As shown in this chapter, Merton (1973) shows that for the case of an asset with price

Question:

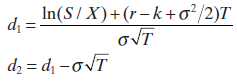

As shown in this chapter, Merton (1973) shows that for the case of an asset with price S paying a continuously compounded dividend yield k , this leads to the following call option pricing formula:C = Se?kTN(d1) ? Xe?rTN(d2),where

a. Modify the BSCall and BSPut functions defined in this chapter to fit the Merton model.

b. Use the function to price an at-the-money option on an index whose current price is S = 1500, when the option?s maturity T = 1, the dividend yield is k = 2.2%, its standard deviation ? = 20%, and the interest rate r = 7%.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a Heres how we can modify the BSCall and BSPut functions defined in the chapter to fit the Merton mo...View the full answer

Answered By

Aruna Mohandas

I have experience in tutoring students on various aspects of communication, such as how to structure and deliver effective presentations, how to improve their writing skills, and how to communicate effectively in a professional setting.

I am skilled in providing personalized feedback and guidance to help students improve their communication skills. I can analyze their communication styles and identify areas where they can improve, and provide practical strategies and exercises to help them achieve their goals.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: