New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

strategy in practice

Wiley CPA Exam Review Regulation 2012 9th Edition O. Ray Whittington, Patrick R. Delaney - Solutions

Gero Corp. had operating income of $160,000, after deducting$10,000 for contributions to State University, but not including dividends of $2,000 received from nonaffiliated taxable domestic corporations.In computing the maximum allowable deduction for contributions, Gero should apply the percentage

During 2011, Nale Corp. received dividends of $1,000 from a 10%-owned taxable domestic corporation. When Nale computes the maximum allowable deduction for contributions in its 2011 return, the amount of dividends to be included in the computation of taxable income isa. $0b. $ 200c. $ 300d. $1,000

Lyle Corp. is a distributor of pharmaceuticals and sells only to retail drug stores. During 2011, Lyle received unsolicited samples of nonprescription drugs from a manufacturer. Lyle donated these drugs in 2011 to a qualified exempt organization and deducted their fair market value as a charitable

Tapper Corp., an accrual-basis calendar-year corporation, was organized on January 2, 2010. During 2010, revenue was exclusively from sales proceeds and interest income. The following information pertains to Tapper:Taxable income before charitable contributions for the year ended December 31, 2010

In 2010, Cable Corp., a calendar-year C corporation, contributed$80,000 to a qualified charitable organization. Cable’s 2010 taxable income before the deduction for charitable contributions was$820,000 after a $40,000 dividends received deduction. Cable also had carryover contributions of $10,000

During 2010, Jackson Corp. had the following income and expenses:Gross income from operations $100,000 Dividend income from taxable domestic 20%-owned corporations 10,000 Operating expenses 35,000 Officers’ salaries 20,000 Contributions to qualified charitable organizations 8,000 Net operating

Silo Corp. was organized on March 1, 2010, began doing business on September 1, 2010, and elected to file its income tax return on a calendar-year basis. The following qualifying organizational expenditures were incurred in organizing the corporation:July 1, 2010 $3,000 September 3, 2010 5,600 The

The costs of organizing a corporation during 2011a. May be deducted in full in the year in which these costs are incurred if they do not exceed $5,000.b. May be deducted only in the year in which these costs are paid.c. May be amortized over a period of 120 months even if these costs are

Brown Corp., a calendar-year taxpayer, was organized and actively began operations on July 1, 2011, and incurred the following costs:Legal fees to obtain corporate charter $40,000 Commission paid to underwriter 25,000 Temporary directors’ meetings 15,000 State incorporation fees 4,400 For 2011,

Which of the following costs are deductible organizational expenditures?a. Professional fees to issue the corporation’s stock.b. Commissions paid by the corporation to underwriters for stock issue.c. Printing costs to issue the corporation’s stock.d. Expenses of temporary directors meetings.

Pym, Inc., which had earnings and profits of $100,000, distributed land to Kile Corporation, a shareholder. Pym’s adjusted basis for this land was $3,000. The land had a fair market value of$12,000 and was subject to a mortgage liability of $5,000, which was assumed by Kile Corporation. The

During 2011, Ral Corp. exchanged 5,000 shares of its own $10 par common stock for land with a fair market value of $75,000. As a result of this exchange, Ral should report in its 2011 tax returna. $25,000 Section 1245 gain.b. $25,000 Section 1231 gain.c. $25,000 ordinary income.d. No gain.

The following information pertains to treasury stock sold by Lee Corp. to an unrelated broker in 2011:Proceeds received $50,000 Cost 30,000 Par value 9,000 What amount of capital gain should Lee recognize in 2011 on the sale of this treasury stock?a. $0b. $ 8,000c. $20,000d. $30,500

Andi Corp. issued $1,000,000 face amount of bonds in 2002 and established a sinking fund to pay the debt at maturity. The bondholders appointed an independent trustee to invest the sinking fund contributions and to administer the trust. In 2010, the sinking fund earned $60,000 in interest on bank

Which of the following entities must include in gross income 100% of dividends received from unrelated taxable domestic corporations in computing regular taxable income?Personal service corporations Personal holding companiesa. Yes Yesb. No Noc. Yes Nod. No Yes

Bradbury Corp., a calendar-year corporation, was formed on January 2, 2007, and had gross receipts for its first four taxable years as follows:Year Gross receipts 2007 $4,500,000 2008 9,000,000 2009 9,500,000 2010 6,500,000 What is the first taxable year that Bradbury Corp. is not exempt from the

A corporation will not be subject to the alternative minimum tax for calendar year 2011 ifa. The corporation’s net assets do not exceed $7.5 million.b. The corporation’s average annual gross receipts do not exceed$10 million.c. The corporation has less than ten shareholders.d. 2011 is the

In computing its 2011 alternative minimum tax, a corporation must include as an adjustmenta. The dividends received deduction.b. The difference between regular tax depreciation and straight-line depreciation over forty years for real property placed in service in 1998.c. Charitable contributions.d.

A corporation’s tax preference items that must be taken into account for 2011 alternative minimum tax purposes includea. Use of the percentage-of-completion method of accounting for long-term contracts.b. Casualty losses.c. Tax-exempt interest on private activity bonds issued in 2008.d. Capital

Rona Corp.’s 2010 alternative minimum taxable income was$200,000. The exempt portion of Rona’s 2010 alternative minimum taxable income wasa. $0b. $12,500c. $27,500d. $52,500

If a corporation’s tentative minimum tax exceeds the regular tax, the excess amount isa. Carried back to the first preceding taxable year.b. Carried back to the third preceding taxable year.c. Payable in addition to the regular tax.d. Subtracted from the regular tax.

Eastern Corp., a calendar-year corporation, was formed during 2009. On January 3, 2010, Eastern placed five-year property in service. The property was depreciated under the general MACRS system. Eastern did not elect to use the straight-line method, and elected not to use bonus depreciation. The

Green Corp. was incorporated and began business in 2008. In computing its alternative minimum tax for 2009, it determined that it had adjusted current earnings (ACE) of $400,000 and alternative minimum taxable income (prior to the ACE adjustment) of $300,000.For 2010, it had adjusted current

Kisco Corp.’s taxable income for 2010 before taking the dividends received deduction was $70,000. This includes $10,000 in dividends from a 15%-owned taxable domestic corporation. Given the following tax rates, what would Kisco’s income tax be before any credits?Taxable income partial rate

Finbury Corporation’s taxable income for the year ended December 31, 2010, was $2,000,000 on which its tax liability was$680,000. In order for Finbury to escape the estimated tax underpayment penalty for the year ending December 31, 2011, Finbury’s 2011 estimated tax payments must equal at

When computing a corporation’s income tax expense for estimated income tax purposes, which of the following should be taken into account?Corporate tax credits Alternative minimum taxa. No Nob. No Yesc. Yes Nod. Yes Yes

Blink Corp., an accrual-basis calendar-year corporation, carried back a net operating loss for the tax year ended December 31, 2010.Blink’s gross revenues have been under $500,000 since inception.Blink expects to have profits for the tax year ending December 31, 2011. Which method(s) of estimated

A corporation’s penalty for underpaying federal estimated taxes isa. Not deductible.b. Fully deductible in the year paid.c. Fully deductible if reasonable cause can be established for the underpayment.d. Partially deductible.

A corporation’s tax year can be reopened after all statutes of limitations have expired if I. The tax return has a 50% nonfraudulent omission from gross income.II. The corporation prevails in a determination allowing a deduction in an open tax year that was taken erroneously in a closed tax

Edge Corp., a calendar-year C corporation, had a net operating loss and zero tax liability for its 2010 tax year. To avoid the penalty for underpayment of estimated taxes, Edge could compute its first quarter 2011 estimated income tax payment using the Annualized income method Preceding year

Bass Corp., a calendar-year C corporation, made qualifying 2010 estimated tax deposits based on its actual 2009 tax liability. On March 15, 2011, Bass filed a timely automatic extension request for its 2010 corporate income tax return. Estimated tax deposits and the extension payment totaled

A civil fraud penalty can be imposed on a corporation that underpays tax bya. Omitting income as a result of inadequate recordkeeping.b. Failing to report income it erroneously considered not to be part of corporate profits.c. Filing an incomplete return with an appended statement, making clear

She transferred property having an adjusted basis of $80,000 and a fair market value of $60,000, and in exchange received Sec. 1244 small business corporation stock. During February 2011, Nancy sold all of her stock for $35,000. What is the amount and character of Nancy’s recognized loss

Nancy, who is single, formed a corporation during 2006 using a tax-free asset transfer that qualified under Sec.

During the current year, Dinah sold Sec. 1244 small business corporation stock that she owned for a loss of $125,000. Assuming Dinah is married and files a joint income tax return for 2011, what is the character of Dinah’s recognized loss from the sale of the stock?a. $125,000 capital loss.b.

Which of the following is not a requirement for stock to qualify as Sec. 1244 small business corporation stock?a. The stock must be issued to an individual or to a partnership.b. The stock was issued for money or property (other than stock and securities).c. The stock must be common stock.d. The

Jackson, a single individual, inherited Bean Corp. common stock from Jackson’s parents. Bean is a qualified small business corporation under Code Sec. 1244. The stock cost Jackson’s parents$20,000 and had a fair market value of $25,000 at the parents’ date of death. During the year, Bean

Roberta Warner and Sally Rogers formed the Acme Corporation on October 1, 2011. On the same date Warner paid $75,000 cash to Acme for 750 shares of its common stock. Simultaneously, Rogers received 100 shares of Acme’s common stock for services rendered.How much should Rogers include as taxable

Rela Associates, a partnership, transferred all of its assets, with a basis of $300,000, along with liabilities of $50,000, to a newly formed corporation in return for all of the corporation’s stock. The corporation assumed the liabilities. Rela then distributed the corporation’s stock to its

Feld, the sole stockholder of Maki Corp., paid $50,000 for Maki’s stock in 2005. In 2011, Feld contributed a parcel of land to Maki but was not given any additional stock for this contribution. Feld’s basis for the land was $10,000, and its fair market value was $18,000 on the date of the

Jones incorporated a sole proprietorship by exchanging all the proprietorship’s assets for the stock of Nu Co., a new corporation. To qualify for tax-free incorporation, Jones must be in control of Nu immediately after the exchange. What percentage of Nu’s stock must Jones own to qualify as

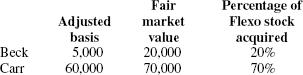

Adams, Beck, and Carr organized Flexo Corp. with authorized voting common stock of $100,000. Adams received 10% of the capital stock in payment for the organizational services that he rendered for the benefit of the newly formed corporation. Adams did not contribute property to Flexo and was under

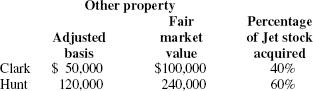

Clark and Hunt organized Jet Corp. with authorized voting common stock of $400,000. Clark contributed $60,000 cash. Both Clark and Hunt transferred other property in exchange for Jet stock as follows:What was Clark’s basis in Jet stock?a. $0b. $100,000c. $110,000d. $160,000 Other property Fair

Alan, Baker, and Carr formed Dexter Corporation during 2011.Pursuant to the incorporation agreement, Alan transferred property with an adjusted basis of $30,000 and a fair market value of $45,000 for 450 shares of stock, Baker transferred cash of $35,000 in exchange for 350 shares of stock, and

John Albin is a retired partner of Brill & Crum, a personal service partnership. Albin has not rendered any ser-vices to Brill &Crum since his retirement in 2009. Under the provisions of Albin’s retirement agreement, Brill & Crum is obligated to pay Albin 10% of the partnership’s net income

For tax purposes, a retiring partner who receives retirement payments ceases to be regarded as a partnera. On the last day of the taxable year in which the partner retires.b. On the last day of the particular month in which the partner retires.c. The day on which the partner retires.d. Only after

In 2006, Lisa Bara acquired a one-third interest in Dee Associates, a partnership. In 2011, when Lisa’s entire interest in the partnership was liquidated, Dee’s assets consisted of the following:cash, $20,000 and tangible property with a basis of $46,000 and a fair market value of $40,000. Dee

If this distribution were in complete liquidation of Reed’s interest in Post, Reed’s recognized gain or loss resulting from the distribution would bea. $7,500 gain.b. $9,000 lossc. $1,500 loss.d. $0.

If this distribution were nonliquidating, Reed’s basis for the inventory would bea. $14,000b. $12,500c. $ 5,000d. $ 1,500

The basis to a partner of property distributed “in kind” in complete liquidation of the partner’s interest is thea. Adjusted basis of the partner’s interest increased by any cash distributed to the partner in the same transaction.b. Adjusted basis of the partner’s interest reduced by any

On June 30, 2011, Berk, a calendar-year taxpayer, retired from his partnership. At that time, his capital account was $50,000 and his share of the partnership’s liabilities was $30,000. Berk’s retirement payments consisted of being relieved of his share of the partnership liabilities and

What is Jody’s basis in the distributed property?a. $0b. $30,000c. $35,000d. $40,000

What amount of taxable gain must Jody report as a result of this distribution?a. $0b. $ 5,000c. $10,000d. $20,000

Day’s adjusted basis in LMN Partnership interest is $50,000.During the year Day received a nonliquidating distribution of$25,000 cash plus land with an adjusted basis of $15,000 to LMN, and a fair market value of $20,000. How much is Day’s basis in the land?a. $10,000b. $15,000c. $20,000d.

Hart’s adjusted basis in Best Partnership was $9,000 at the time he received the following nonliquidating distribution of partnership property:Cash $ 5,000 Land Adjusted basis 7,000 Fair market value 10,000 What was the amount of Hart’s basis in the land?a. $0b. $ 4,000c. $ 7,000d. $10,000

Curry’s adjusted basis in Vantage Partnership was $5,000 at the time he received a nonliquidating distribution of land. The land had an adjusted basis of $6,000 and a fair market value of $9,000 to Vantage. What was the amount of Curry’s basis in the land?a. $9,000b. $6,000c. $5,000d. $1,000

Stone and Frazier decided to terminate the Woodwest Partnership as of December 31.On that date, Woodwest’s balance sheet was as follows:Cash $2,000 Land (adjusted basis) 2,000 Capital—Stone 3,000 Capital—Frazier 1,000 The fair market value of the land was $3,000. Frazier’s outside basis in

On June 30, 2011, James Roe sold his interest in the calendaryear partnership of Roe & Doe for $30,000. Roe’s adjusted basis in Roe & Doe at June 30, 2011, was $7,500 before apportionment of any 2011 partnership income. Roe’s distributive share of partnership income up to June 30, 2011, was

On April 1, 2010, George Hart, Jr. acquired a 25% interest in the Wilson, Hart, and Company partnership by gift from his father. The partnership interest had been acquired by a $50,000 cash investment by Hart, Sr. on July 1, 2004. The tax basis of Hart, Sr.’s partnership interest was $60,000 at

What amount of ordinary income should Carr report in his 2011 income tax return on the sale of his partnership interest?a. $0b. $ 20,000c. $ 34,000d. $140,000

What was the total amount realized by Carr on the sale of his partnership interest?a. $174,000b. $154,000c. $140,000d. $134,000

On December 31, 2010, after receipt of his share of partnership income, Clark sold his interest in a limited partnership for $30,000 cash and relief of all liabilities. On that date, the adjusted basis of Clark’s partnership interest was $40,000, consisting of his capital account of $15,000 and

David Beck and Walter Crocker were equal partners in the calendar-year partnership of Beck & Crocker. On July 1, 2010, Beck died. Beck’s estate became the successor in interest and continued to share in Beck & Crocker’s profits until Beck’s entire partnership interest was liquidated on April

Under which of the following circumstances is a partnership that is not an electing large partnership considered terminated for income tax purposes?I. Fifty-five percent of the total interest in partnership capital and profits is sold within a twelve-month period.II. The partnership’s business

Partnership Abel, Benz, Clark & Day is in the real estate and insurance business. Abel owns a 40% interest in the capital and profits of the partnership, while Benz, Clark, and Day each owns a 20% interest. All use a calendar year. At November 1, 2010, the real estate and insurance business is

Cobb, Danver, and Evans each owned a one-third interest in the capital and profits of their calendar-year partnership. On September 18, 2010, Cobb and Danver sold their partnership interests to Frank, and immediately withdrew from all participation in the partnership.On March 15, 2011, Cobb and

Curry’s sale of her partnership interest causes a partnership termination. The partnership’s business and financial operations are continued by the other members. What is (are) the effect(s) of the termination?I. There is a deemed distribution of assets to the remaining partners and the

On January 3, 2010, the partners’ interests in the capital, profits, and losses of Able Partnership were% of capital profits and losses Dean 25%Poe 30%Ritt 45%On February 4, 2010, Poe sold her entire interest to an unrelated person. Dean sold his 25% interest in Able to another unrelated person

Irving Aster, Dennis Brill, and Robert Clark were partners who shared profits and losses equally. On February 28, 2011, Aster sold his interest to Phil Dexter. On March 31, 2011, Brill died, and his estate held his interest for the remainder of the year. The partnership continued to operate and for

Without obtaining prior approval from the IRS, a newly formed partnership may adopta. A taxable year which is the same as that used by one or more of its partners owning an aggregate interest of more than 50% in profits and capital.b. A calendar year, only if it comprises a twelve-month period.c. A

Which one of the following statements regarding a partnership’s tax year is correct?a. A partnership formed on July 1 is required to adopt a tax year ending on June 30.b. A partnership may elect to have a tax year other than the generally required tax year if the deferral period for the tax year

Under Section 444 of the Internal Revenue Code, certain partnerships can elect to use a tax year different from their required tax year. One of the conditions for eligibility to make a Section 444 election is that the partnership musta. Be a limited partnership.b. Be a member of a tiered

Gladys Peel owns a 50% interest in the capital and profits of the partnership of Peel and Poe. On July 1, 2010, Peel bought land the partnership had used in its business for its fair market value of$10,000. The partnership had acquired the land five years ago for$16,000. For the year ended December

Kay Shea owns a 55% interest in the capital and profits of Dexter Communications, a partnership. In 2011, Kay sold an oriental lamp to Dexter for $5,000. Kay bought this lamp in 2005 for her personal use at a cost of $1,000 and had used the lamp continuously in her home until the lamp was sold to

In March 2011, Lou Cole bought 100 shares of a listed stock for$10,000. In May 2011, Cole sold this stock for its fair market value of $16,000 to the partnership of Rook, Cole & Clive. Cole owned a one-third interest in this partnership. In Cole’s 2011 tax return, what amount should be reported

Doris and Lydia are sisters and also are equal partners in the capital and profits of Agee & Nolan. The following information pertains to 300 shares of Mast Corp. stock sold by Lydia to Agee &Nolan.Year of purchase 2004 Year of sale 2011 Basis (cost) $9,000 Sales price (equal to fair market value)

Hall and Haig are equal partners in the firm of Arosa Associates.On January 1, 2010, each partner’s adjusted basis in Arosa was$40,000. During 2010 Arosa borrowed $60,000, for which Hall and Haig are personally liable. Arosa sustained an operating loss of$10,000 for the year ended December 31,

Which of the following should be used in computing the basis of a partner’s interest acquired from another partner?Cash paid by transferee to transferor Transferee’s share of partnership liabilitiesa. No Yesb. Yes Noc. No Nod. Yes Yes

Lee inherited a partnership interest from Dale during 2011. The adjusted basis of Dale’s partnership interest was $50,000, and its fair market value on the date of Dale’s death (the estate valuation date)was $70,000. What was Lee’s original basis for the partnership interest?a. $70,000b.

On January 1, 2011, Kane was a 25% equal partner in Maze General Partnership, which had partnership liabilities of $300,000.On January 2, 2011, a new partner was admitted and Kane’s interest was reduced to 20%. On April 1, 2011, Maze repaid a $100,000 general partnership loan. Ignoring any

Gray is a 50% partner in Fabco Partnership. Gray’s tax basis in Fabco on January 1, 2010, was $5,000. Fabco made no distributions to the partners during 2010, and recorded the following:Ordinary income $20,000 Tax exempt income 8,000 Portfolio income 4,000 What is Gray’s tax basis in Fabco on

On January 4, 2011, Smith and White contributed $4,000 and$6,000 in cash, respectively, and formed the Macro General Partnership. The partnership agreement allocated profits and losses 40% to Smith and 60% to White. In 2011, Macro purchased property from an unrelated seller for $10,000 cash and a

Dean is a 25% partner in Target Partnership. Dean’s tax basis in Target on January 1, 2010, was $20,000. At the end of 2010, Dean received a nonliquidating cash distribution of $8,000 from Target.Target’s 2010 accounts recorded the following items:Municipal bond interest income $12,000 Ordinary

Peters has a one-third interest in the Spano Partnership. During 2010, Peters received a $16,000 guaranteed payment, which was deductible by the partnership, for services rendered to Spano. Spano reported a 2010 operating loss of $70,000 before the guaranteed payment. What is (are) the net

What is Miles’s tax basis in Decor on December 31, 2010?a. $211,250b. $215,000c. $218,750d. $222,500

What total amount from Decor is includible in Flagg’s 2010 tax return?a. $15,000b. $18,750c. $22,500d. $37,500

What was Jones’ initial basis in the partnership interest?a. $51,000b. $45,000c. $39,000d. $33,000

What was Curry’s initial basis in the partnership interest?a. $45,000b. $30,000c. $24,000d. $18,000

On December 31, 2009, Edward Baker gave his son, Allan, a gift of a 50% interest in a partnership in which capital is a material income-producing factor. For the year ended December 31, 2010, the partnership’s ordinary income was $100,000. Edward and Allan were the only partners in 2010. There

Gilroy, a calendar-year taxpayer, is a partner in the firm of Adams and Company which has a fiscal year ending June 30.The partnership agreement provides for Gilroy to receive 25% of the ordinary income of the partnership. Gilroy also receives a guaranteed payment of $1,000 monthly which is

At December 31, 2009, Alan and Baker were equal partners in a partnership with net assets having a tax basis and fair market value of $100,000. On January 1, 2010, Carr contributed securities with a fair market value of $50,000 (purchased in 2008 at a cost of $35,000)to become an equal partner in

Dale’s distributive share of income from the calendar-year partnership of Dale & Eck was $50,000 in 2010. On December 15, 2010, Dale, who is a cash-basis taxpayer, received a $27,000 distribution of the partnership’s 2010 income, with the $23,000 balance paid to Dale in February 2011. In

Under the Internal Revenue Code sections pertaining to partnerships, guaranteed payments are payments to partners fora. Payments of principal on secured notes honored at maturity.b. Timely payments of periodic interest on bona fide loans that are not treated as partners’ capital.c. Services or

The method used to depreciate partnership property is an election made bya. The partnership and must be the same method used by the“principal partner.”b. The partnership and may be any method approved by the IRS.c. The “principal partner.”d. Each individual partner.

Guaranteed payments made by a partnership to partners for services rendered to the partnership, that are deductible business expenses under the Internal Revenue Code, are I. Deductible expenses on the US Partnership Return of Income, Form 1065, in order to arrive at partnership income (loss).II.

On January 2, 2010, Arch and Bean contribute cash equally to form the JK Partnership. Arch and Bean share profits and losses in a ratio of 75% to 25%, respectively. For 2010, the partnership’s ordinary income was $40,000. A distribution of $5,000 was made to Arch during 2010. What amount of

Chris, a 25% partner in Vista partnership, received a $20,000 guaranteed payment in 2010 for deductible services rendered to the partnership. Guaranteed payments were not made to any other partner. Vista’s 2010 partnership income consisted of Net business income before guaranteed payments $80,000

A guaranteed payment by a partnership to a partner for services rendered, may include an agreement to pay I. A salary of $5,000 monthly without regard to partnership income.II. A 25% interest in partnership profits.a. I only.b. II only.c. Both I and II.d. Neither I nor II.

The partnership of Felix and Oscar had the following items of income during the taxable year ended December 31, 2010.Income from operations $156,000 Tax-exempt interest income 8,000 Dividends from foreign corporations 6,000 Net rental income 12,000 What is the total ordinary income of the

The partnership of Martin & Clark sustained an ordinary loss of$84,000 in 2010. The partnership, as well as the two partners, are on a calendar-year basis. The partners share profits and losses equally.At December 31, 2010, Clark, who materially participates in the partnership’s business, had an

Showing 600 - 700

of 2483

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

Last

Step by Step Answers