We examine the pricing of a semiannual pay, one-year credit default swap (CDS). The premium payments are

Question:

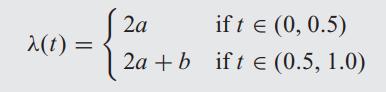

We examine the pricing of a semiannual pay, one-year credit default swap (CDS). The premium payments are made at the beginning of each semiannual period, and default payments are made at the end of each period. The default intensity is given by the following function

The CDS spreads for a half year and one year are

![]()

The risk-free rate is r = 0.01 and the recovery rate is φ = 0.6. Recovery is a fraction of par. Solve for a, b assuming the CDS contracts are fairly priced.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

We begin with the halfyear CDS At inception the premium payment is 5 s05 for a half year Thus the pa...View the full answer

Answered By

Ankur Gupta

I have a degree in finance from a well-renowned university and I have been working in the financial industry for over 10 years now. I have a lot of experience in financial management, and I have been teaching financial management courses at the university level for the past 5 years. I am extremely passionate about helping students learn and understand financial management, and I firmly believe that I have the necessary skills and knowledge to effectively tutor students in this subject.

2+ Reviews

10+ Question Solved

Related Book For

Question Posted: