New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

principles corporate finance

Corporate Finance 6th Edition Jonathan Berk, Peter DeMarzo - Solutions

Simple Simon’s Bakery purchases supplies on terms of 1/10, Net 25. If Simple Simon’s chooses to take the discount offered, it must obtain a bank loan to meet its short-term financing needs.A local bank has quoted Simple Simon’s owner an interest rate of 12% on borrowed funds.Should Simple

Your firm purchases goods from its supplier on terms of 3/15, Net 40.a. What is the effective annual cost to your firm if it chooses not to take the discount and makes its payment on day 40?b. What is the effective annual cost to your firm if it chooses not to take the discount and makes its

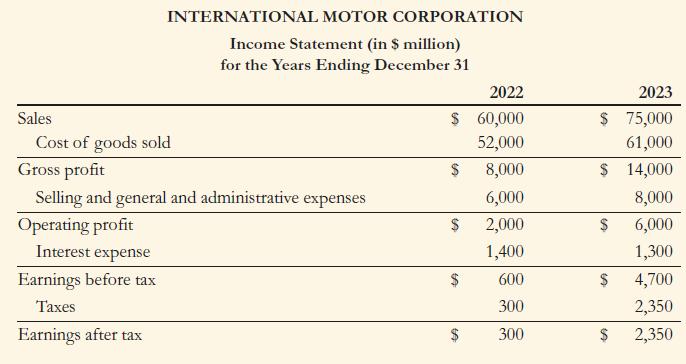

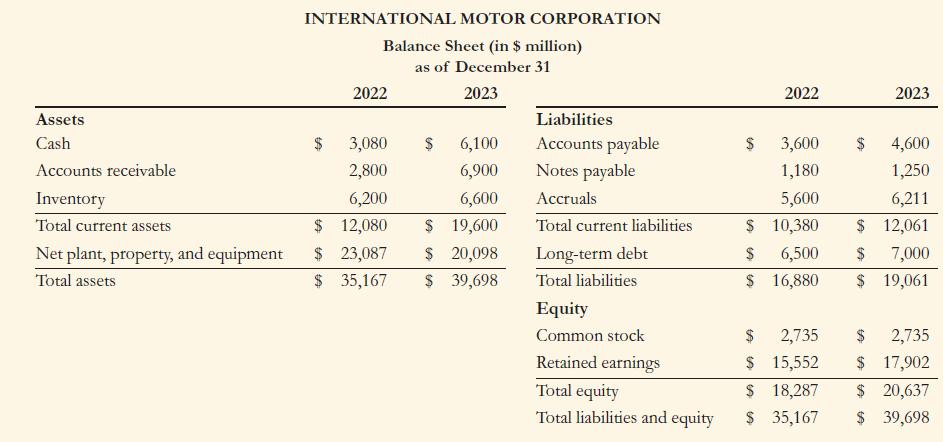

Use the financial statements supplied on the next page for International Motor Corporation( IMC) to answer the following questions.a. Calculate the cash conversion cycle for IMC for both 2022 and 2023. What change has occurred, if any? All else being equal, how does this change affect IMC’s need

Ohio Valley Homecare Suppliers, Inc. (OVHS) had $20 million in sales in 2022. Its cost of goods sold was $8 million, and its average inventory balance was $2,000,000.a. Calculate the average number of inventory days outstanding for OVHS.b. The average days of inventory in the industry is 73 days.

Which of the following short-term securities would you expect to offer the highest before-tax return: Treasury bills, certificates of deposit, short-term tax exempts, or commercial paper?Why?Appendix

What is the difference between a European option and an American option? Are European options available exclusively in Europe and American options available exclusively in the United States?Appendix

Why is an announcement of a share repurchase considered a positive signal?appendix

Suppose AMC waits until after the news comes out to do the share repurchase. What would AMC’s share price be after the repurchase if its enterprise value goes up? What would AMC’s share price be after the repurchase if its enterprise value declines?AMC Corporation currently has an enterprise

The current price of Estelle Corporation stock is $25. In each of the next two years, this stock price will either go up by 20% or go down by 20%. The stock pays no dividends. The one-year risk-free interest rate is 6% and will remain constant. Using the Binomial Model, calculate the price of a

Using the information in Problem 1, use the Binomial Model to calculate the price of a oneyear put option on Estelle stock with a strike price of $25.Appendix

The current price of Natasha Corporation stock is $6. In each of the next two years, this stock price can either go up by $2.50 or go down by $2. The stock pays no dividends. The one-year risk-free interest rate is 3% and will remain constant. Using the Binomial Model, calculate the price of a

Using the information in Problem 3, use the Binomial Model to calculate the price of a twoyear European put option on Natasha stock with a strike price of $7.Appendix

Suppose the option in Example 21.1 actually sold in the market for $8. Describe a trading strategy that yields arbitrage profits.Appendix

Suppose the option in Example 21.2 actually sold today for $5. You do not know what the option will trade for next period. Describe a trading strategy that will yield arbitrage profits.Appendix

What is the highest possible value for the delta of a call option? What is the lowest possible value?Appendix

Consider the setting of Problem 9. Suppose that in the event Hema Corp. defaults, $90 million of its value will be lost to bankruptcy costs. Assume there are no other market imperfections.a. What is the present value of these bankruptcy costs, and what is their delta with respect to the firm’s

Roslin Robotics stock has a volatility of 30% and a current stock price of $60 per share. Roslin pays no dividends. The risk-free interest is 5%. Determine the Black-Scholes value of a oneyear, at-the-money call option on Roslin stock.Appendix

Rebecca is interested in purchasing a European call on a hot new stock, Up, Inc. The call has a strike price of $100 and expires in 90 days. The current price of Up stock is $120, and the stock has a standard deviation of 40% per year. The risk-free interest rate is 6.18% per year.a. Using the

Using the data in Table 21.1, compare the price on July 24, 2009, of the following options on JetBlue stock to the price predicted by the Black-Scholes formula. Assume that the standard deviation of JetBlue stock is 65% per year and that the short-term risk-free rate of interest is 1% per year.a.

Using the market data in Figure 20.10 and a risk-free rate of 0.25% per annum, calculate the implied volatility of Google stock in September 2012, using the bid price of the 700 January 2014 call option.Appendix

Using the implied volatility you calculated in Problem 14, and the information in that problem, use the Black-Scholes option pricing formula to calculate the value of the 750 January 2014 call option.Appendix

Plot the value of a two-year European put option with a strike price of $20 on World Wide Plants as a function of the stock price. Recall that World Wide Plants has a constant dividend yield of 5% per year and that its volatility is 20% per year. The two-year risk-free rate of interest is 4%.

Consider again the at-the-money call option on Roslin Robotics evaluated in Problem 11.What is the impact on the value of this call option of each of the following changes (evaluated separately)?a. The stock price increases by $1 to $61.b. The volatility of the stock goes up by 1% to 31%.c.

Harbin Manufacturing has 10 million shares outstanding with a current share price of $20 per share. In one year, the share price is equally likely to be $30 or $18. The risk-free interest rate is 5%.a. What is the expected return on Harbin stock?b. What is the risk-neutral probability that

Using the information on Harbin Manufacturing in Problem 19, answer the following:a. Using the risk-neutral probabilities, what is the value of a one-year call option on Harbin stock with a strike price of $25?b. What is the expected return of the call option?c. Using the risk-neutral

Using the information in Problem 1, calculate the risk-neutral probabilities. Then use them to price the option.Appendix

Using the information in Problem 3, calculate the risk-neutral probabilities. Then use them to price the option.Appendix

Explain the difference between the risk-neutral and actual probabilities. In which states is one higher than the other? Why?Appendix

Explain why risk-neutral probabilities can be used to price derivative securities in a world where investors are risk averse.Appendix

Calculate the beta of the January 2010 $9 call option on JetBlue listed in Table 21.1. Assume that the volatility of JetBlue is 65% per year and its beta is 0.85. The short-term risk-free rate of interest is 1% per year. What is the option’s leverage ratio?Appendix

Consider the March 2010 $5 put option on JetBlue listed in Table 21.1. Assume that the volatility of JetBlue is 65% per year and its beta is 0.85. The short-term risk-free rate of interest is 1%per year.a. What is the put option’s leverage ratio?b. What is the beta of the put option?c. If the

Return to Example 20.11 (on page 754), in which Google was contemplating issuing zerocoupon debt due in 16 months with a face value of $163.5 billion, and using the proceeds to pay a special dividend. Google currently has a market value of $229.2 billion and the risk-free rate is 0.25%. Using the

You would like to know the unlevered beta of Schwartz Industries (SI). SI’s value of outstanding equity is $400 million, and you have estimated its beta to be 1.2. SI has four-year zerocoupon debt outstanding with a face value of $100 million that currently trades for $75 million.SI pays no

Suppose that in December 2016, the spot exchange rate for the Japanese yen is ¥116/$. At the same time, the one-year interest rate in the United States is 4.85% and the one-year interest rate in Japan is 0.10%. Based on these rates, what forward exchange rate is consistent with no arbitrage?

You are a U.S. investor who is trying to calculate the present value of a e5 million cash inflow that will occur one year in the future. The spot exchange rate is 5 = \($1.25/€\) and the forward rate is F1 = \($1.215/€.\) You estimate that the appropriate dollar discount rate for this cash flow

The dollar cost of debt for Healy Consulting, a U.S. research firm, is 7.5%. The firm faces a tax rate of 30% on all income, no matter where it is earned. Managers in the firm need to know its yen cost of debt because they are considering launching a new bond issue in Tokyo to raise money for a new

Tailor Johnson, the menswear company with a subsidiary in Ethiopia described in Problem 13, is considering the tax benefits resulting from deferring repatriation of the earnings from the subsidiary. Under U.S. tax law, the U.S. tax liability is not incurred until the profits are brought back home.

Assume that in the original Ityesi example in Table 23.2, all sales actually occur in the United States and are projected to be $60 million per year for four years. Keeping other costs in pounds as shown in the table, calculate the NPV of the investment opportunity. Also remember that when the EBIT

You are a senior financial analyst with IBM in its capital budgeting division. IBM is considering expanding in Australia due to its positive business atmosphere and cultural similarities to the United States.The new facility would require an initial investment in fixed assets of \($5\) billion

Explain the meanings of the following financial terms:a. Optionb. Expiration datec. Strike priced. Calle. Put Appendix

Explain the difference between a long position in a put and a short position in a call.Appendix

Which of the following positions benefit if the stock price increases?a. Long position in a callb. Short position in a callc. Long position in a putd. Short position in a put Appendix

You own a call option on Intuit stock with a strike price of $40. The option will expire in exactly three months’ time.a. If the stock is trading at $55 in three months, what will be the payoff of the call?b. If the stock is trading at $35 in three months, what will be the payoff of the call?c.

Assume that you have shorted the call option in Problem 6.a. If the stock is trading at $55 in three months, what will you owe?b. If the stock is trading at $35 in three months, what will you owe?c. Draw a payoff diagram showing the amount you owe at expiration as a function of the stock price at

You own a put option on Ford stock with a strike price of $10. The option will expire in exactly six months’ time.a. If the stock is trading at $8 in six months, what will be the payoff of the put?b. If the stock is trading at $23 in six months, what will be the payoff of the put?c. Draw a payoff

Assume that you have shorted the put option in Problem 8.a. If the stock is trading at $8 in three months, what will you owe?b. If the stock is trading at $23 in three months, what will you owe?c. Draw a payoff diagram showing the amount you owe at expiration as a function of the stock price at

What position has more downside exposure: a short position in a call or a short position in a put? That is, in the worst case, in which of these two positions would your losses be greater?Appendix

Consider the IBM call and put options in Problem 3. Ignoring any interest you might earn over the remaining few days’ life of the options:a. Compute the break-even IBM stock price for each option (i.e., the stock price at which your total profit from buying and then exercising the option would be

You are long both a call and a put on the same share of stock with the same exercise date. The exercise price of the call is $40 and the exercise price of the put is $45. Plot the value of this combination as a function of the stock price on the exercise date.Appendix

You are long two calls on the same share of stock with the same exercise date. The exercise price of the first call is $40 and the exercise price of the second call is $60. In addition, you are short two otherwise identical calls, both with an exercise price of $50. Plot the value of this

A forward contract is a contract to purchase an asset at a fixed price on a particular date in the future. Both parties are obligated to fulfill the contract. Explain how to construct a forward contract on a share of stock from a position in options.Appendix

You own a share of Costco stock. You are worried that its price will fall and would like to insure yourself against this possibility. How can you purchase insurance against this possibility?Appendix

It is February 21, 2022, and you own IBM stock. You would like to insure that the value of your holdings will not fall significantly. Using the data in Problem 3, and expressing your answer in terms of a percentage of the current value of your portfolio:a. What will it cost to insure that the value

Dynamic Energy Systems stock is currently trading for $33 per share. The stock pays no dividends.A one-year European put option on Dynamic with a strike price of $35 is currently trading for $2.10. If the risk-free interest rate is 10% per year, what is the price of a one-year European call option

You happen to be checking the newspaper and notice an arbitrage opportunity. The current stock price of Intrawest is $20 per share and the one-year risk-free interest rate is 8%. A oneyear put on Intrawest with a strike price of $18 sells for $3.33, while the identical call sells for$7. Explain

Consider the IBM call and put options in Problem 3. IBM paid a dividend on February 10, 2022, and was not scheduled to pay another dividend until May 2022. Ignoring the negligible interest you might earn on T-bills over the remaining few days’ life of the options, show that there is no arbitrage

In mid-March 2022, European-style options on the S&P 100 index (OEX) expiring in December 2023 were priced as follows:Given an interest rate of 1.7% for a December 2023 maturity (21 months in the future), use put-call parity (with dividends) to determine:a. The price of a December 2023 OEX put

Suppose Amazon stock is trading for $2000 per share, and Amazon pays no dividends.a. What is the maximum possible price of a call option on Amazon?b. What is the maximum possible price of a put option on Amazon with a strike price of $2250?c. What is the minimum possible value of a call option on

Consider the data for IBM options in Problem 3. Suppose a new American-style put option on IBM is issued with a strike price of $130 and an expiration date of April 1st.a. What is the maximum possible price for this option?b. What is the minimum possible price for this option?Appendix

You are watching the option quotes for your favorite stock, when suddenly there is a news announcement.Explain what type of news would lead to the following effects:a. Call prices increase, and put prices fall.b. Call prices fall, and put prices increase.c. Both call and put prices increase.Appendix

Explain why an American call option on a non-dividend-paying stock always has the same price as its European counterpart.Appendix

Consider an American put option on XAL stock with a strike price of $55 and one year to expiration.Assume XAL pays no dividends, XAL is currently trading for $10 per share, and the one-year interest rate is 10%. If it is optimal to exercise this option early:a. What is the price of a one-year

The stock of Harford Inc. is about to pay a $0.30 dividend. It will pay no more dividends for the next month. Consider call options that expire in one month. If the interest rate is 6% APR(monthly compounding), what is the maximum strike price where it could be possible that early exercise of the

Suppose the S&P 500 is at 2700, and a one-year European call option with a strike price of$1200 has a negative time value. If the interest rate is 5%, what can you conclude about the dividend yield of the S&P 500? (Assume all dividends are paid at the end of the year.)Appendix

Suppose the S&P 500 is at 2700, and it will pay a dividend of $90 at the end of the year.Suppose also that the interest rate is 2%. If a one-year European put option has a negative time value, what is the lowest possible strike price it could have?Appendix

Wesley Corp. stock is trading for $25/share. Wesley has 20 million shares outstanding and a market debt-equity ratio of 0.5. Wesley’s debt is zero-coupon debt with a 5-year maturity and a yield to maturity of 10%.a. Describe Wesley’s equity as a call option. What is the maturity of the call

Express the position of an equity holder in terms of put options.Appendix

Use the option data from July 13, 2009, in the following table to determine the rate Google would have paid if it had issued $128 billion in zero-coupon debt due in January 2011. Suppose Google currently had 320 million shares outstanding, implying a market value of $135.1 billion.(Assume perfect

Suppose that in July 2009, Google were to issue $96 billion in zero-coupon senior debt, and another $32 billion in zero-coupon junior debt, both due in January 2011. Use the option data in the preceding table to determine the rate Google would pay on the junior debt issue. (Assume perfect capital

Homer Boats has accounts payable days of 38, inventory days of 65, and accounts receivable days of 32.What is its operating cycle?

FastChips Semiconductors has inventory days of 83, accounts receivable days of 45, and accounts payable days of 75.What is its cash conversion cycle?

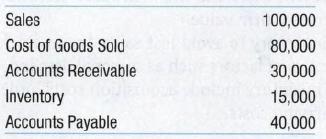

Westerly Industries has the following financial information. What is its cash conversion cycle? Sales 100,000 Cost of Goods Sold 80,000 Accounts Receivable 30,000 Inventory 15,000 Accounts Payable 40,000

Aberdeen Outboard Motors is contemplating building a new plant. The company anticipates that the plant will require an initial investment of $3.5 million in net working capital today. The plant will last 15 years, at which point the full investment in net working capital will be recovered. Given an

Your firm currently has net working capital of $250,000 that it expects to grow at a rate of 8% per year forever. You are considering some suggestions that could slow that growth to 6% per year. If your discount rate is 15%, how would these changes impact the value of your firm?

Assume the credit terms offered to your firm by your suppliers are 2/10, net 60.Calculate the cost of the trade credit if your firm does not take the discount and pays on day 60.

Your supplier offers terms of 4/10, net 60.What is the effective annual cost of trade credit if you choose to forgo the discount and pay on day 60?

The Saban Corporation is trying to decide whether to switch to a bank that will accommodate electronic funds transfers from Saban’s customers. Saban’s financial manager believes the new system would decrease its collection float by as much as eight days. The new bank would require a

The Manana Corporation had sales of $280 million this year. Its accounts receivable balance averaged $25 million. How long, on average, does it take the firm to collect on its sales?

Your company had $12 million in sales last year. Its cost of goods sold was $8 million and its average inventory balance was $1,680,000. What was its average days of inventory?

You are the Chief Financial Officer (CFO) of Walmart. This afternoon you played golf with a member of the company’s board of directors. Somewhere during the back nine, the board member enthusiastically described a recent article she had read in a leading management journal. This article noted

Describe the different approaches a firm could take when preparing for cash flow shortfalls.

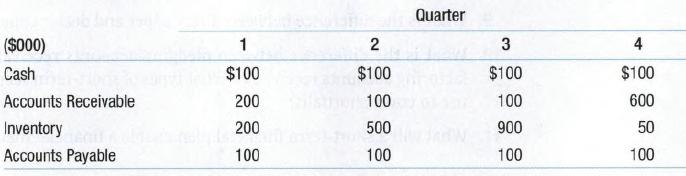

What are the permanent working capital needs of your company? What are the temporary needs (see MyFinanceLab for the data in Excel format)?The following table includes quarterly working capital levels for your firm for the next year. Quarter ($000) 1 2 3 st 4 Cash $100 $100 $100 $100 Accounts

If you chose to use only long-term financing, what total amount of borrowing would you need to have on a permanent basis? Forecast your excess cash levels under this scenario (see MyFinanceLab for the data in Excel format).The following table includes quarterly working capital levels for your firm

If you hold only $100 in cash at any time, what is your maximum short-term borrowing and when (see MyFinanceLab for the data in Excel format)?The following table includes quarterly working capital levels for your firm for the next year. Quarter ($000) 1 2 3 st 4 Cash $100 $100 $100 $100 Accounts

If you choose to enter the year with $400 total in cash, what is your maximum shortterm borrowing (see MyFinanceLab for the data in Excel format)?The following table includes quarterly working capital levels for your firm for the next year. Quarter ($000) 1 2 3 st 4 Cash $100 $100 $100 $100

If you want to limit your maximum short-term borrowing to $500, how much excess cash must you carry (see MyFinanceLab for the data in Excel format)?The following table includes quarterly working capital levels for your firm for the next year. Quarter ($000) 1 2 3 st 4 Cash $100 $100 $100 $100

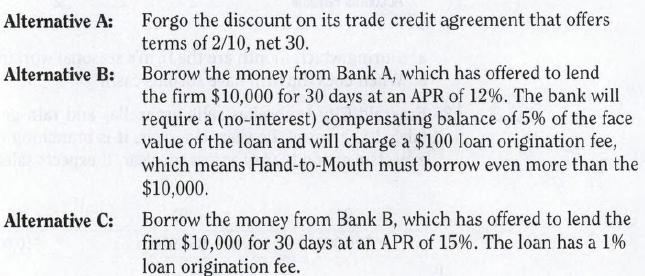

The Hand-to-Mouth Company needs a $10,000 loan for the next 30 days. It is trying to decide among three options:Which alternative is the cheapest source of financing for Hand-to-Mouth? Alternative A: Forgo the discount on its trade credit agreement that offers terms of 2/10, net 30. Alternative B:

Explain put-call parity.

It is August 21, 2013, and you have decided to purchase 10 September call contracts on Amazon’s stock with an exercise price of $285. Because you are buying, you must pay the ask price. How much money will this purchase cost you? Is this option in-the-money or out-of-the-money?

You are short a put option on Oracle stock with an exercise price of $20 that expires today. Plot the value of this option as a function of the stock price.

Assume you decided to purchase the September 275 through 290 put options quoted in Table 21.2 on August 21, 2013, and you financed each position by borrowing at 3% for 31 days. Plot the profit of each position as a function of the stock price on expiration.

What is the difference between a European option and an American option?

Assume that you have shorted the call option in Problem 2.a. If the stock is trading at \($55\) in three months, what will you owe?b. If the stock is trading at \($35\) in three months, what will you owe?c. Draw a payoff diagram showing the amount you owe at expiration as a function of the stock

Assume that you have shorted the put option in Problem 4.a. If the stock is trading at \($8\) in three months, what will you owe?b. If the stock is trading at \($23\) in three months, what will you owe?c. Draw a payoff diagram showing the amount you owe at expiration as a function of the stock

Why do you think shareholders from target companies enjoy an average gain when acquired, while acquiring shareholders often do not gain anything?

Your company has earnings per share of \($4\). It has 1 million shares outstanding, each of which has a price of \($40\). You are thinking of buying TargetCo, which has earnings per share of \($2\), 1 million shares outstanding, and a price per share of \($25\). You will pay for TargetCo by issuing

The NFF Corporation has announced plans to acquire LE Corporation. NFF is trading at \($35\) per share and LE is trading at \($25\) per share, implying a premerger value of LE of \($4\) billion. If the projected synergies are \($1\) billion, what is the maximum exchange ratio NFF could offer in a

Assume that all investors have the same information and care only about expected return and volatility. If new information arrives about one stock, can this information affect the price and return of other stocks? If so, explain why?Appendix

Assume that the CAPM is a good description of stock price returns. The market expected return is 7% with 10% volatility and the risk-free rate is 3%. New news arrives that does not change any of these numbers but it does change the expected return of the following stocks:a. At current market

Suppose the CAPM equilibrium holds perfectly. Then the risk-free interest rate increases, and nothing else changes.a. Is the market portfolio still efficient?b. If your answer to part (a) is yes, explain why. If not, describe which stocks would be buying opportunities and which stocks would be

Showing 1800 - 1900

of 5445

First

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

Last

Step by Step Answers