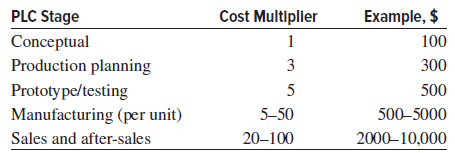

Question: Cost increases imposed by design changes introduced at different times during advancing stages of the product life cycle (PLC) usually rise dramatically as the change

Hamound Industries designed, developed, and is now manufacturing for sales an improved version of its model GR1 smoke detector system that can be used on high speed trains, such as the TGV (Train à Grande Vitesse in French). The original estimates, developed during the conceptual design stage, are shown below. During the testing stage, a major safety flaw was discovered and significant design changes were made, affecting only the equipment first cost estimate, fortunately. Now, during manufacturing, a significant problem has emerged that makes the internet-connectivity feature difficult to manufacture with the level of required reliability. This change will increase the manufacturing cost per unit by a factor of 5. The initial economic analysis, conducted during the conceptual stage, using the AW value at i = 7 per year, showed very promising results. However, the design changes have affected this positive analysis. Use the original estimates and the PLC cost multipliers summarized above to perform AW analyses for the four stages from conceptual through manufacturing to determine what has happened to the economic viability of the improved product.

Equipment original first cost P, $ ........................ˆ’6,000,000

Equipment AOC, $ per year ....................................ˆ’300,000

Manufacturing cost, $ per unit .......................................2.75

Revenue, $ per unit .......................................................12.75

Number of units per year ........................................500,000

Life, years ............................................................................10

Salvage value, $ ...................................................Constant at 10% of original P

Example, $ PLC Stage Conceptual Production planning Prototy pe/testing Manufacturing (per unit) Sales and after-sales Cost Multipller 100 3 300 500 5-50 500-5000 20100 200010,000 TGV

Step by Step Solution

3.49 Rating (172 Votes )

There are 3 Steps involved in it

Testing stage Equipment first cost increases to 30000000 S remains at 600000 Manufacturing stage ... View full answer

Get step-by-step solutions from verified subject matter experts