Question: Use the information for P20-21. Instructions Under Option 2: (a) Assume that at the signing of the original lease, Sanderson Inc. has no intention of

Use the information for P20-21.

Instructions

Under Option 2:

(a) Assume that at the signing of the original lease, Sanderson Inc. has no intention of exercising the lease renewal.Determine the classification of the three-year lease for BMW Canada, which follows IFRS 16.

(b) Prepare the journal entry to show how BMW Canada records the collection of the first lease payment on January 1,2017.

(c) Assume now that Sanderson Inc. signs the renewal option at the same time that it enters into the original lease agreement.

1. Prepare a lease amortization schedule including the renewal period for BMW Canada.

2. Determine the classification of the lease for BMW Canada.

3. Record all of the necessary transactions on January 1, 2017 for the first two lease payments collected and for anyadjusting journal entries at the end of the fiscal year ending December 31, 2017 for BMW Canada.

Data From P20-21:

Sanderson Inc., a pharmaceutical distribution firm, is providing a BMW car for its chief executive officer as part of a remuneration package. Sanderson has a calendar year end, issues financial statements annually, and follows ASPE. You have been assigned the task of calculating and reporting the financial statement effect of several options Sanderson is considering in obtaining the vehicle for its CEO.

Option 1: Obtain financing from Western Bank to finance an outright purchase of the BMW from BMW Canada, which regularly sells and leases luxury vehicles.

Option 2: Sign a lease with BMW Canada and exercise the option to renew the lease at the end of the initial term.

Option 3: Sign a lease with BMW Canada and exercise the option to purchase at the end of the lease. The amount of the option price is financed with a bank loan.

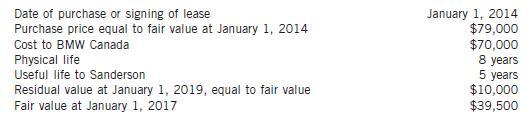

For the purpose of your comparison, you can assume a January 1, 2014 purchase and you can also exclude all amounts for any provincial sales taxes, GST, and HST on all the proposed transactions. You can also assume that Sanderson uses the straight-line method of depreciating automobiles. Assume that for options 1 and 2, the BMW is sold on January 1, 2019, for $10,000.

Sanderson does not expect to incur any extra kilometre charges because it is likely that the BMW won’t be driven that much by the CEO. However, there is a 10% chance that an extra 10,000 km will be driven and a 15% chance that an extra 20,000 km will be used.

Terms and values concerning the asset that are common to all options are the following:

Borrowing terms with Western Bank for purchase: Option 1

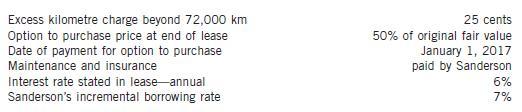

For Option 2:

Terms, conditions, and other information related to the initial lease with BMW Canada:

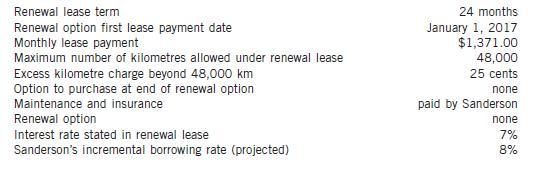

Terms, conditions, and other information related to the renewal option for lease with BMW Canada:

Borrowing terms with Western Bank to exercise option to purchase: Option 3

Step by Step Solution

3.47 Rating (173 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts