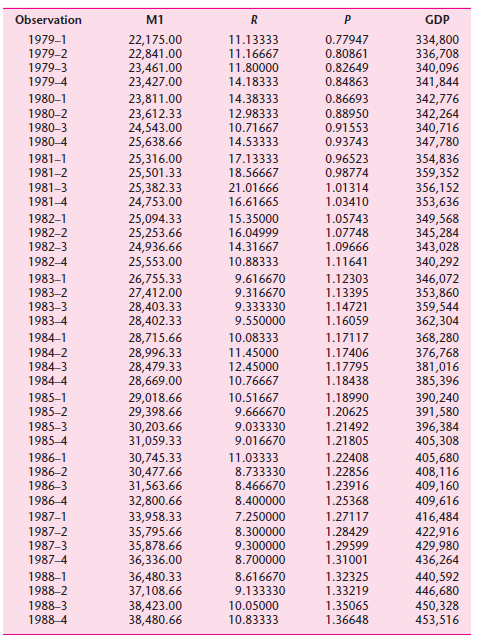

Question: Using the Canadian data given in the following table, find out if M1 and R are stationary random variables. If not, are they cointegrated? Show

Observation M1 GDP 22,175.00 22,841.00 23,461.00 23,427.00 1979-1 11.13333 0.77947 334,800 336,708 340,096 341,844 342,776 342,264 340,716 347,780 354,836 359,352 356,152 353,636 1979-2 11.16667 0.80861 0.82649 0.84863 1979-3 11.80000 1979-4 14.18333 0.86693 19801 23,811.00 23,612.33 24,543.00 25,638.66 14.38333 19802 12.98333 0.88950 0.91553 0.93743 19803 10.71667 1980-4 14.53333 19811 25,316.00 25,501.33 25,382.33 24,753.00 17.13333 0.96523 1981-2 18.56667 0.98774 1981-3 21.01666 1.01314 1981-4 16.61665 1.03410 25,094.33 25,253.66 24,936.66 25,553.00 19821 15.35000 1.05743 349,568 345,284 343,028 340,292 16.04999 14.31667 19822 1.07748 19823 1.09666 19824 10.88333 1.11641 19831 26,755.33 27,412.00 28,403.33 28,402.33 9.616670 1.12303 346,072 353,860 359,544 362,304 9.316670 19832 1.13395 1983-3 9.333330 1.14721 1.16059 1983-4 9.550000 1.17117 1.17406 19841 28,715.66 28,996.33 28,479.33 28,669.00 10.08333 368,280 376,768 381,016 385,396 1984-2 11.45000 1984-3 12.45000 10.76667 1.17795 1984-4 1.18438 19851 29,018.66 29,398.66 30,203.66 31,059.33 10.51667 1.18990 390,240 391,580 396,384 405,308 1985-2 9.666670 1.20625 19853 1985-4 9.033330 1.21492 1.21805 9.016670 405,680 408,116 409,160 409,616 416,484 422,916 429,980 436,264 19861 30,745.33 30,477.66 31,563.66 32,800.66 33,958.33 35,795.66 35,878.66 36,336.00 11.03333 1.22408 19862 8.733330 1.22856 19863 8.466670 1.23916 1986-4 8.400000 1.25368 19871 7.250000 1.27117 1987-2 8.300000 1.28429 1987-3 9.300000 8.700000 1.29599 1987-4 1.31001 19881 36,480.33 37,108.66 38,423.00 38,480.66 8.616670 1.32325 440,592 446,680 450,328 453,516 1988-2 1988-3 1988-4 9.133330 1.33219 10.05000 1.35065 10.83333 1.36648

Step by Step Solution

3.41 Rating (170 Votes )

There are 3 Steps involved in it

In the level form M1 is nonstationary on the basis of the DF test in its various form... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (2 attachments)

1529_605d88e1e0735_666615.pdf

180 KBs PDF File

1529_605d88e1e0735_666615.docx

120 KBs Word File