Take the actual SABR formula per Section 6.2.1 with 0 = 0.5%, = 0,

Question:

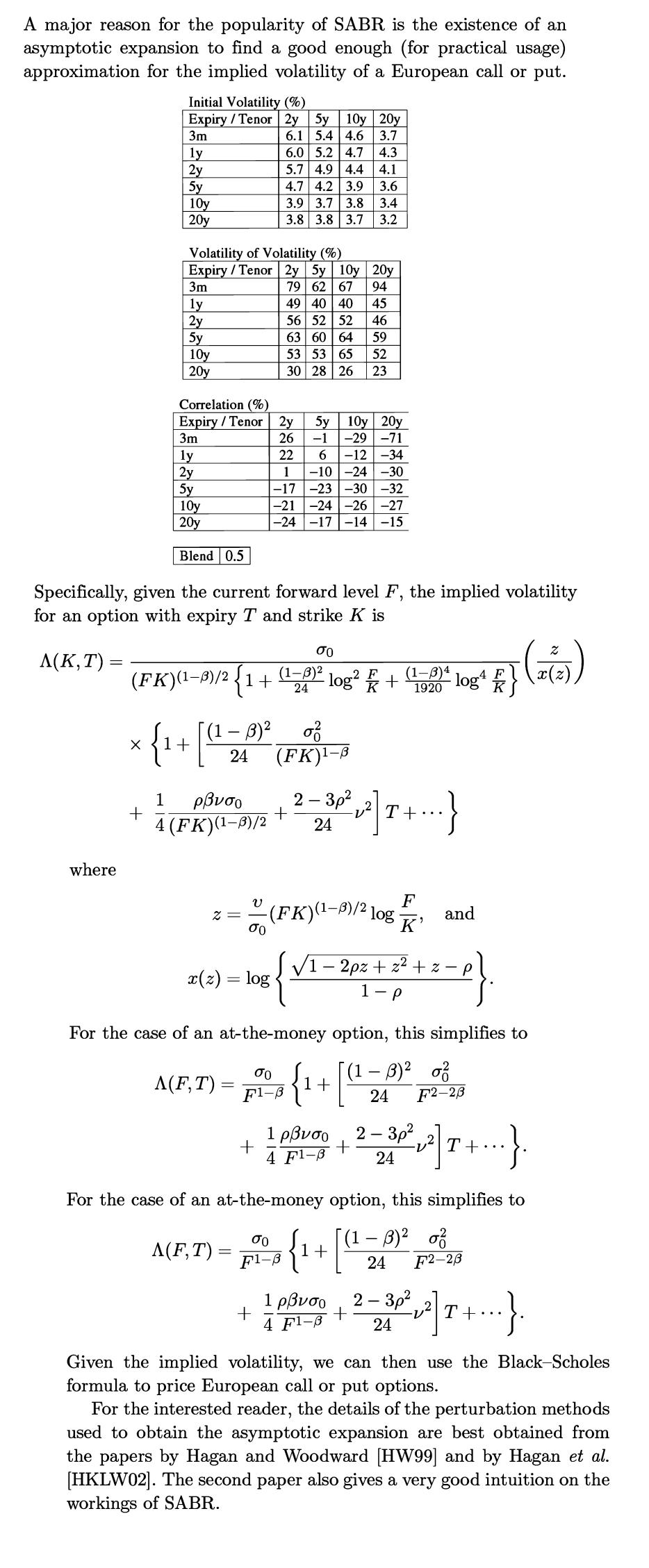

Take the actual SABR formula per Section 6.2.1 with σ0 = 0.5%, β = 0, ρ = −25%, ν = 30%, and F = 4%. By considering an expiry of 20 years and strikes at 10 basis points increments from 1 % to 2 % inclusive, try and construct an arbitrage involving butterflies (i.e. long a call at strike K − δ short two calls at strike K and long a call at strike K + δ where δ > 0). This is an illustration of the problem of negative densities under the SABR model for very low strikes and long enough expiry.

Section 6.2.1

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Mamba Dedan

I am a computer scientist specializing in database management, OS, networking, and software development. I have a knack for database work, Operating systems, networking, and programming, I can give you the best solution on this without any hesitation. I have a knack in software development with key skills in UML diagrams, storyboarding, code development, software testing and implementation on several platforms.

56+ Reviews

137+ Question Solved

Related Book For

Question Posted: