Klarke plc acquired a subsidiary, Cameroon Ltd, on 1 October 2017. The statements of financial position of

Question:

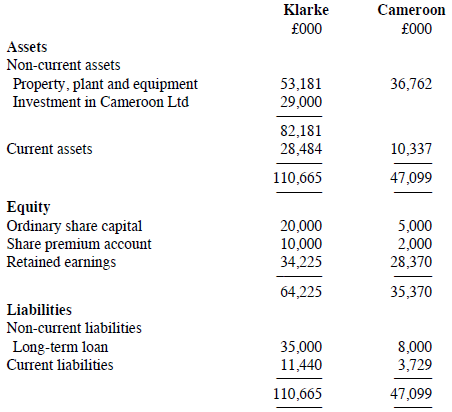

Klarke plc acquired a subsidiary, Cameroon Ltd, on 1 October 2017. The statements of financial position of Klarke plc and Cameroon Ltd as at 30 September 2018 are as follows:

Additional data:

(i) The share capital of Cameroon Ltd consists of ordinary shares of ?1 each. There have been no changes to the balances of share capital and share premium during the year. No dividends were paid or proposed by Cameroon Ltd during the year.

(ii) Klarke plc acquired 3,000,000 shares in Cameroon Ltd on 1 October 2017.

(iii) At 1 October 2017, the retained earnings of Cameroon Ltd were ?24,700,000.

(iv) The fair value of the non-current assets of Cameroon Ltd at 1 October 2017 was ?37,000,000. The book value of the non-current assets at 1 October 2017 was ?33,000,000. The revaluation has not been recorded in the books of Cameroon Ltd (ignore any effect on the depreciation for the year). There were no other differences between the book value and the fair value of the other assets and liabilities of Cameroon Ltd at the date of acquisition.

(v) The directors have concluded that goodwill on the acquisition of Cameroon Ltd has been impaired during the year. They estimate that the impairment loss amounts to 20% of the goodwill.

Required:

Calculate the following figures relating to the acquisition of Cameroon Ltd that will appear in the consolidated statement of financial position of Klarke plc at 30 September 2018:

(a) The non-controlling interest.

(b) The goodwill arising on acquisition.

(c) The consolidated retained earnings of the group.

GoodwillGoodwill is an important concept and terminology in accounting which means good reputation. The word goodwill is used at various places in accounting but it is recognized only at the time of a business combination. There are generally two types of...

Step by Step Answer:

a The noncontrolling interest 35370 5000 200...View the full answer

International Financial Reporting A Practical Guide

ISBN: 978-1292200743

6th edition

Authors: Alan Melville