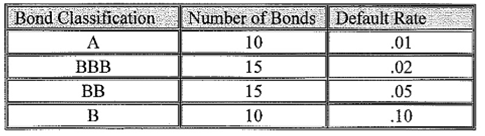

A firm has a portfolio of the following 50 bonds with the corresponding annual default rates. The

Question:

A firm has a portfolio of the following 50 bonds with the corresponding annual default rates. The default rates apply to the population of all bonds.

Assume that the bonds in the portfolio represent a random sample of all bonds in the population.

a. What is the probability that at least 2 B bonds default?

b. What is the probability that no more than 1 BB bond defaults?

c. What is the expected number of BBB defaults in the portfolio? d. What is the expected number of total defaults in the portfolio? e. An insurance company will insure against the risk of default. Assume that the loss due to default is $100,000 for each bond, and the insurance company has a margin of 50% for expenses and profit. What premium will the insurance company charge?

Expert Answer:

a Let X be the number of bonds default Using Binomial probability Probabilit... View the full answer