Question: Suppose you express the CobbDouglas model given in Eq. (7.9.1) as follows: Y i = β 1 Xβ 2 2i X β 3 3i u

Suppose you express the Cobb€“Douglas model given in Eq. (7.9.1) as follows:

Yi = β1Xβ22i X β33i ui

If you take the log-transform of this model, you will have ln ui as the disturbance term on the right-hand side.

a. What probabilistic assumptions do you have to make about ln ui to be able to apply the classical normal linear regression model (CNLRM)? How would you test this with the data given in the following?

b. Do the same assumptions apply to ui ? Why or why not?

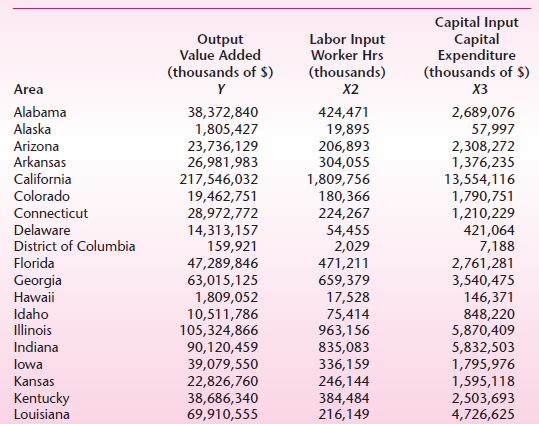

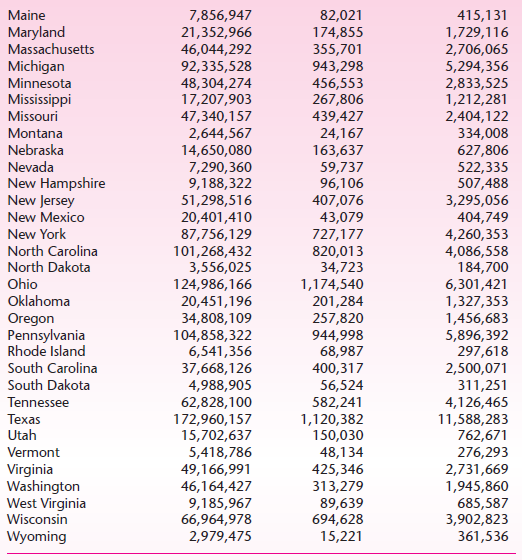

Capital Input Capital Expenditure (thousands of $) X Labor Input Worker Hrs (thousands) X2 Output Value Added (thousands of $) Area Alabama 38,372,840 1,805,427 23,736,129 26,981,983 217,546,032 19,462,751 28,972,772 14,313,157 159,921 47,289,846 63,015,125 1,809,052 10,511,786 105,324,866 90,120,459 39,079,550 22,826,760 38,686,340 69,910,555 424,471 19,895 206,893 304,055 1,809,756 180,366 224,267 54,455 2,029 471,211 659,379 17,528 75,414 963,156 835,083 336,159 246,144 384,484 216,149 2,689,076 57,997 2,308,272 1,376,235 13,554,116 1,790,751 1,210,229 421,064 7,188 2,761,281 3,540,475 146,371 848,220 5,870,409 5,832,503 1,795,976 1,595,118 2,503,693 4,726,625 Alaska Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Hawaii Idaho illinois Indiana lowa Kansas Kentucky Louisiana Maine 7,856,947 21,352,966 46,044,292 92,335,528 48,304,274 17,207,903 47,340,157 2,644,567 14,650,080 7,290,360 9,188,322 51,298,516 20,401,410 87,756,129 101,268,432 3,556,025 124,986,166 20,451,196 34,808,109 104,858,322 6,541,356 37,668,126 4,988,905 62,828,100 172,960,157 15,702,637 5,418,786 49,166,991 46,164,427 9,185,967 66,964,978 2,979,475 82,021 174,855 355,701 943,298 456,553 267,806 439,427 24,167 163,637 59,737 96,106 407,076 43,079 727,177 820,013 34,723 1,174,540 201,284 257,820 944,998 68,987 400,317 56,524 582,241 1,120,382 150,030 48,134 425,346 313,279 89,639 694,628 15,221 415,131 1,729,116 2,706,065 5,294,356 2,833,525 1,212,281 2,404,122 334,008 627,806 522,335 507,488 3,295,056 404,749 4,260,353 4,086,558 184,700 6,301,421 1,327,353 1,456,683 5,896,392 297,618 2,500,071 311,251 4,126,465 11,588,283 762,671 276,293 2,731,669 1,945,860 685,587 3,902,823 361,536 Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee as Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming

Step by Step Solution

3.38 Rating (170 Votes )

There are 3 Steps involved in it

a As discussed in Sec 69 to use the classical normal ... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (2 attachments)

1529_605d88e1cea2f_656278.pdf

180 KBs PDF File

1529_605d88e1cea2f_656278.docx

120 KBs Word File