per unit are provided in a. the balance sheet. b. the standard production budget. c. the standard cost sheet. d. the standard work-in-process account. e. None of the above.

Standard costs are developed for a. direct materials. b. direct labor. c. variable overhead. d. fixed overhead. e. All of the above.

Reasons for adopting a standard cost system include a. to enhance operational control. b. to imitate most other firms. c. to encourage purchasing managers to purchase cheap materials. d. that the weighted average method can be used for process

An ideal standard is one that a. relies on maximum efficiency. b. uses only historical experience. c. can be achieved under efficient operating conditions. d. makes allowances for normal breakdowns, interruptions, less than perfect skill, and so

A currently attainable standard is one that a. relies on maximum efficiency. b. uses only historical experience. c. can be achieved under efficient operating conditions. d. is based on ideal operating conditions. e. None of the above.

The standard cost per unit of output for a particular input is calculated using the equation a. Actual input price per unit × Actual input used per unit. b. Standard input price × Inputs allowed for the actual output. c. Standard input price × Actual

Standards set by engineering studies a. can determine the most efficient way of operating. b. can provide rigorous guidelines. c. may not be achievable by operating personnel. d. often do not allow operating personnel to have much input.

Historical experience should be used with caution in setting standards because a. most companies keep poor records. b. ideal standards are always better than historical standards. c. they may not be achievable by operating personnel. d. they may

In a similar sense as companies, the U.S. government must prepare a budget each year. However, unlike private, for-profit companies, the budget and its details are available to the public. The entire budgetary process is established by law. The government makes available a considerable amount of

Which of the following items is not a possible example of myopic behavior? a. Promotion of deserving employees b. Reducing expenditures on preventive maintenance c. Cutting back on new product development d. Laying off top sales personnel so that

Which of the following is not an advantage of participative budgeting? a. It fosters a sense of creativity in managers. b. It encourages budgetary slack. c. It fosters a sense of responsibility. d. It encourages greater goal congruence. e.

Some key budgetary features that tend to promote positive managerial behavior are a. frequent feedback on performance. b. participative budgeting. c. realistic standards. d. well-designed monetary and nonmonetary incentives. e. all of the

An ideal budgetary system is one that a. encourages dysfunctional behavior. b. encourages myopic behavior. c. encourages goal-congruent behavior. d. encourages subversion of an organization’s goals. e. does none of the above.

The percentage of accounts receivable uncollectible can be ignored for cash budgeting because a. for most companies, it is not a material amount. b. it is included in cash sales. c. it appears on the budgeted income statement. d. no cash is received

Assume that a company has the following accounts receivable collection pattern: Month of sale 40% Month following sale 60%All sales are on credit.

The cash budget serves which of the following purposes? a. Documents the need for liberal inventory policies b. Provides information about the ability to repay loans c. Reveals the amount lost due to uncollectible accounts d. Reveals the amount of

Select the one budget below that is not a financial budget. a. The cost of goods sold budget b. The cash budget c. The budgeted balance sheet d. The capital expenditures budget e. None of the above

Which of the following is needed to prepare a budgeted income statement? a. The production budget b. The budgeted balance sheet c. Budgeted selling and administrative expenses d. The capital expenditures budget e. None of the above

A company plans on selling 200 units. The selling price per unit is $12. There are 20 units in beginning inventory, and the company would like to have 50 units in ending inventory. How many units should be produced for the coming period? a. 250 b. 200 c.

A company requires 100 pounds of plastic to meet the production needs of a small toy. It currently has 10 pounds of plastic inventory. The desired ending inventory of plastic is 30 pounds. How many pounds of plastic should be budgeted for purchasing during the coming period? a. 100

Which of the following is needed to prepare the production budget? a. Direct materials needed for production b. Expected unit sales c. Direct labor needed for production d. Units of materials in ending inventory e. None of the above

The first step in preparing the sales budget is to a. talk with past customers. b. review the production budget carefully. c. assess the desired ending inventory of finished goods. d. prepare a sales forecast. e. increase sales beyond the

Before a direct materials purchases budget can be prepared, you should first a. prepare a sales budget. b. prepare a production budget. c. decide on the desired ending inventory of materials. d. obtain the expected price of each type of

Which of the following is not part of the operating budget? a. The capital budget b. The cost of goods sold budget c. The production budget d. The direct labor budget e. The selling and administrative expenses budget

A moving, 12-month budget that is updated monthly is a. a waste of time and effort. b. a continuous budget. c. a master budget. d. not used by industrial firms. e. always used by firms that prepare a master budget.

The budget committee a. reviews the budget. b. resolves differences that arise as the budget is prepared. c. approves the final budget. d. is directed (typically) by the controller. e. does all of the above.

Which of the following is not an advantage of budgeting? a. It forces managers to plan. b. It provides information for decision making. c. It guarantees an improvement in organizational efficiency. d. It provides a standard for performance

Which of the following is not part of the control process? a. Monitoring of actual activity b. Comparison of actual with planned activity c. Investigating d. Developing a strategic plan e. Taking corrective action

A budget a. is a long-term plan. b. covers at least two years. c. is only a control tool. d. is necessary only for large firms. e. is a short-term financial plan.

Refer to the information in Multiple-Choice Exercise 8-10. What is the total inventory-related cost at the EOQ? (HINT: Round the number of setups to the nearest whole number.) a. 3,030 b. 1,500 c. 3,400 d. 2,985 e. 5,000

Refer to the information in Multiple-Choice Exercise 8-10. The economic order quantity (EOQ) for Product C is a. 500. b. 600. c. 700. d. 800. e. 1,000.

Shulman Company produces a number of products and provides the following information: Annual demand for Product C 20,000 Cost of setting up to make

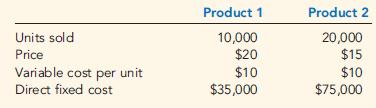

Albert Company provided the following information:Common fixed cost totaled $46,000. Albert allocates common fixed cost to product 1 and product 2 on the basis of sales. If product 2 is dropped, which of the following is true? a. Sales will increase by $300,000. b. Overall

Many companies use absorption costing because it a. accords with GAAP. b. is most useful for management decision making. c. provides the contribution margin. d. provides the segment margin. e. None of the above.

A segment could be which of the following? a. Product b. Customer type c. Geographic region d. All of the above e. None of the above

Suppose that a material has a lead time of three days and that the average usage of the material is 12 units per day. The maximum usage is 15 units per day. What is the safety stock? a. 3 b. 9 c. 12 d. 15 e. 5

Suppose that a material has a lead time of three days and that the average usage of the material is 12 units per day. What is the reorder point? a. 12 b. 15 c. 36 d. 45 e. 3

Which of the following is a reason for carrying inventory? a. To balance setup and carrying costs b. To satisfy customer demand c. To avoid shutting down manufacturing facilities d. To take advantage of discounts e. All of the above

The EOQ for Part B-22 is 2,500 units, and four orders are placed each year. The total annual ordering cost is $1,200.Which of the following is true? a. The total carrying cost is $1,200. b. The annual demand for the part is 2,500 units. c. The cost of placing one

In a segmented income statement, which of the following statements is true? a. Segment margin is greater than contribution margin. b. Common fixed expenses must be allocated to each segment. c. Contribution margin is equal to sales less all variable and direct

A company shows the following unit costs for its product: Direct materials $40 Direct labor 30

What are value-added activities? Value-added costs?

What is activity-based product costing?

Dykes, Inc. has the following two activities: (1) Retesting reworked products, cost: $160,000. The retesting cost of the most efficient competitor is $50,000. (2) Welding subassemblies, cost: $300,000 (15,000 welding hours). A benchmarking study reveals that the most efficient level for Dykes would

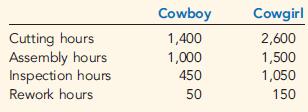

Refer to Cornerstone Exercise 7-29. The following activity data have been collected: Cutting $60,000 Assembling

An example of an environmental prevention cost is a. restoring land to its natural state. b. developing environmental management systems. c. licensing facilities for producing contaminants. d. auditing environmental activities. e. treating

An example of a societal cost is a. maintaining pollution equipment. b. recycling scrap. c. disposing of toxic materials. d. medical care due to polluted air. e. all of the above.

An example of an environmental internal failure cost is a. cleaning up oil spills. b. damaging ecosystems from solid waste disposal. c. verifying supplier environmental performance. d. measuring levels of contamination. e. none of the

Which of the following represents environmental detection costs? a. Developing environmental performance measures b. Recycling products c. Disposing of toxic materials d. Carrying out contamination tests e. None of the above

Which of the following is an external failure cost (quality)? a. Lost market share b. Retesting c. Rework d. Design reviews e. All of the above

Which of the following is an internal failure cost (quality)? a. Supplier evaluation and selection b. Scrapped units c. Packaging inspection d. Product liability e. Complaint adjustment

Which of the following is an appraisal cost (quality)? a. Design reviews b. Quality reporting c. Manager of an inspection team d. Warranties e. Retesting

Which of the following is a quality prevention cost? a. Quality planning b. Supplier evaluation and selection c. Quality audits d. Field trials e. All of the above

Striving to produce the same activity output with lower costs for the inputused is concerned with which of the following dimensions of activity performance? a. Quality b. Time c. Activity sharing d. Efficiency e. Effectiveness

Thom Company produces 100 units in 5 hours. The velocity for Thom a. is 20 units per hour. b. is 5 hours per unit. c. is 3 minutes per unit. d. is 1 hour per 20 units. e. cannot be calculated.

Thom Company produces 100 units in 5 hours. The cycle time for Thom a. is 20 units per hour. b. is 5 hours per unit. c. is 3 minutes per unit. d. is 1 hour per 20 units. e. cannot be calculated.

The cost of inspecting incoming parts is most likely to be reduced by a. activity sharing. b. activity selection. c. activity reduction. d. activity elimination. e. none of the above.

Suppose that a company is spending $50,000 per year for inspecting, $40,000 for purchasing, and $60,000 for reworking products. A good estimate of nonvalue-added costs would be a. $110,000. b. $50,000. c. $60,000. d. $90,000. e. $100,000.

Which of the following are nonvalue-added activities? a. Moving goods b. Storing goods c. Inspecting finished goods d. Reworking a defective product e. All of the above

A forklift and its driver used for moving materials are examples of a. activity outputs. b. activity output measures. c. resource drivers. d. activity inputs. e. root causes.

Lambert Company has two suppliers: Deming and Leming. The cost of warranty work due to defective components is $2,000,000. The total units repaired under warranty average 100,000, of which 90,000 have components from Deming and 10,000 have components from Leming. Select the items below that

This year, Lambert Company will ship 1,500,000 pounds of goods to customers at a cost of $1,200,000. If a customer orders 10,000 pounds an produces $200,000 of revenue (total revenue is $20 million), the amount of shipping cost assigned to the customer by using ABC would be a. cannot be

Which of the following is a true statement about activity-based supplier costing? a. The cost of a supplier is the purchase price of the components or materials acquired. b. Suppliers can affect many internal activities of a firm and significantly increase the cost of

Which of the following is a true statement about activity-based customer costing? a. Customer diversity requires multiple drivers to trace costs accurately to customers. b. Customers can consume customer-driven activities in different proportions. c. It often

Assume that the moving activity has an expected cost of $80,000. Expected direct labor hours are 20,000, and expected number of moves is 40,000. The best activity rate for moving is a. $4 per move. b. $1.33 per hour-move. c. $4 per hour. d. $2 per

The receiving department employs one worker, who spends 75 percent of his time on the receiving activity and 25 percent of his time on inspecting products. His salary is $40,000. The amount of cost assigned to the receiving activity is a. $34,000. b. $40,000. c.

Showing 4000 - 4100

of 5971

First

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

Last

Step by Step Answers