Question: 1) 2) Consider two risky securities A and B with a correlation coefficient = 1. A has an expected rate of return of 10% and

1)

2) Consider two risky securities A and B with a correlation coefficient = 1. A has an expected rate of return of 10% and a standard deviation of 15%. B has an expected rate of return of 8% and a standard deviation of 10%. What is the rate of return for the risk-free portfolio that is formed with these two securities?

9.4%

8.8%

8.6%

9.2%

3)

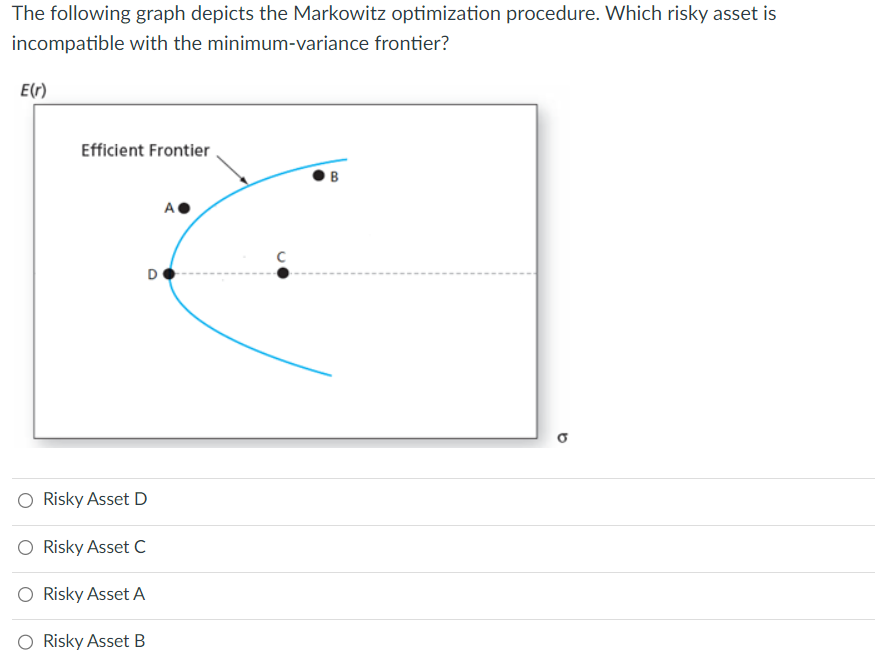

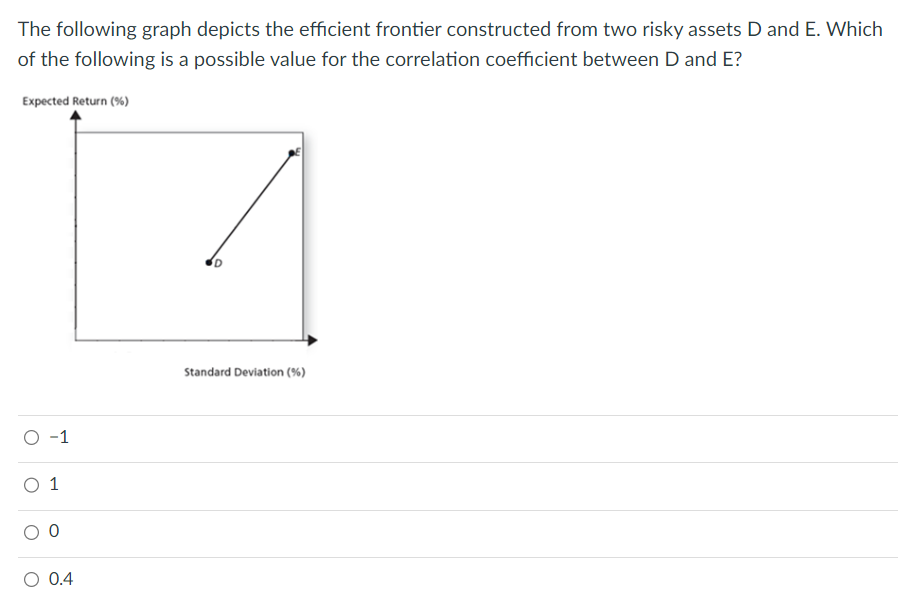

The following graph depicts the Markowitz optimization procedure. Which risky asset is incompatible with the minimum-variance frontier? Risky Asset D Risky Asset C Risky Asset A Risky Asset B The following graph depicts the efficient frontier constructed from two risky assets D and E. Which of the following is a possible value for the correlation coefficient between D and E ? Expoetad Dasuan raes 1 1 0 0.4

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts