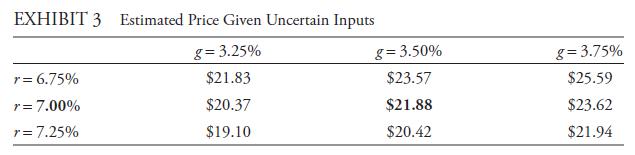

In Example 6, the Gordon growth model value for MSEX was estimated as ($21.88) based on a

Question:

In Example 6, the Gordon growth model value for MSEX was estimated as \($21.88\) based on a current dividend of \($0.74\), an expected dividend growth rate of 3.5 percent, and a required return on equity of 7.00 percent. What if the estimates of r and g can each vary by 25 basis points? How sensitive is the model value to changes in the estimates of r and g? Exhibit 3 provides information on this sensitivity.

A point of interest following from the mathematics of the Gordon growth model is that when the spread between r and g is the widest (r = 7.25 percent and g = 3.25 percent), the Gordon growth model value is the smallest (\($19.10\)), and when the spread is the narrowest (r = 6.75 percent and g = 3.75 percent), the model value is the largest (\($25.59\)).

As the spread goes to zero, in fact, the model value increases without bound. The largest value in Exhibit 3, \($25.59\), is almost 34 percent larger than the smallest value, \($19.10\).

Two-thirds of the values in Exhibit 3 exceed MSEX’s current market price of \($20.50\), tending to support the conclusion that MSEX is undervalued. In summary, the best estimate of the value of MSEX given the assumptions is \($21.88\), bolded in Exhibit 3, but the estimate is quite sensitive to rather small changes in inputs.

Data From Example 6:-

As an analyst for a US domestic equity–income mutual fund, Roberta Kim is evaluating Middlesex Water Company (NASDAQ: MSEX), a publicly traded water utility, for possible inclusion in the approved list of investments. Kim is conducting the analysis in mid-2013.

Not all countries have traded water utility stocks. In the United States, about 85 percent of the population gets its water from government entities. A group of investor-

owned water utilities, however, also supplies water to the public. With a market capitalization of about \($327\) million as of mid-2013, MSEX is among the ten largest publicly traded US water utilities. MSEX’s historical base is the Middlesex System, serving residential, industrial, and commercial customers in a well-developed area of central New Jersey. Through various subsidiaries, MSEX also provides water and wastewater collection and treatment services to areas of southern New Jersey and Delaware.

Hampered by a decline in earnings during the recent recession, net income growth during the past five years has been somewhat less than 2 percent. During the last five years, MSEX’s return on equity averaged 7.8 percent with relatively little variation, and its profit margins are above industry averages. Because MSEX obtains most of its revenue from the regulated business providing an important staple, water, to a relatively stable population, Kim feels confident in forecasting future earnings and dividend growth. MSEX appears to have a policy of small annual increases in the dividend rate, maintaining an average dividend payout ratio of approximately 80 percent. Other facts and forecasts include the following:

• MSEX’s per-share dividends for 2012 (D0) were \($0.74\).

• Kim forecasts a long-term earnings growth rate of 3.5 percent per year, somewhat above the 2.7 percent consensus 3–5-year earnings growth rate forecast reported by Zacks Investment Research (based on two analysts).

• MSEX’s raw beta and adjusted beta are, respectively, 0.70 and 0.80 based on 60 monthly returns. The R2 associated with beta, however, is under 20 percent.

• Kim estimates that MSEX’s pretax cost of debt is 5.6 percent based on Standard &

Poor’s issuer rating for MSEX of A− and the current corporate yield curve.

• Kim’s estimate of MSEX’s required return on equity is 7.00 percent.

• MSEX’s current market price is \($20.50\).

i. Calculate the Gordon growth model estimate of value for MSEX using Kim’s required return on equity estimate.

ii. State whether MSEX appears to be overvalued, fairly valued, or undervalued based on the Gordon growth model estimate of value.

iii. Justify the selection of the Gordon growth model for valuing MSEX.

iv. Calculate the CAPM estimate of the required return on equity for MSEX under the assumption that beta regresses to the mean. (Assume an equity risk premium of 4.5 percent and a risk-free rate of 3 percent as of the price quotation date.)

v. Calculate the Gordon growth estimate of value using A) the required return on equity from your answer to Question 4, and B) a bond-yield-plus-risk-premium approach with a risk premium of 2.5 percent.

vi. Evaluate the effect of uncertainty in MSEX’s required return on equity on the valuation conclusion in Question 2.

Step by Step Answer: