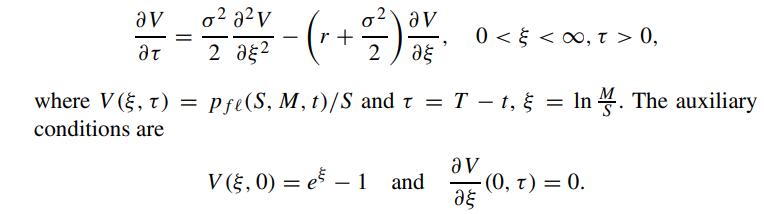

Use (4.2.21) to derive the following partial differential equation for the floating strike lookback put option Solve

Question:

Use (4.2.21) to derive the following partial differential equation for the floating strike lookback put option

Solve the above Neumann boundary value problem and check the result with the put price formula given in (4.2.10).

Define W = ∂V/∂ξ so that W satisfies the same governing differential equation but the boundary condition becomes W(0,τ) = 0. Solve for W(ξ,τ), then integrate W with respect to ξ to obtain V . Be aware that an arbitrary function ∅(t) is generated upon integration with respect to ξ . Obtain an ordinary differential equation for ∅(t) by substituting the solution for V into the original differential equation.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

To derive the partial differential equation PDE and solve the Neumann boundary value problem for the ...View the full answer

Answered By

Sheikh Muhammad Ibrahim

During the course of my study, I have worked as a private tutor. I have taught Maths and Physics to O'Level and A'Level students, as well as I have also taught basic engineering courses to my juniors in the university. Engineering intrigues me alot because it a world full of ideas. I have passionately taught students and this made me learn alot. Teaching algebra and basic calculus, from the very basics of it made me very patient. Therefore, I know many tricks to make your work easier for you. I believe that every student has a potential to work himself. I am just here to polish your skills. I am a bright student in my university. My juniors are always happy from me because I help in their assignments and they are never late.

14+ Reviews

24+ Question Solved

Related Book For

Question Posted: