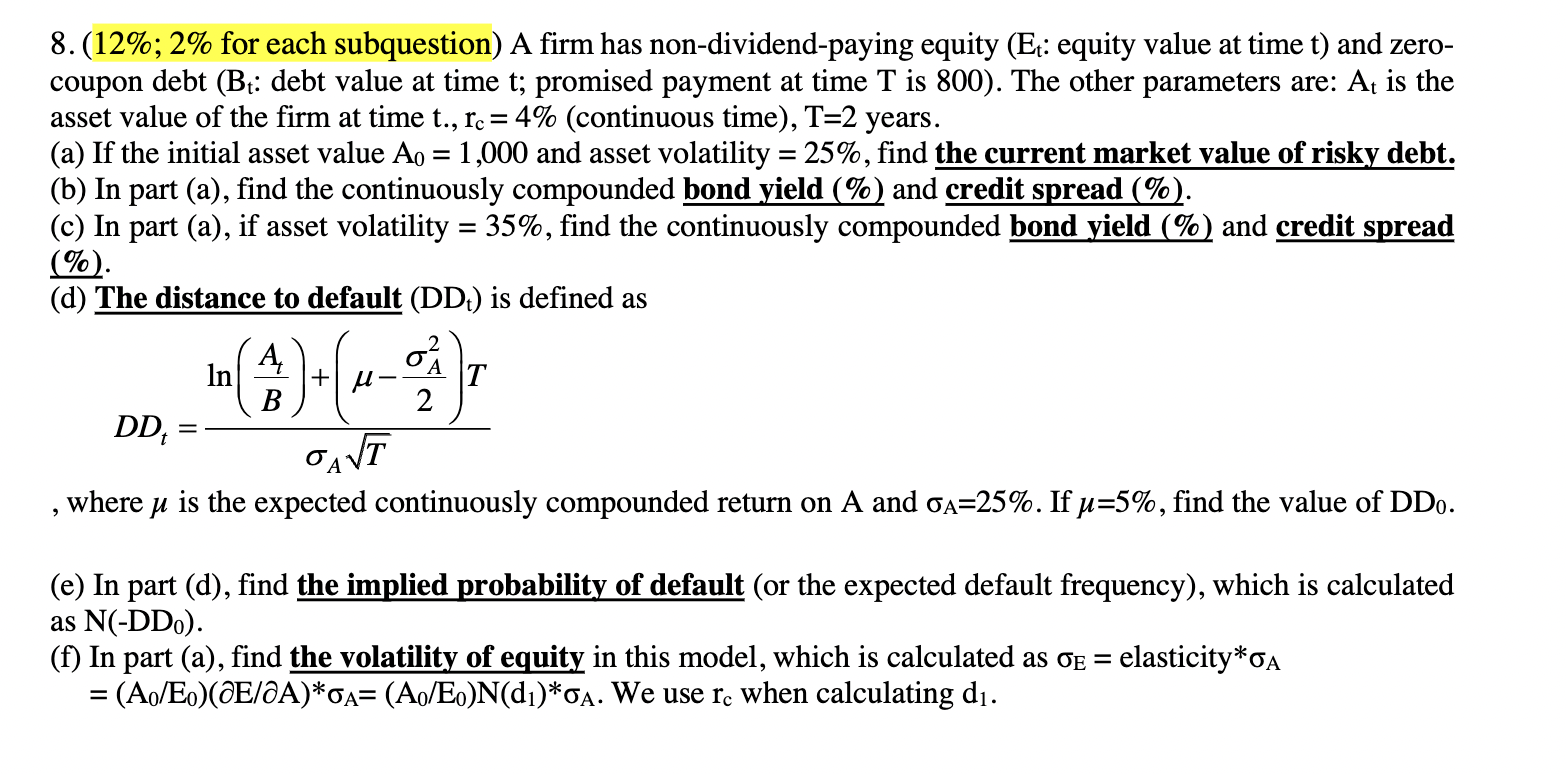

Question: ( 1 2 % ; 2 % for each subquestion ) A firm has non - dividend - paying equity ( E t : equity

; for each subquestion A firm has nondividendpaying equity : equity value at time and zero

coupon debt : debt value at time ; promised payment at time is The other parameters are: is the

asset value of the firm at time continuous time years.

a If the initial asset value and asset volatility find the current market value of risky debt.

b In part a find the continuously compounded bond yield and credit spread

c In part a if asset volatility find the continuously compounded bond yield and credit spread

d The distance to default is defined as

where is the expected continuously compounded return on A and If find the value of

e In part d find the implied probability of default or the expected default frequency which is calculated

as

f In part a find the volatility of equity in this model, which is calculated as elasticity

elA We use when calculating

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock