Consider the (operatorname{ARDL}(p, q)) equation and the data in the file usmacro. For (p=2) and (q=1), results

Question:

Consider the \(\operatorname{ARDL}(p, q)\) equation

![]()

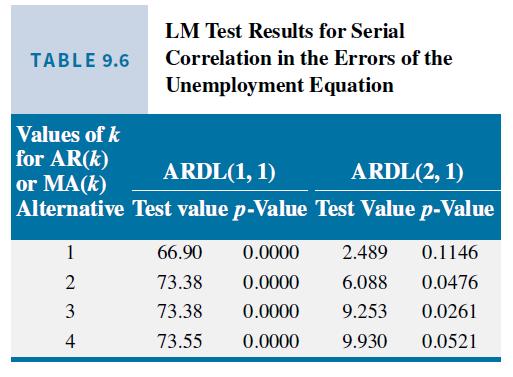

and the data in the file usmacro. For \(p=2\) and \(q=1\), results from the LM test for serially correlated errors were reported in Table 9.6 for \(\operatorname{AR}(k)\) or \(\operatorname{MA}(k)\) alternatives with \(k=1,2,3,4\). The \(\chi^{2}=T \times R^{2}\) version of the test, with missing initial values for \(\hat{e}_{t}\) set to zero, was used to obtain those results.

a. Using the same test statistic and the same AR and MA alternatives, and a \5\% significance level, test for serially correlated errors in the two models, \((p=4, q=3)\) and \((p=6, q=5)\).

b. Examine the residual correlograms from the two models in part (a). What do they suggest?

Data From Table 9.6:-

Step by Step Answer:

Principles Of Econometrics

ISBN: 9781118452271

5th Edition

Authors: R Carter Hill, William E Griffiths, Guay C Lim