New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

strategy in practice

Wiley CPA Exam Review Regulation 2012 9th Edition O. Ray Whittington, Patrick R. Delaney - Solutions

Which one of the following statements concerning Roth IRAs is not correct?a. The maximum annual contribution to a Roth IRA is reduced if adjusted gross income exceeds certain thresholds.b. Contributions to a Roth IRA are not deductible.c. An individual is allowed to make contributions to a Roth IRA

Richard Putney, who lived in Idaho for five years, moved to Texas in 2011 to accept a new position. His employer reimbursed him in full for all direct moving costs, but did not pay for any part of the following indirect moving expenses incurred by Putney:Househunting trips to Texas $800 Temporary

Martin Dawson, who resided in Detroit, was unemployed for the last six months of 2010. In January 2011, he moved to Houston to seek employment, and obtained a full-time job there in February. He kept this job for the balance of the year. Martin paid the following expenses in 2011 in connection with

James, a calendar-year taxpayer, was employed and resided in Boston. On February 4, 2011, James was permanently transferred to Florida by his employer. James worked full-time for the entire year. In 2011, James incurred and paid the following unreimbursed expenses in relocating.Lodging and travel

Charles Gilbert, a corporate executive, incurred business-related unreimbursed expenses in 2011 as follows:Entertainment $900 Travel 700 Education 400 Assuming that Gilbert does not itemize deductions, how much of these expenses should he deduct on his 2011 tax return?a. $0b. $ 700c. $1,300d. $1,600

Adams owns a second residence that is used for both personal and rental purposes. During 2011, Adams used the second residence for 50 days and rented the residence for 200 days. Which of the following statements is correct?a. Depreciation may not be deducted on the property under any

Easel Co. has elected to reimburse employees for business expenses under a nonaccountable plan. Easel does not require employees to provide proof of expenses and allows employees to keep any amount not spent. Under the plan, Mel, an Easel employee for a full year, gets $400 per month for business

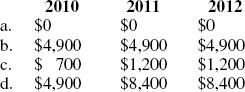

During August 2011, Roe Corp. purchased and placed in service a machine to be used in its manufacturing operations. This machine cost$2,014,000. What portion of the cost may Roe elect to treat as an expense rather than as a capital expenditure?a. $236,000b. $250,000c. $486,000d. $500,000

With regard to depreciation computations made under the general MACRS method, the half-year convention provides thata. One-half of the first year’s depreciation is allowed in the year in which the property is placed in service, regardless of when the property is placed in service during the year,

Under the modified accelerated cost recovery system (MACRS) of depreciation for property placed in service after 1986,a. Used tangible depreciable property is excluded from the computation.b. Salvage value is ignored for purposes of computing the MACRS deduction.c. No type of straight-line

Data Corp., a calendar-year corporation, purchased and placed into service office equipment during October 2011. No other equipment was placed into service during 2011. Under the general MACRS depreciation system, what convention must Data use?a. Full-year.b. Half-year.c. Midquarter.d. Midmonth.

On June 29, 2011, Sullivan purchased and placed into service an apartment building costing $360,000 including $30,000 for the land.What was Sullivan’s MACRS deduction for the apartment building in 2011?a. $7,091b. $6,500c. $6,000d. $4,583

Krol Corp., a calendar-year taxpayer, purchased used furniture and fixtures for use in its business and placed the property in service on November 1, 2010. The furniture and fixtures cost $56,000 and represented Krol’s only acquisition of depreciable property during the year. Krol did not elect

Which of the following conditions must be satisfied for a taxpayer to expense, in the year of purchase, under Internal Revenue Code Section 179, the cost of new or used tangible depreciable personal property?I. The property must be purchased for use in the taxpayer’s active trade or business.II.

Aviation Corp. manufactures model airplanes for children. During 2011, Aviation purchased $820,000 of production machinery to be used in its business. For 2011, Aviation’s taxable income before any Sec. 179 expense deduction was $195,000. What is the maximum amount of Sec. 179 expense election

If an individual taxpayer’s passive losses relating to rental real estate activities cannot be used in the current year, then they may be carrieda. Back two years, but they cannot be carried forward.b. Forward up to a maximum period of twenty years, but they cannot be carried back.c. Back two

With regard to the passive loss rules involving rental real estate activities, which one of the following statements is correct?a. The term “passive activity” includes any rental activity without regard as to whether or not the taxpayer materially participates in the activity.b. Gross

Don Wolf became a general partner in Gata Associates on January 1, 2010, with a 5% interest in Gata’s profits, losses, and capital. Gata is a distributor of auto parts. Wolf does not materially participate in the partnership business. For the year ended December 31, 2010, Gata had an operating

The rule limiting the allowability of passive activity losses and credits applies toa. Partnerships.b. S corporations.c. Personal service corporations.d. Widely held C corporations.

Cobb, an unmarried individual, had an adjusted gross income of$200,000 in 2010 before any IRA deduction, taxable social security benefits, or passive activity losses. Cobb incurred a loss of $30,000 in 2010 from rental real estate in which he actively participated. What amount of loss attributable

Destry, a single taxpayer, reported the following on his US Individual Income Tax Return Form 1040:Income Wages $ 5,000 Interest on savings account 1,000 Net rental income 4,000 Deductions Personal exemption $ 3,700 Standard deduction 5,800 Net business loss 16,000 Net short-term capital loss 2,000

Robin Moore, a self-employed taxpayer, reported the following information for 2011:Income: Dividends from investments $ 500 Net short-term capital gain on sale of investment 1,000 Deductions: Net loss from business (6,000)Personal exemption (3,700)Standard deduction (5,800)What is the amount of

Jennifer, who is single, has the following items of income and deduction for 2011:Salary $30,000 Itemized deductions (all attributable to a personal casualty loss when a hurricane destroyed her residence) 45,000 Personal exemption 3,700 What is the amount of Jennifer’s net operating loss for

During the 2010 holiday season, Palo Corp. gave business gifts to seventeen customers. These gifts, which were not of an advertising nature, had the following fair market values:4 at $ 10 4 at 25 4 at 50 5 at 100 How much of these gifts was deductible as a business expense for 2010?a. $840b. $365c.

Earl Cook, who worked as a machinist for Precision Corp., loaned Precision $1,000 in 2008. Cook did not own any of Precision’s stock, and the loan was not a condition of Cook’s employment by Precision.In 2011, Precision declared bankruptcy, and Cook’s note receivable from Precision became

Jason Budd, CPA, reports on the cash basis. In April 2010, Budd billed a client $3,500 for the following professional services:Personal estate planning $2,000 Personal tax return preparation 1,000 Compilation of business financial statements 500 No part of the $3,500 was ever paid. In April 2011,

Ram Corp.’s operating income for the year ended December 31, 2010, amounted to $100,000. Included in Ram’s 2010 operating expenses is a $6,000 insurance premium on a policy insuring the life of Ram’s president. Ram is beneficiary of this policy. In Ram’s 2010 tax return, what amount should

In the case of a corporation that is not a financial institution, which of the following statements is correct with regard to the deduction for bad debts?a. Either the reserve method or the direct charge-off method may be used, if the election is made in the corporation’s first taxable year.b. On

Under the uniform capitalization rules applicable to property acquired for resale, which of the following costs should be capitalized with respect to inventory if no exceptions are met?Marketing costs Off-site storage costsa. Yes Yesb. Yes Noc. No Nod. No Yes

Which of the following costs is not included in inventory under the Uniform Capitalization rules for goods manufactured by the taxpayer?a. Research.b. Warehousing costs.c. Quality control.d. Taxes excluding income taxes.

Banks Corp., a calendar-year corporation, reimburses employees for properly substantiated qualifying business meal expenses. The employees are present at the meals, which are neither lavish nor extravagant, and the reimbursement is not treated as wages subject to withholdings. For 2011, what

Mock operates a retail business selling illegal narcotic substances. Which of the following item(s) may Mock deduct in calculating business income?I. Cost of merchandise.II. Business expenses other than the cost of merchandise.a. I only.b. II only.c. Both I and II.d. Neither I nor II.

The uniform capitalization method must be used by I. Manufacturers of tangible personal property.II. Retailers of personal property with $2 million dollars in average annual gross receipts for the three preceding years.a. I only.b. II only.c. Both I and II.d. Neither I nor II.

Which of the following taxpayers may use the cash method of accounting for tax purposes?a. Partnership that is designated as a tax shelter.b. Retail store with $2 million inventory, and $9 million average annual gross receipts.c. An international accounting firm.d. C corporation manufacturing

Dr. Berger, a physician, reports on the cash basis. The following items pertain to Dr. Berger’s medical practice in 2010:Cash received from patients in 2010 $200,000 Cash received in 2010 from third-party reimbursers for services provided by Dr.Berger in 2009 30,000 Salaries paid to employees in

Alex Burg, a cash-basis taxpayer, earned an annual salary of$80,000 at Ace Corp. in 2010, but elected to take only $50,000. Ace, which was financially able to pay Burg’s full salary, credited the unpaid balance of $30,000 to Burg’s account on the corporate books in 2010, and actually paid this

Unless the Internal Revenue Service consents to a change of method, the accrual method of tax reporting is generally mandatory for a sole proprietor when there are Accounts receivable for services rendered Year-end merchandise inventoriesa. Yes Yesb. Yes Noc. No Nod. No Yes

Blair, CPA, uses the cash receipts and disbursements method of reporting. In 2010, a client gave Blair 100 shares of a listed corporation’s stock in full satisfaction of a $5,000 accounting fee the client owed Blair. This stock had a fair market value of $4,000 on the date it was given to Blair.

On December 1, 2010, Michaels, a self-employed cash-basis calendar-year taxpayer, borrowed $100,000 to use in her business.The loan was to be repaid on November 30, 2011. Michaels paid the entire interest of $12,000 on December 1, 2010. What amount of interest is deductible on Michaels’ 2011

Axis Corp. is an accrual-basis calendar-year corporation. On December 13, 2010, the Board of Directors declared a 2% of profits bonus to all employees for services rendered during 2010 and notified them in writing. None of the employees own stock in Axis.The amount represents reasonable

In 2010, Stewart Corp. properly accrued $5,000 for an income item on the basis of a reasonable estimate. In 2011, after filing its 2010 federal income tax return, Stewart determined that the exact amount was $6,000. Which of the following statements is correct?a. No further inclusion of income is

Which of the following taxpayers may use the cash method of accounting?a. A tax shelter.b. A qualified personal service corporation.c. A C corporation with annual gross receipts of $50,000,000.d. A manufacturer with annual gross receipts of $3,000,000.

A cash-basis taxpayer should report gross incomea. Only for the year in which income is actually received in cash.b. Only for the year in which income is actually received whether in cash or in property.c. For the year in which income is either actually or constructively received in cash only.d.

John Budd is single, with no dependents. During 2010, John received wages of $11,000 and state unemployment compensation benefits of $2,000. He had no other source of income. The amount of state unemployment compensation benefits that should be included in John’s 2010 adjusted gross income isa.

Royce Rentals, Inc., an accrual-basis taxpayer, reported rent receivable of $25,000 and $35,000 in its 2010 and 2009 balance sheets, respectively. During 2010, Royce received $50,000 in rent payments and $5,000 in nonrefundable rent deposits. In Royce’s 2010 corporate income tax return, what

Amy Finch had the following cash receipts during 2011:Net rent on vacant lot used by a car dealer (lessee pays all taxes, insurance, and other expenses on the lot) $6,000 Advance rent from lessee of above vacant lot, such advance to be applied against rent for the last two months of the five-year

Emil Gow owns a two-family house that has two identical apartments. Gow lives in one apartment and rents out the other. In 2010, the rental apartment was fully occupied and Gow received$7,200 in rent. During the year ended December 31, 2010, Gow paid the following:Real estate taxes $6,400 Painting

Paul Bristol, a cash-basis taxpayer, owns an apartment building.The following information was available for 2010:An analysis of the 2010 bank deposit slips showed recurring monthly rents received totaling $50,000.On March 1, 2010, the tenant in apartment 2B paid Bristol$2,000 to cancel the lease

Lake Corp., an accrual-basis calendar-year corporation, had the following 2011 receipts:Advanced rental payments where the lease ends in 2013 $125,000 Lease cancellation payment from a five-year lease tenant 50,000 Lake had no restrictions on the use of the advanced rental payments and renders no

In 2010, Emil Gow won $5,000 in a state lottery. Also in 2010, Emil spent $400 for the purchase of lottery tickets. Emil elected the standard deduction on his 2010 income tax return. The amount of lottery winnings that should be included in Emil’s 2010 taxable income isa. $0b. $2,000c. $4,600d.

In 2011, Joan accepted and received a $10,000 award for outstanding civic achievement. Joan was selected without any action on her part, and no future services are expected of her as a condition of receiving the award. What amount should Joan include in her 2011 adjusted gross income in connection

With regard to the alimony deduction in connection with a 2011 divorce, which one of the following statements is correct?a. Alimony is deductible by the payor spouse, and includible by the payee spouse, to the extent that payment is contingent on the status of the divorced couple’s children.b.

Pierre, a headwaiter, received tips totaling $2,000 in December 2010. On January 5, 2011, Pierre reported this tip income to his employer in the required written statement. At what amount, and in which year, should this tip income be included in Pierre’s gross income?a. $2,000 in 2010.b. $2,000

Mr. and Mrs. Alvin Charak took a foster child, Robert, into their home in 2010. A state welfare agency paid the Charaks $3,900 during the year for related expenses. Actual expenses incurred by the Charaks during 2010 in caring for Robert amounted to $3,000.The remaining $900 was spent by the

The following information is available for Ann Drury for 2010:Salary $36,000 Premiums paid by employer on group-term life insurance in excess of $50,000 500 Proceeds from state lottery 5,000 How much should Drury report as gross income on her 2010 tax return?a. $36,000b. $36,500c. $41,000d. $41,500

Income in respect of a cash-basis decedenta. Covers income earned and collected after a decedent’s death.b. Receives a stepped-up basis in the decedent’s estate.c. Includes a bonus earned before the taxpayer’s death but not collected until after death.d. Must be included in the decedent’s

Ed and Ann Ross were divorced in January 2010. In accordance with the divorce decree, Ed transferred the title in their home to Ann in 2010. The home, which had a fair market value of $150,000, was subject to a $50,000 mortgage that had twenty more years to run.Monthly mortgage payments amount to

In 2006, Ross was granted an incentive stock option (ISO) by her employer as part of an executive compensation package. Ross exercised the ISO in 2009 and sold the stock in 2011 at a gain. Ross was subject to regular tax for the year in which thea. ISO was granted.b. ISO was exercised.c. Stock was

Lee, an attorney, uses the cash receipts and disbursements method of reporting. In 2010, a client gave Lee 500 shares of a listed corporation’s stock in full satisfaction of a $10,000 legal fee the client owed to Lee. This stock had a fair market value of $8,000 on the date it was given to Lee.

Hall, a divorced person and custodian of her twelve-year-old child, submitted the following information to the CPA who prepared her 2010 return:The divorce agreement, executed in 2007, provides for Hall to receive $3,000 per month, of which $600 is designated as child support. After the child

Clark filed Form 1040EZ for the 2010 taxable year. In July 2011, Clark received a state income tax refund of $900, plus interest of $10, for overpayment of 2010 state income tax. What amount of the state tax refund and interest is taxable in Clark’s 2011 federal income tax return?a. $0b. $ 10c.

John and Mary were divorced in 2010. The divorce decree provides that John pay alimony of $10,000 per year, to be reduced by 20% on their child’s 18th birthday. During 2011, John paid$7,000 directly to Mary and $3,000 to Spring College for Mary’s tuition. What amount of these payments should be

Perle, a dentist, billed Wood $600 for dental services. Wood paid Perle $200 cash and built a bookcase for Perle’s office in full settlement of the bill. Wood sells comparable bookcases for $350.What amount should Perle include in taxable income as a result of this transaction?a. $0b. $200c.

With regard to the inclusion of social security benefits in gross income for the 2011 tax year, which of the following statements is correct?a. The social security benefits in excess of modified adjusted gross income are included in gross income.b. The social security benefits in excess of one half

Darr, an employee of Sorce C corporation, is not a shareholder.Which of the following would be included in a taxpayer’s gross income?a. Employer-provided medical insurance coverage under a health plan.b. A $10,000 gift from the taxpayer’s grandparents.c. The fair market value of land that the

Which of the following conditions must be present in a divorce agreement for a payment to qualify as deductible alimony?I. Payments must be in cash.II. The payment must end at the recipient’s deatha. I only.b. II only.c. Both I and II.d. Neither I nor II.

Bob and Sue Stewart were divorced in 2009. Under the terms of their divorce decree, Bob paid alimony to Sue at the rate of $50,000 in 2009, $20,000 in 2010, and nothing in 2011. What amount of alimony recapture must be included in Bob’s gross income for 2011?a. $0b. $23,283c. $30,000d. $32,500

In July 1996, Dan Farley leased a building to Robert Shelter for a period of fifteen years at a monthly rental of $1,000 with no option to renew. At that time the building had a remaining estimated useful life of twenty years.Prior to taking possession of the building, Shelter made improvements at

Majors, a candidate for a graduate degree, received the following scholarship awards from the university in 2011:$10,000 for tuition, fees, books, and supplies required for courses.$2,000 stipend for research services required by the scholarship.What amount of the scholarship awards should Majors

Which payment(s) is (are) included in a recipient’s gross income?I. Payment to a graduate assistant for a part-time teaching assignment at a university. Teaching is not a requirement toward obtaining the degree.II. A grant to a Ph.D. candidate for his participation in a universitysponsored

For the year ended December 31, 2010, Don Raff earned $1,000 interest at Ridge Savings Bank on a certificate of deposit scheduled to mature in 2011. In January 2011, before filing his 2010 income tax return, Raff incurred a forfeiture penalty of $500 for premature withdrawal of the funds. Raff

In 2011 Uriah Stone received the following interest payments:Interest of $400 on refund of federal income tax for 2009.Interest of $300 on award for personal injuries sustained in an automobile accident during 2008.Interest of $1,500 on municipal bonds.Interest of $1,000 on United States savings

Daniel Kelly received interest income from the following sources in 2011:New York Port Authority bonds $1,000 Puerto Rico Commonwealth bonds 1,800 What portion of such interest is tax exempt?a. $0b. $1,000c. $1,800d. $2,800

Clark bought Series EE US Savings Bonds in 2011. Redemption proceeds will be used for payment of college tuition for Clark’s dependent child. One of the conditions that must be met for tax exemption of accumulated interest on these bonds is that thea. Purchaser of the bonds must be the sole owner

Charles and Marcia are married cash-basis taxpayers. In 2011, they had interest income as follows:$500 interest on federal income tax refund.$600 interest on state income tax refund.$800 interest on federal government obligations.$1,000 interest on state government obligations.What amount of

During 2011 Kay received interest income as follows:On US Treasury certificates $4,000 On refund of 2009 federal income tax 500 The total amount of interest subject to tax in Kay’s 2011 tax return isa. $4,500b. $4,000c. $ 500d. $0

In a tax year where the taxpayer pays qualified education expenses, interest income on the redemption of qualified US Series EE Bonds may be excluded from gross income. The exclusion is subject to a modified gross income limitation and a limit of aggregate bond proceeds in excess of qualified

Micro Corp., a calendar-year accrual-basis corporation, purchased a five-year, 8%, $100,000 taxable corporate bond for$108,530 on July 1, 2010, the date the bond was issued. The bond paid interest semiannually. Micro elected to amortize the bond premium. For Micro’s 2010 tax return, the bond

During 2009, Karen purchased 100 shares of preferred stock of Boling Corp. for $5,500. During 2011, Karen received a stock dividend of ten additional shares of Boling Corp. preferred stock. On the date the preferred stock was distributed, it had a fair market value of $60 per share. What is

Jack and Joan Mitchell, married taxpayers and residents of a separate property state, elect to file a joint return for 2011 during which they received the following dividends:Received by Jack Joan Alert Corporation (a qualified, domestic corporation) $400 $ 50 Canadian Mines, Inc. (a Canadian

Amy Finch had the following cash receipts during 2011:Dividend from a mutual insurance company on a life insurance policy $500 Dividend on listed corporation stock; payment date by corporation was 12/30/10, but Amy received the dividend in the mail on 1/2/11 875 Total dividends received to date on

In 2011, Gail Judd received the following dividends from Benefit Life Insurance Co., on Gail’s life insurance policy (Total dividends received have not yet exceeded accumulated premiums paid) $100 Safe National Bank, on bank’s common stock 300 Roe Mfg. Corp., a Delaware corporation, on

On February 1, 2011, Hall learned that he was bequeathed 500 shares of common stock under his father’s will. Hall’s father had paid $2,500 for the stock in 2006. Fair market value of the stock on February 1, 2011, the date of his father’s death, was $4,000 and had increased to $5,500 six

James Martin received the following compensation and fringe benefits from his employer during 2011:Salary $50,000 Year-end bonus 10,000 Medical insurance premiums paid by employer 1,000 Reimbursement of qualified moving expenses 5,000 What amount of the preceding payments should be included in

During the current year Hal Leff sustained a serious injury in the course of his employment. As a result of this injury, Hal received the following payments during the year:Workers’ compensation $2,400 Reimbursement from his employer’s accident and health plan for medical expenses paid by Hal

John Budd files a joint return with his wife. Budd’s employer pays 100% of the cost of all employees’ group-term life insurance under a qualified plan. Under this plan, the maximum amount of tax-free coverage that may be provided for Budd by his employer isa. $100,000b. $ 50,000c. $ 10,000d. $

Howard O’Brien, an employee of Ogden Corporation, died on June 30, 2011. During July, Ogden made employee death payments(which do not represent the proceeds of life insurance) of $10,000 to his widow, and $10,000 to his fifteen-year-old son. What amounts should be included in gross income by the

David Autrey was covered by an $80,000 group-term life insurance policy of which his wife was the beneficiary. Autrey’s employer paid the entire cost of the policy, for which the uniform annual premium was $8 per $1,000 of coverage. Autrey died during 2011, and his wife was paid the $80,000

Under a “cafeteria plan” maintained by an employer,a. Participation must be restricted to employees, and their spouses and minor children.b. At least three years of service are required before an employee can participate in the plan.c. Participants may select their own menu of benefits.d.

Seymour Thomas named his wife, Penelope, the beneficiary of a$100,000 (face amount) insurance policy on his life. The policy provided that upon his death, the proceeds would be paid to Penelope with interest over her present life expectancy, which was calculated at twenty-five years. Seymour died

Fuller was the owner and beneficiary of a $200,000 life insurance policy on a parent. Fuller sold the policy to Decker, for $25,000.Decker paid a total of $40,000 in premiums. Upon the death of the parent, what amount must Decker include in gross income?a. $0b. $135,000c. $160,000d. $200,000

Richard Brown, who retired on May 31, 2010, receives a monthly pension benefit of $700 payable for life. His life expectancy at the date of retirement is ten years. The first pension check was received on June 15, 2010. During his years of employment, Brown contributed $12,000 to the cost of his

Which of the following forms of tenancy will be created if a tenant stays in possession of the leased premises without the landlord’s consent, after the tenant’s one-year written lease expires?a. Tenancy at will.b. Tenancy for years.c. Tenancy from period to period.d. Tenancy at sufferance.

Which of the following methods of obtaining personal property will give the recipient ownership of the property?Lease Finding abandoned propertya. Yes Yesb. Yes Noc. No Yesd. No No

Which of the following rights is (are) generally given to a lessee of residual property?I. A covenant of quiet enjoyment.II. An implied warranty of habitability.a. I only.b. II only.c. Both I and II.d. Neither I nor II.

Which of the following provisions must be included to have an enforceable written residential lease?A description of the leased premises A due date for the payment of renta. Yes Yesb. Yes Noc. No Yesd. No No

Rich purchased property from Sklar for $200,000. Rich obtained a $150,000 loan from Marsh Bank to finance the purchase, executing a promissory note and a mortgage. By recording the mortgage, Marsh protects itsa. Rights against Rich under the promissory note.b. Rights against the claims of

A mortgagor’s right of redemption will be terminated by a judicial foreclosure sale unlessa. The proceeds from the sale are not sufficient to fully satisfy the mortgage debt.b. The mortgage instrument does not provide for a default sale.c. The mortgagee purchases the property for market value.d.

On February 1, Frost bought a building from Elgin, Inc. for$250,000. To complete the purchase, Frost borrowed $200,000 from Independent Bank and gave Independent a mortgage for that amount;gave Elgin a second mortgage for $25,000; and paid $25,000 in cash.Independent recorded its mortgage on

Which of the following conditions must be met to have an enforceable mortgage?a. An accurate description of the property must be included in the mortgage.b. A negotiable promissory note must accompany the mortgage.c. Present consideration must be given in exchange for the mortgage.d. The amount of

Showing 900 - 1000

of 2483

First

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

Last

Step by Step Answers