Consider an individual asset, with random holding period return (r_{i}), and the market portfolio, with corresponding return

Question:

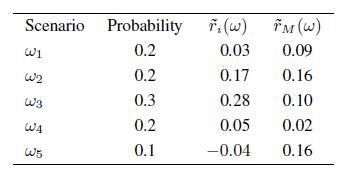

Consider an individual asset, with random holding period return \(r_{i}\), and the market portfolio, with corresponding return \(r_{M}\). We describe uncertainty by five discrete scenarios, as in the following table:

- Assuming that CAPM holds, find the risk-free return.

- Does the result look sensible? If not, how can you explain the anomaly?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Joseph Kabuga Njenga

I am becoming an expert through solving questions from past year.I am doing part time job and also show the talents of our country.I am feeling proud to be an indian and teaching students.

0 Reviews

10+ Question Solved

Related Book For

An Introduction To Financial Markets A Quantitative Approach

ISBN: 9781118014776

1st Edition

Authors: Paolo Brandimarte

Question Posted: