Consider the regression model (y_{i}=beta_{1} x_{i 1}+beta_{2} x_{i 2}+e_{i}) with two explanatory variables, (x_{i 1}) and (x_{i

Question:

Consider the regression model \(y_{i}=\beta_{1} x_{i 1}+\beta_{2} x_{i 2}+e_{i}\) with two explanatory variables, \(x_{i 1}\) and \(x_{i 2}\), but no constant term.

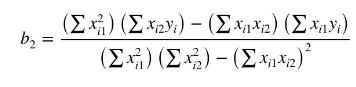

a. The sum of squares function is \(S\left(\beta_{1}, \beta_{2} \mid \mathbf{x}_{1}, \mathbf{x}_{2}\right)=\sum_{i=1}^{N}\left(y_{i}-\beta_{1} x_{i 1}-\beta_{2} x_{i 2}\right)^{2}\). Find the partial derivatives with respect to the parameters \(\beta_{1}\) and \(\beta_{2}\). Setting these derivatives to zero and solving and show that the least squares estimator of \(\beta_{2}\) is

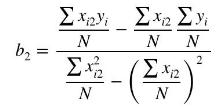

b. Let \(x_{i 1}=1\) and show that the estimator in (a) reduces to

Compare this equation to equation (2A.5) and show that they are equivalent.

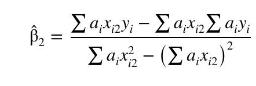

c. In the estimator in part (a), replace \(y_{i}, x_{i 1}\) and \(x_{i 2}\) by \(y_{i}^{*}=y_{i} / \sqrt{h_{i}}, x_{i 1}^{*}=x_{i 1} / \sqrt{h_{i}}\) and \(x_{i 2}^{*}=x_{i 2} / \sqrt{h_{i}}\). These are transformed variables for the heteroskedastic model \(\sigma_{i}^{2}=\sigma^{2} h\left(\mathbf{z}_{i}\right)=\sigma^{2} h_{i}\). Show that the resulting GLS estimator can be written as

where \(a_{i}=1 /\left(c h_{i}\right)\) and \(c=\sum\left(1 / h_{i}\right)\). Find \(\sum_{i=1}^{N} a_{i}\).

d. Show that under homoskedasticity \(\hat{\beta}_{2}=b_{2}\).

e. Explain how \(\hat{\beta}_{2}\) can be said to be constructed from "weighted data averages" while the usual least squares estimator \(b_{2}\) is constructed from "arithmetic data averages." Relate your discussion to the difference between WLS and ordinary least squares.

Data From Equation 2A.5:-

Step by Step Answer:

Principles Of Econometrics

ISBN: 9781118452271

5th Edition

Authors: R Carter Hill, William E Griffiths, Guay C Lim