Question: Orth and Associates is a small firm that provides structural engineering services for its clients. The company performs structural engineering services for both residential and

Required:

a. 1. Using the plantwide allocation method, calculate the total cost for each product.

2. Using the plantwide approach, calculate the profit for each product. Also calculate profit as a percent of sales revenue for each product (round to the nearest tenth of a percent).

b. 1. Using activity-based costing, calculate the predetermined overhead rate for each activity.

2. Using activity-based costing, calculate the amount of overhead assigned to each product.

3. Using activity-based costing, calculate the profit for each product. Also calculate profit as a percent of sales revenue for each product (round to the nearest tenth of a percent).

c. What caused the shift of overhead costs to the residential product using activity-based costing? How might management use this information to make improvements within the company?

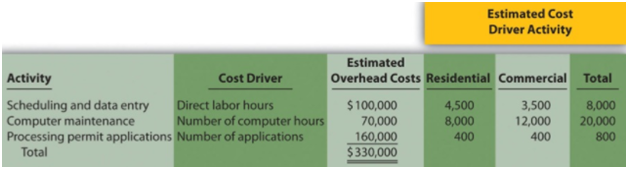

Estimated Cost Driver Activity Estimated Overhead Costs Residential Commercial Total 4,500 8,000 400 Cost Driver Direct labor hours Number of computer hours Activity Scheduling and data entry Computer maintenance Processing permit applications Number of applications Total 8,000 20,000 800 3,500 12,000 400 $ 100,000 160,000 $330,000

Step by Step Solution

3.54 Rating (164 Votes )

There are 3 Steps involved in it

a 1 The plantwide allocation used by Orth and Associates is based on direct labor costs The rate is calculated as Estimated overhead cost 330000 Estimated activity in allocation base 300000 direct lab... View full answer

Get step-by-step solutions from verified subject matter experts