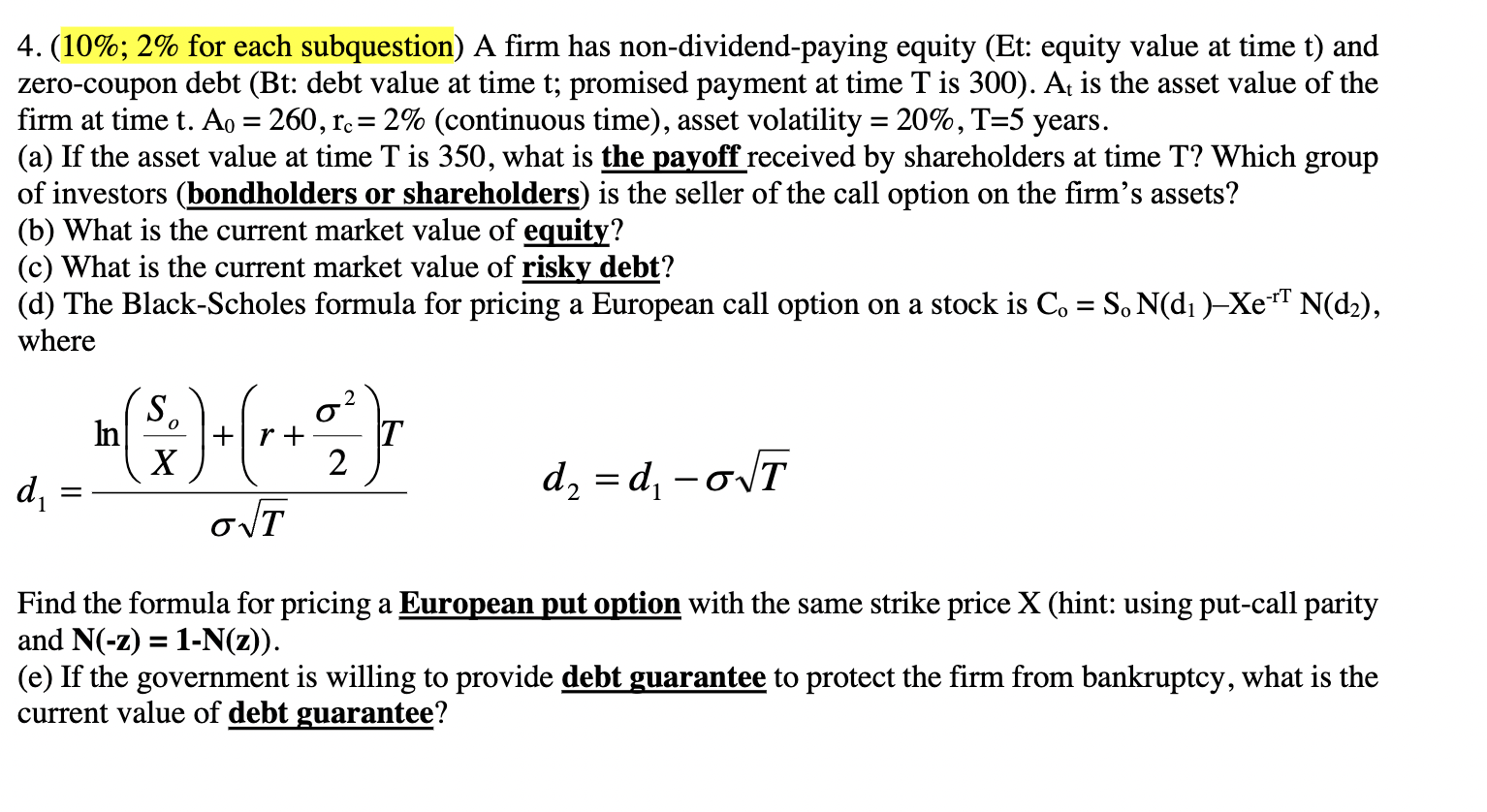

Question: ( 1 0 % ; 2 % for each subquestion ) A firm has non - dividend - paying equity ( Et: equity value at

; for each subquestion A firm has nondividendpaying equity Et: equity value at time and

zerocoupon debt Bt: debt value at time ; promised payment at time is is the asset value of the

firm at time tcontinuous time asset volatility years.

a If the asset value at time is what is the payoff received by shareholders at time Which group

of investors bondholders or shareholders is the seller of the call option on the firm's assets?

b What is the current market value of equity?

c What is the current market value of risky debt?

d The BlackScholes formula for pricing a European call option on a stock is

where

Find the formula for pricing a European put option with the same strike price hint: using putcall parity

and

e If the government is willing to provide debt guarantee to protect the firm from bankruptcy, what is the

current value of debt guarantee?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock