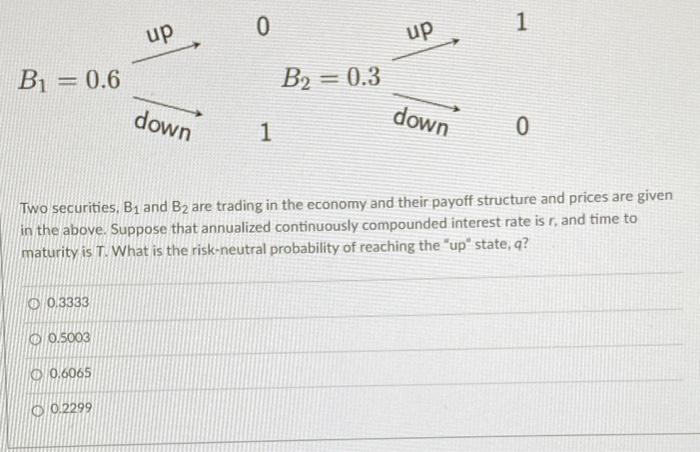

Question: 0 1 up up B1 = 0.6 -- B2 = 0.3 down down 1 0 Two securities. B and B2 are trading in the economy

0 1 up up B1 = 0.6 -- B2 = 0.3 down down 1 0 Two securities. B and B2 are trading in the economy and their payoff structure and prices are given in the above. Suppose that annualized continuously compounded interest rate is r, and time to maturity is T. What is the risk-neutral probability of reaching the "up state, q? O 0.3333 O.S003 0 0.6065 0.2299

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock