New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

managerial accounting

Cornerstones of Managerial Accounting 3rd Edition Mowen, Hansen, Heitger - Solutions

Interview questions are asked to determine a. what activities are being performed. b. who performs the activities. c. the relative amount of time spent on each activity by individual workers. d. possible activity drivers for assigning costs to

The second stage of ABC entails the assignment of a. resource costs to departments. b. activity costs to products or customers. c. resource costs to a plantwide pool. d. resource costs to individual activities. e. resource costs to

The first stage of ABC entails the assignment of a. resource costs to departments. b. activity costs to products or customers. c. resource costs to a plantwide pool. d. resource costs to individual activities. e. resource costs to

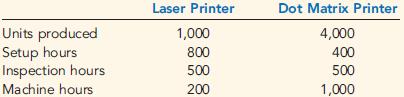

Refer to the data for Multiple-Choice Exercise 7-3. Suppose that machine hours are used to assign all overhead costs to the two products. Select the best answer from the following: a. Laser printers are undercosted, and dot matrix printers are overcosted. b. Laser printers

Consider the information given on two products and their activity usage:The consumption ratios for the setup activity for each product are a. 0.167; 0.833. b. 0.333; 0.667. c. 0.500; 0.500. d. 0.20; 0.80. e. none of the above.

Consider the information given on two products and their activity usage:

Which of the following is a nonunit-level driver? a. Direct labor hours b. Machine hours c. Setup hours d. Direct materials e. Assembly hours

A unit-level driver is consumed by a product each and every time that a. a batch of products is produced. b. a purchase order is issued. c. a unit is produced. d. a customer complains. e. none of the above.

Refer to the data in Cornerstone Exercise 6-29.Required:Prepare a cost of production report.Data From Exercise 6-29:Bebida Inc. produces soft drinks. Mixing is the first department and its output is measured in gallons. Bebida uses the FIFO method. All manufacturing costs are added uniformly. For

Transferred-in goods are treated by the receiving department as a. units started for the period. b. a material added at the beginning of the process. c. a category of materials separate from conversion costs. d. All of the above. e. None

With nonuniform inputs, the cost of EWIP is calculated by a. multiplying the unit cost in each input category by the equivalent units of each input found in EWIP. b. subtracting the cost of goods transferred out from the total cost of materials. c. adding the

When materials are added either at the beginning or the end of the process, a unit cost should be calculated for the a. materials and labor categories. b. materials category only. c. materials and conversion categories. d. conversion category

For August, Lanny Company had 25,000 units in BWIP, 40 percent complete, with costs equal to $36,000. During August, the cost incurred was $450,000. Using the FIFO method, Lanny had 125,000 equivalent units for August. There were 100,000 units transferred out during the month. The cost of goods

Assume for August that Faust Manufacturing has manufacturing costs equal to $80,000. During August, the cost incurred was $720,000. Using the FIFO method, Faust had 120,000 equivalent units for August. The cost per equivalent unit for August is a. $6.12. b. $6.50.

During July, Faust Manufacturing started and completed 80,000 units. In BWIP, there were 25,000 units, 20 percent complete. In EWIP, there were 25,000 units, 80 percent complete. Using FIFO, the equivalent units are a. 80,000 units. b. 85,000 units. c. 65,000

During June, Faust Manufacturing started and completed 80,000 units. In BWIP, there were 25,000 units, 60 percent complete. In EWIP, there were 25,000 units, 40 percent complete. Using FIFO, the equivalent units are a. 80,000 units. b. 100,000 units. c. 90,000

For September, Murphy Company has manufacturing costs in BWIP equal to $100,000. During September, the manufacturing costs incurred were $650,000. Using the weighted average method, Murphy had 100,000 equivalent units for September. The equivalent unit cost for September is a.

For August, Kimbrell Company has costs in BWIP equal to $50,000. During August, the cost incurred was $450,000. Using the weighted average method, Kimbrell had 125,000 equivalent units for August. There were 100,000 units transferred out during the month. The cost of goods transferred out is

During June, Kimbrell Manufacturing completed and transferred out 100,000 units. In EWIP, there were 25,000 units, 40 percent complete. Using the weighted average method, the equivalent units are a. 100,000 units. b. 125,000 units. c. 105,000 units.

During May, Kimbrell Manufacturing completed and transferred out 100,000 units. In EWIP, there were 25,000 units, 80 percent complete. Using the weighted average method, the equivalent units are a. 100,000 units. b. 125,000 units. c. 105,000 units. d.

During May, Kimbrell Manufacturing completed and transferred out 100,000 units. In EWIP, there were 25,000 units, 80 percent complete. Using the weighted average method, the equivalent units are a. 100,000 units. b. 125,000 units. c. 105,000 units. d.

During May, Kimbrell Manufacturing completed and transferred out 100,000 units. In EWIP, there were 25,000 units, 80 percent complete. Using the weighted average method, the equivalent units are a. 100,000 units. b. 125,000 units. c. 105,000 units. d.

Use the following information for Multiple-Choice Exercise 6-9.The drilling department incurred $24,000 of manufacturing costs during the month of October. The department transferred out 2,000 units and had 400 equivalent units in EWIP. There was no BWIP.The cost of EWIP is a.

Use the following information for Multiple-Choice Exercise 6-8.The drilling department incurred $24,000 of manufacturing costs during the month of October. The department transferred out 2,000 units and had 400 equivalent units in EWIP. There was no BWIP.The cost of goods transferred out is

Use the following information for Multiple-Choice Exercise 6-7.The drilling department incurred $24,000 of manufacturing costs during the month of October. The department transferred out 2,000 units and had 400 equivalent units in EWIP. There was no BWIP.The unit cost for the month of October

During the month of May, the grinding department produced and transferred out 2,000 units. EWIP had 500 units, 60 percent complete. There was no BWIP. The equivalent units of output for May are a. 2,000. b. 2,500. c. 2,300. d. 2,200. e.

The costs transferred from a prior process to a subsequent process a. are treated as another type of material cost. b. are referred to as transferred-in costs (for the receiving department). c. are referred to as the cost of goods transferred out (for the

To record the transfer of costs from a prior process to a subsequent process, the following entry would be made: a. debit Finished Goods and credit Work in Process. b. debit Work in Process (subsequent department) and credit Transferred-In Materials. c. debit

Sequential processing is characterized by a. a pattern where partially completed units are worked on simultaneously. b. a pattern where different partially completed units must pass through parallel processes before being brought together in a final process. c. a

Operation costing works well whenever a. heterogeneous products pass through a series of processes and receive similar doses of materials, labor, and overhead. b. homogeneous products pass through a series of processes and receive similar doses of materials, labor, and

Process costing works well whenever a. heterogeneous products pass through a series of processes and receive similar doses of materials, labor, and overhead. b. homogeneous products pass through a series of processes and receive similar amounts of materials, labor, and

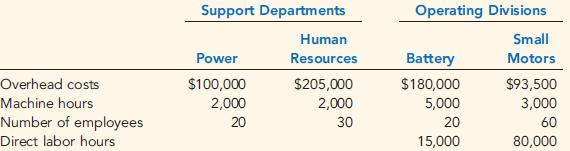

Refer to Exercise 5-44 for data. Now assume that Dexter Company uses the sequential method to allocate support department costs to the producing departments. Human Resources is allocated first in the sequential method for Dexter.Required: 1. Calculate the allocation ratios for Power and

(Appendix 5B) The method that assigns support department costs by giving full recognition to support department interactions is known as a. the sequential method. b. the proportional method. c. the reciprocal method. d. the direct method.

(Appendix 5B) The method that assigns support department costs by giving partial recognition to support department interactions is known as a. the sequential method. b. the proportional method. c. the reciprocal method. d. the direct method.

(Appendix 5B) The method that assigns support department costs only to producing departments in proportion to each department’s usage of the service is known as a. the sequential method. b. the proportional method. c. the reciprocal method. d. the

(Appendix 5B) The method that assigns support department costs only to producing departments in proportion to each department’s usage of the service is known as a. the sequential method. b. the proportional method. c. the reciprocal method. d. the

(Appendix 5B) An example of a support department is a. data processing. b. personnel. c. a materials storeroom. d. payroll. e. all of the above.

(Appendix 5B) An example of a producing department is a. a materials storeroom. b. the maintenance department. c. engineering design. d. assembly. e. all of the above.

(Appendix 5B) Those departments that provide essential services to producing departments are referred to as a. revenue generating departments. b. support departments. c. profit centers. d. production departments. e. none of the above.

(Appendix 5B) Those departments responsible for creating products or services that are sold to customers are referred to as a. profit making departments. b. support departments. c. cost centers. d. production departments. e. none of the

(Appendix 5A) When a job costing $2,000 is finished but not sold, the following journal entry is made: a. Cost of Goods Sold 2,000 Finished Goods

Wilson Company has a predetermined overhead rate of $5 per direct labor hour. The job order cost sheet for Job 145 shows 1,000 direct labor hours costing $10,000 and materials requisitions totaling $7,500. Job 145 had 500 units completed and transferred to Finished Goods. What is the cost per unit

The costs of a job are accounted for on the a. materials requisition sheet. b. time ticket. c. requisition for overhead application. d. job-order cost sheet. e. sales invoice.

When a job is completed, the total cost of the job is a. subtracted from the raw materials account. b. subtracted from the work-in-process account. c. subtracted from the finished goods account. d. added to the accounts payable account. e.

When materials are requisitioned for use in production in a job-order costing firm, the cost of materials is added to the a. raw materials account. b. work-in-process account. c. finished goods account. d. accounts payable account. e. cost

Which of the following is typically a process-costing firm? a. Paint manufacturer b. Custom cabinetmaker c. Large regional medical center d. Law office e. Custom framing shop

Which of the following is typically a job-order costing firm? a. Paint manufacturer b. Pharmaceutical manufacturer c. Large regional medical center d. Cement manufacturer e. Cleaning products manufacturer

The overhead variance is overapplied if a. actual overhead is less than applied overhead. b. actual overhead is more than applied overhead. c. applied overhead is less than actual overhead. d. estimated overhead is less than applied overhead.

Applied overhead is a. an important part of normal costing. b. never used in normal costing. c. an important part of actual costing. d. the predetermined overhead rate multiplied by estimated activity level. e. the predetermined overhead

The predetermined overhead rate equals a. actual overhead divided by actual activity level for a period. b. estimated overhead divided by estimated activity level for a period. c. actual overhead minus estimated overhead. d. actual overhead multiplied

The predetermined overhead rate is a. calculated at the end of each month. b. calculated at the end of the year. c. equal to actual overhead divided by actual activity level for a period. d. equal to estimated overhead divided by actual activity level

In a normal costing system, the cost of a job includes a. actual direct materials, actual direct labor, and actual overhead. b. estimated direct materials, estimated direct labor, and estimated overhead. c. actual direct materials, actual direct labor, actual

The ending balance of which of the following accounts is calculated by summing the totals of the open (unfinished) job-order cost sheets? a. Raw Materials b. Work in Process c. Finished Goods d. Cost of Goods Sold e. Overhead Control

Which of the following statements is true? a. Job-order costing is used only in manufacturing firms. b. The job cost sheet is subsidiary to the work-in-process account. c. Job-order costing is simpler to use than process costing because the recordkeeping

Solemon Company has fixed costs of $15,000, variable cost per unit of $5, and a price of $8. If Solemon wants to earn a targeted profit of $3,600, how many units must be sold? a. 6,200 b. 5,000 c. 1,200 d. 3,720 e. 1,875

If a company’s fixed costs rise by $10,000, which of the following will be true? a. The break-even point will decrease. b. The variable cost ratio will increase. c. The break-even point will be unchanged. d. The variable cost ratio will

Use the following information for 4-10The variable cost ratio and the contribution margin ratio for Corleone are Variable cost ratio Contribution margin ratio a. 80%

Use the following information for 4-9Corleone Company produces a single product with a price of $15, variable costs per unit of $12, and fixed costs of $9,000.Corleone’s break-even point in units a. is 600. b. is 750. c. is 9,000. d. is 3,000.

The contribution margin is the a. amount by which sales exceed fixed costs. b. difference between sales and total expenses. c. difference between sales and operating income. d. difference between sales and total variable expense. e.

If the margin of safety is 0, then a. the company is operating at a loss. b. the company is precisely breaking even. c. the company is earning a small profit. d. the margin of safety cannot be less than or equal to 0; it must be positive.

The use of fixed costs to extract higher percentage changes in profits as sales activity changes involves a. margin of safety. b. operating leverage. c. degree of operating leverage. d. sensitivity analysis. e. variable cost reduction.

An important assumption of cost-volume-profit analysis is that a. both costs and revenues are linear functions. b. all cost and revenue relationships are analyzed within the relevant range. c. there is no change in inventories. d. sales mix remains

In the cost-volume-profit graph, a. the break-even point is found where the total revenue curve crosses the x-axis. b. the area of profit is to the left of the break-even point. c. the area of loss cannot be determined. d. both the total revenue curve

Break-even revenue for the multiple-product firm can a. be calculated by dividing total fixed cost by the overall contribution margin ratio. b. be calculated by dividing segment fixed cost by the overall contribution margin ratio. c. be calculated by dividing

The amount of revenue required to earn a targeted profit is equal to a. fixed cost divided by contribution margin. b. fixed cost divided by contribution margin ratio. c. fixed cost plus targeted profit divided by contribution margin ratio. d. targeted

If the variable cost per unit goes up, Contribution margin Break-even point a. increases increases. b.

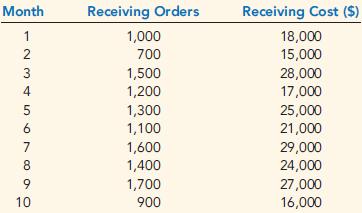

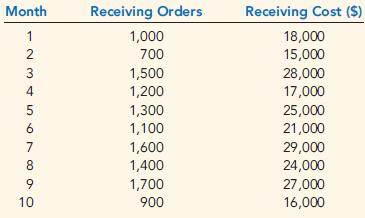

Refer to the Farnsworth Company information in Problem 3-41 for the first 10 months of data on receiving orders and receiving cost. Now suppose that Tracy has gathered two more months of data:For the following requirements, round the intercept terms to the nearest dollar and round the variable

Refer to the Farnsworth Company information in Problem 3-41 for the first 10 months of data on receiving orders and receiving cost. Now suppose that Tracy has gathered two more months of data:For the following requirements, round the intercept terms to the nearest dollar and round the variable

Refer to the Farnsworth Company information in Problem 3-41. However, now assume that Tracy has used the method of least squares on the receiving data and has gotten the following results: Intercept

Refer to the company information in Exercise 3-33.Required:1. What is the cost formula for a year?2. Using the cost formula from Requirement 1, predict the cost of parts inspection for a year in which 29,000 parts are inspected.Data From Exercise 3-33: The method of least squares was used to

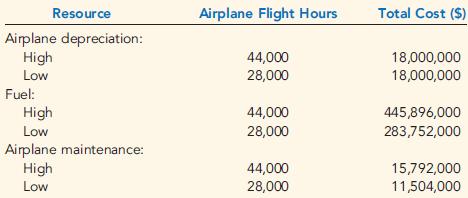

Refer to the Fly High Airlines company information in Exercise 3-31.Required:1. Develop annual cost formulas for airplane depreciation, fuel, and airplane maintenance.2. Using the three annual cost formulas that you developed, predict the cost of each resource in a year with 480,000 airline flight

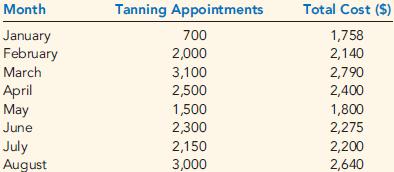

Refer to the Luisa Crimini company information in Exercise 3-28.Required:Prepare a scattergraph based on Luisa’s data. Use cost for the vertical axis and number of tanning appointments for the horizontal. Based on an examination of the scattergraph, does there appear to be a linear relationship

Refer to the Ben Palman art gallery information in Exercise 3-26.Required:1. Assume that the cost driver is number of opening shows. Develop the cost formula for the gallery’s costs for a year.2. Using the formula developed in Requirement 1, what is the total cost for Ben in a year with 12

Appendix) In the method of least squares, the coefficient that tells the percentage of variation in the dependent variable that is explained by the independent variable is a. the intercept term. b. the x-coefficient. c. the coefficient of correlation.

The cost formula for monthly supervisory cost in a factory. Total cost =$4,500This cost a. is strictly variable. b. is strictly fixed. c. is a mixed cost. d. is a step cost.

An advantage of the scattergraph method is that it a. is objective. b. is easier to use than the high-low method. c. is the most accurate method. d. removes outliers. e. is descriptive of nonlinear data.

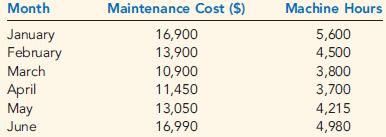

The following six months of data were collected on maintenance cost and the number of machine hours in a factory:Select the correct set of high and low months.

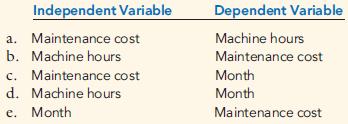

The following six months of data were collected on maintenance cost and the number of machine hours in a factory:Select the independent and dependent variables

An advantage of the high-low method is that it a. is objective. b. is subjective. c. is the most accurate method. d. removes outliers. e. is descriptive of nonlinear data.

The following cost formula for total purchasing cost in a factory was developed using monthly data. Purchasing cost =$123,800 + ($15 × Number of purchase orders)Next month, 2,000 purchase orders are predicted. The total cost predicted for the purchasing department next

The following cost formula was developed using monthly data for a hospital. Total cost = $51,400 + ($125 × Number of patient days)The term ‘‘Total cost’’ a. is the variable rate. b. is the intercept. c. is the dependent

The following cost formula was developed using monthly data for a hospital. Total cost = $51,400 + ($125 × Number of patient days)The term ‘‘Number of patient days’’ a. is the variable rate. b. is the intercept. c. is the dependent

The following cost formula was developed using monthly data for a hospital. Total cost = $51,400 + ($125 × Number of patient days)The term $125 a. is the variable rate. b. is the intercept. c. is the dependent variable. d. is the

The following cost formula was developed by using monthly data for a hospital. Total cost = $51,400 + ($125 × Number of patient days)The term $51,400 a. is the variable rate. b. is the intercept. c. is the dependent variable.

Which of the following would probably be a fixed cost in an automobile insurance company? a. Application forms b. Time spent by adjusters to evaluate accidents c. The salary of customer service representatives d. All of the above

Which of the following would probably be a variable cost in a soda bottling plant? a. Direct labor b. Bottles c. Carbonated water d. Power to run the bottling machine e. All of the above

A factor that causes or leads to a change in a cost or activity is a(n) a. driver. b. intercept. c. slope. d. variable term. e. cost object.

A factor that causes or leads to a change in a cost or activity is a(n) a. driver. b. intercept. c. slope. d. variable term. e. cost object.

Refer to the data provided in Exercise 2-39.Required:Prepare an income statement for Jasper Company for last year. Calculate the percentage of sales for each line item on the income statement. Round percentages to the nearest tenth of a percent..Data From Exercise 2-39:Jasper Company provided the

Refer to the data provided in Exercise 2-39.Required:1. Calculate the sales revenue for last year.2. Prepare an income statement for Jasper Company for last year.Data From Exercise 2-39:Jasper Company provided the following information for last year: Sales in units

Refer to the data provided in Exercise 2-37.Required:What was the cost of goods sold for March?Data From Exercise 2-37:In March, Chilton Company purchased materials costing $14,000 and incurred direct labor cost of $20,000. Overhead totaled $36,000 for the month. Information on inventories was as

Refer to the Barnard Company information in Multiple-Choice Exercise 2-13. Operating income is a. $34,000. b. $110,000. c. $234,000. d. $270,000. e. $74,000

Refer to the Barnard Company information in Multiple-Choice Exercise 2-13. The total period expense is a. $276,000. b. $200,000. c. $76,000. d. $40,000. e. $36,000.

Refer to the Barnard Company information in Multiple-Choice Exercise 2-13. The gross margin per unit is a. $24.00. b. $11.00. c. $16.00. d. $26.00. e. $3.40.

Refer to the Barnard Company information in Multiple-Choice Exercise 2-13. The cost of goods sold per unit is: a. $7.00. b. $20.00. c. $15.00. d. $5.00. e. $27.60.

Refer to the Barnard Company information in Multiple-Choice Exercise 2-13. Conversion cost per unit is: a. $7.00. b. $20.00. c. $15.00. d. $5.00. e. $27.60.

Refer to the Barnard Company information in Multiple-Choice Exercise 2-13. Conversion cost per unit is: a. $7.00. b. $20.00. c. $15.00. d. $5.00. e. $27.60.

Last year, Barnard Company incurred the following costs: Direct materials $ 50,000 Direct labor

Which of the following is a period expense? a. Factory insurance b. CEO salary c. Direct labor d. Factory maintenance e. All of the above

JackMan Company produces diecast metal bulldozers for toy shops. JackMan estimated the following average costs per bulldozer: Direct materials $8.65

Showing 4100 - 4200

of 5971

First

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

Last

Step by Step Answers