Consider the one-dividend American put option model where the discrete dividend at time t d is paid

Question:

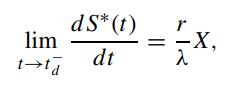

Consider the one-dividend American put option model where the discrete dividend at time td is paid at the known rate λ, that is, the dividend payment is λStd . Show that the slope of the optimal exercise boundary of the American put at time right before td is given by (Meyer, 2001)

where r is the riskless interest rate.

Consider the balance of the gain in interest income from the strike price and the loss in dividend over the differential time interval δt right before td.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

To derive the expression for the slope of the optimal exercise boundary of the American put option w...View the full answer

Answered By

Fahmin Arakkal

Tutoring and Contributing expert question and answers to teachers and students.

Primarily oversees the Heat and Mass Transfer contents presented on websites and blogs.

Responsible for Creating, Editing, Updating all contents related Chemical Engineering in

latex language

8+ Reviews

22+ Question Solved

Related Book For

Question Posted: