Frits Seegers, President of Citibank California, was meeting with his management team to review the performance evaluation

Question:

Frits Seegers, President of Citibank California, was meeting with his management team to review the performance evaluation and bonus decisions for the California branch managers. James McGaran’s performance evaluation was next. Frits felt uneasy about this one. McGaran was manager of the most important branch in the Los Angeles area, and his financials were impressive. A year ago he would have received “above par” rating with full bonus. But last year, the California Division of Citibank had introduced a new performance scorecard to highlight the importance of a diverse set of measures in achieving the strategic goals of the division. Among the new measures introduced was a customer satisfaction indicator. Unfortunately, James McGaran had scored “below par” on customer satisfaction.

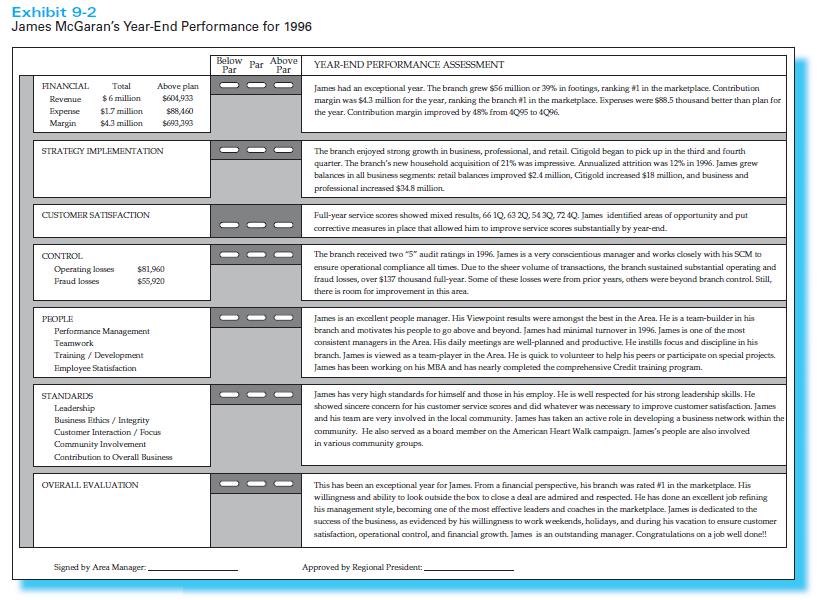

Frits looked at Lisa Johnson, the area manager supervising James McGaran. Frits had read Lisa’s comments (Exhibit 9-2). The comments were very positive, but Lisa had not wanted to give a final recommendation until she had discussed it with Frits. She knew that James’ case would be watched closely by many managers within the division.

The Financial District Branch

James McGaran was manager of the most important of the 31 branches in the Los Angeles area. Located in Los Angeles’s financial district, James’s branch had a staff of 15 people, revenues of $6 million, and $4.3 million in profit margin. The customer base was very diverse. Individual customers ranged from people who worked in the financial district with sophisticated retail banking needs to less informed individuals banking for convenience. Business customers were sophisticated buyers who demanded high service quality and knowledgeable employees who could satisfy their financial needs. “Mom and pop” businesses, the dominant segment in other regions, were also present but to a much lesser extent. Competition was intense. Two competitors—Bank of America and Wells Fargo—had offices less than a block away from James’s branch.

James joined Citibank in 1985 as assistant branch manager. He had worked in the banking industry since 1977. Within a year, in 1986, he was promoted to manager of a small branch. He progressed quickly through the ranks until 1992 when he was given the responsibility of managing the Financial District office. His performance in this office had exceeded expectations every single year. He had delivered impressive financial results for four years in a row. In 1996, when the division expanded its performance indicators to include non-financial measures, it became apparent that his branch’s customer satisfaction ratings did not follow the same pattern as its financial performance.

James reported to Lisa Johnson, Los Angeles area manager. Lisa was a long time employee of Citibank. She joined the company in 1978 in Chicago and moved to California in early 1988. Her area was the biggest in the division and included two regions that had previously been managed separately. Lisa was a hands-on manager who spent a lot of time in the branches supporting the managers and becoming familiar with the events in each branch.

New Performance Scorecard

Citibank was a niche player in the California market. It had eighty branches compared with four hundred offices of its biggest competitor. Citibank’s strategy in California was to build a profitable franchise by providing relationship banking combined with a high level of service to its customers. Service was delivered face to face (in the branch) or remotely, depending on the wishes of the customers. Customers’ service expectations rose in line with their net worth, as did their profitability for the bank. These customers demanded high levels of service with careful personal attention and a broad selection of financial products. Citibank provided a broad array of services including a dense network of ATM machines, 24 hour banking, and home banking.

Financial measures had dominated Citibank’s performance evaluation in the past. But top managers in the division felt that these measures were poor vehicles to communicate the high service strategy of the bank. Frits Seegers wanted people in the division to have a broader view of the business and focus their attention on those dimensions that were critical to the long term success of the franchise.

To reflect the importance of non-financial measures as leading indicators of strategy implementation, the California Division developed a Performance Scorecard. It complemented existing financial measures with new measures reflecting important competitive dimensions in the bank’s strategy. The initial version was pre-tested in 1995 and, starting in the first quarter of 1996, Performance Scorecard goals and performance data became a central management tool to implement strategy and evaluate performance.

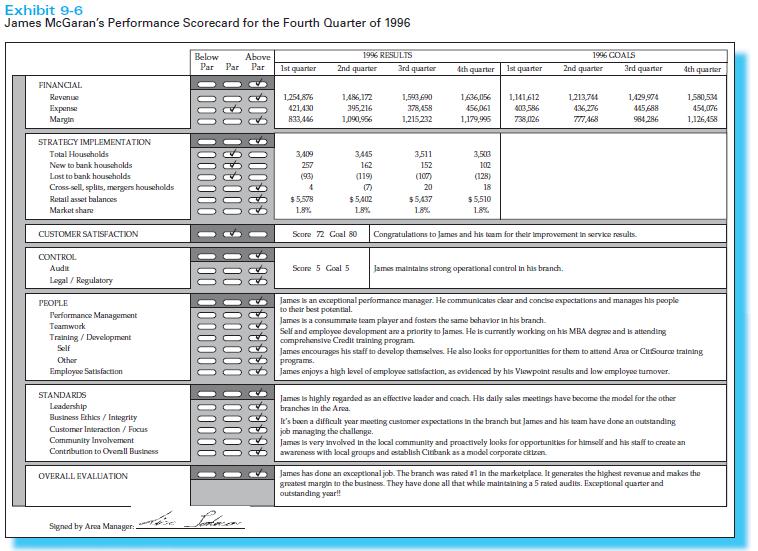

The Performance Scorecard was built around six different types of measures: financial, strategy implementation, customer satisfaction, control, people, and standards (see Exhibits 9-3 to 9-6).

Financial measures were obtained from the regular accounting system and focused primarily on total revenue and profit margin against targets.

Strategy implementation measures tracked revenue for different types of target customer segments relevant to the strategy of the branch. James’s Performance Scorecard focused primarily on revenues from retail customers—households, businesses, and professionals.

Customer satisfaction was measured through telephone interviews with approximately twenty-five branch customers who had visited the branch during the past month. Customer satisfaction scores were derived from questions that focused on branch service as well as other Citibank services like 24 hours phone banking and ATM services. An independent research firm was responsible for administering the survey under the guidance of the division’s Relationship Satisfaction department. Given the current strategy of the bank, which focused on customer service as a key differentiator, Frits Seegers considered the customer satisfaction measure as critical to the long term success of his division. He saw it as a leading indicator of future financial performance. If customer satisfaction deteriorated, it was only a matter of time before it showed in the financials.

Control measures reported the evaluation by internal auditors on the branch’s internal control processes. Branches had to score at least par (defined as 4 on a scale of 1 to 5) to be eligible for any bonus. If the rating was below 4, the branch’s business was considered at risk and did not meet the minimum requirements for effective control.

People and Standards were non-quantifiable ratings determined subjectively by the branch manager’s boss. The “people” measure focused on the proactive efforts of the manager to develop and communicate with subordinates, to encourage area training programs, and to be a role model to more junior people. Standards included an assessment of a manager’s involvement in community groups, trade associations, and business ethics.

Each component of the Scorecard was scored independently into one of three rating categories: “below par,” “par,” or “above par.” For those measures that could be measured quantitatively financial, strategy implementation, customer satisfaction, and control—pre-defined performance thresholds determined where performance fell in this three-level scale. However, ratings related to people and standards lacked an appropriate objective indicator: in these cases performance was determined subjectively by the branch manager’s superior.

In addition, the manager’s boss gave a global rating for each of the six components of the Scorecard and an overall rating for the branch manager.

Performance and Incentives

The performance planning process started in October with a negotiation process between Frits Seegers and his area managers. At the end of this initial stage, Performance Scorecard targets for the upcoming year were established for the division and for each area. These targets were cascaded down the organization. Area managers negotiated with branch managers to determine their financial targets and strategy implementation goals for the year. At the end of this process, the targets for branch managers were added up to ensure that they equaled or exceeded the area’s targets.

Customer satisfaction and control goals were common to all branches in the division. For customer satisfaction, the 1996 goal was to achieve a rating of at least 80.

Financial, strategy implementation, customer satisfaction, and control targets formed the quantitative basis for ex post performance evaluation. Each quarter, area managers received branch information with the actual numbers for each of these measures and a comparison with the quarterly objectives. This information, together with the subjective scores that the area manager gave for the People and Standards ratings, formed the basis for the quarterly and yearly evaluation of branch managers.

Year-end performance evaluation was determined jointly by a team led by Frits Seegers. The team comprised the area managers, including Lisa Johnson, and managers from human resources, quality, and finance. Frits believed that having a team jointly evaluate performance of every branch manager gave consistency to the process throughout the division. It was this team that was now meeting to decide James’s performance evaluation for the year.

In addition to other motivational elements associated with the yearly evaluation, a branch manager’s bonus was linked to his or her final Performance Scorecard rating. A“below par” rating did not carry any bonus. A “par” rating generated a bonus of up to 15% of the basic salary (for branch managers with a salary in the lower part of the salary bracket, the bonus could reach 20%). An “above par” rating could mean as much as 30% bonus.

Without “par” ratings in all the components of the Scorecard, a manager could not get an “above par” rating.

Performance of the Financial District Branch

Frits reviewed the 1996 performance evaluation forms for James McGaran. His financials were outstanding—20% above target. According to Lisa Johnson, James’s branch “had generated the highest revenue and made the greatest margin contribution to the business of any branch in the system.” His strategy implementation scores were in the “par” to “above par” range, although Lisa Johnson had given him an “above par” rating in three quarters. James had maintained an “above par” rating in the control scorecard and Lisa Johnson had rated him exceptionally where she had the discretion to do so.

However, customer satisfaction was “below par”. A branch obtained a “par” rating if it scored 74 to 79. If customer satisfaction was above 80 or it had improved 6 points with no regression during 2 quarters and it was above the market average (77), then the branch got an “above par” rating.

Lisa and Frits were aware that a strict application of the new policies for performance evaluation meant that James could get at most a “par” evaluation for the year. But James’s branch was the largest and toughest branch in the division. He had a demanding clientele and challenging competition. It was difficult to manage such a diverse set of indicators, and the customer satisfaction measure was sometimes hard to reconcile with demonstrated financial performance. James had discussed with Lisa his concerns regarding the adequacy of the survey. Customers rated not only their branch, but also other Citibank services such as ATM’s that were out of the control of branch managers. Thus, it was possible that these centralized services were not providing adequate support to the sophisticated customers of James’s branch.

Notwithstanding these concerns, James had worked hard to improve the customer satisfaction rating during the last quarter. He had made some changes in his staff to improve the score. One person in the branch was now dedicated to greeting the customer when arriving at the office and helping with any problems that may arise. He also held branch meetings and coached branch employees to focus their attention on improving customer satisfaction.

James gave a lot of importance to his ratings. It was a matter of pride to be “above par” and show that he was able to successfully run the hardest branch in the division. He had felt very disappointed when, in two quarters of the year, his rating had been only par. His branch was difficult and he was delivering the best financial performance in the division. He thought that his efforts deserved an above par rating, even if customer satisfaction was somewhat lagging.

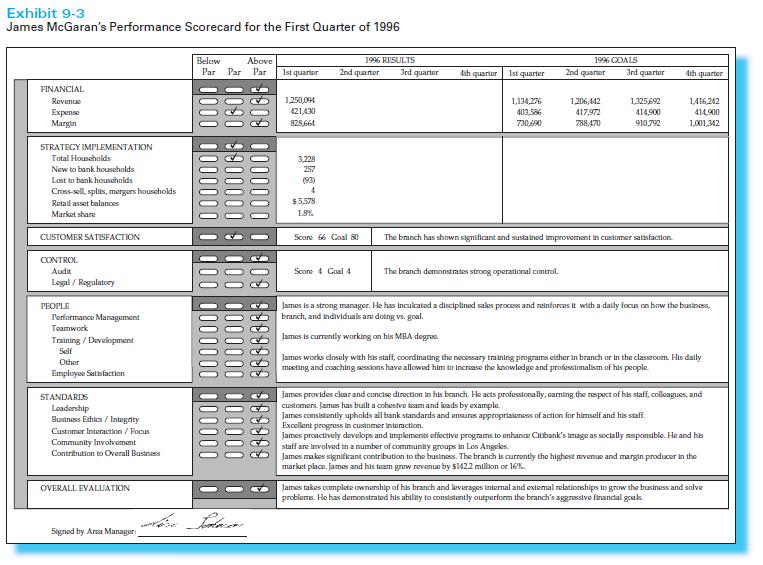

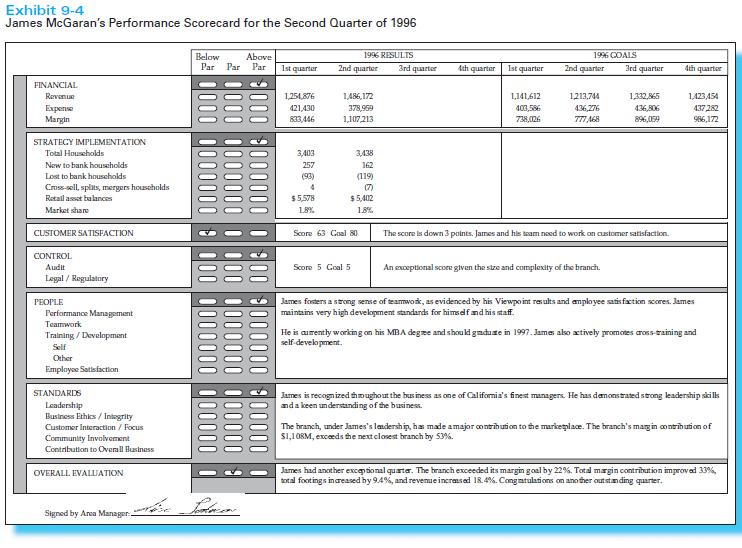

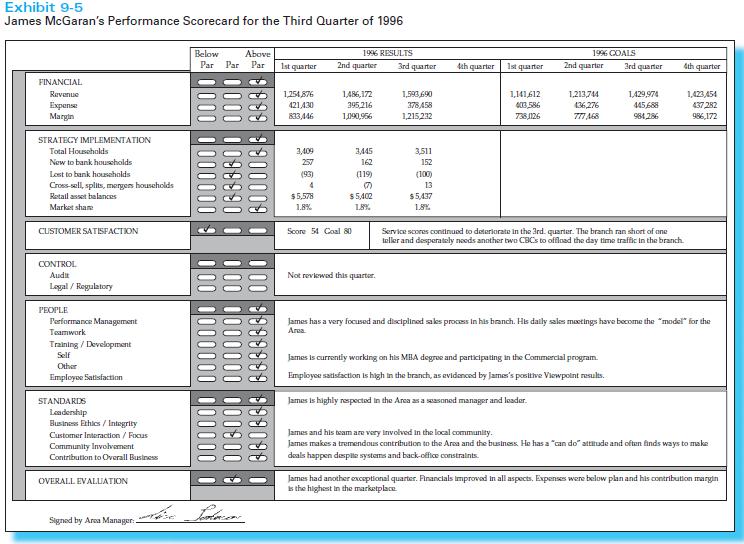

Frits reviewed James’s scorecards for each quarter of 1996 (Exhibits 9-3 to 9-6). His financials were exceptional, but only in the last quarter was he able to pull customer satisfaction to an acceptable level. If the performance evaluation team gave James an “above par” people could think that the division was not serious about its non-financial measures. James had been “below par” in customer satisfaction for all quarters of 1996 and, if this measure was truly important, he should not get an “above par” rating. On the other hand, he deserved the above par given his excellent performance in other dimensions. James was a reference point for a lot of other branch managers.

Frits held the summary scorecard in his hand (Exhibit 9-2) and turned to Lisa Johnson:

“Lisa, I’ve read over your comments and reviewed James’s quarterly scorecards. All that now remains is ticking off the six boxes on this summary form and deciding on an overall performance rating for James . . . What do you recommend?”

Required

(a) Why has Citibank introduced its Performance Scorecard? What benefits does Citibank expect the Performance Scorecard to provide?

(b) What cause-and-effect linkages are implied in the Performance Scorecard?

(c) What characteristics are desirable for measures used to evaluate and reward performance Discuss the Performance Scorecard’s measures in relation to the characteristics you identified.

(d) Assume that you are Lisa Johnson. Complete Exhibit 1 to evaluate James’s performance and explain your rationale for your rating on each of the six dimensions and the overall evaluation.

Step by Step Answer:

Part a Why has Citibank introduced its Performance Scorecard Citibank introduced its Performance Scorecard to emphasize a diverse set of measures for evaluating performance that cohere with the banks ...View the full answer

Management Accounting Information for Decision-Making and Strategy Execution

ISBN: 978-0137024971

6th Edition

Authors: Anthony A. Atkinson, Robert S. Kaplan, Ella Mae Matsumura, S. Mark Young