Question: Analyze each case and choose a letter code under each category (type and approach) to indicate the preferable accounting for each case. a. A private

Analyze each case and choose a letter code under each category (type and approach) to indicate the preferable accounting for each case.

a. A private company changed from the percentage-of-completion method to completed-contract method for all contracts currently in process and for all new contracts. All prior balances

can be reconstructed.

b. Changed the measurement method for asset retirement obligations to present value basis instead of undiscounted estimated costs.

c. Changed from FIFO to average cost for inventory to reduce accounting costs. Only the previous year’s opening balance can be reconstructed.

d. Changed depreciation method from declining-balance to straight-line to conform with industry practice.

e. Discovered that a $400,000 acquisition of machinery two years ago had been debited to the land account.

f. Changed from cost method to revaluation method for capital assets; prior years’ valuations are obtainable.

g. Wrote off development costs accumulated and capitalized in two previous years due to serious doubts about the project’s viability.

h. Changed from historical cost to net realizable value for inventory valuation to comply with new accounting standards. The opening balance cannot be reconstructed.

i. Changed residual value of an intangible capital asset to zero based on new economic circumstances.

j. Discovered a transposition error in the previous year’s opening inventory: $17,200; should have been $71,200.

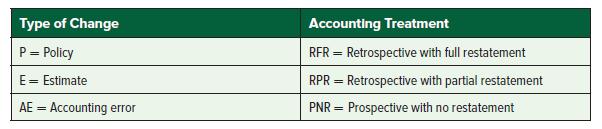

Type of Change P = Policy E = Estimate AE = Accounting error Accounting Treatment RFR = Retrospective with full restatement RPR = Retrospective with partial restatement PNR = Prospective with no restatement

Step by Step Solution

3.42 Rating (155 Votes )

There are 3 Steps involved in it

This is an accounting error not a change in policy because asset retirement obligations always ... View full answer

Get step-by-step solutions from verified subject matter experts