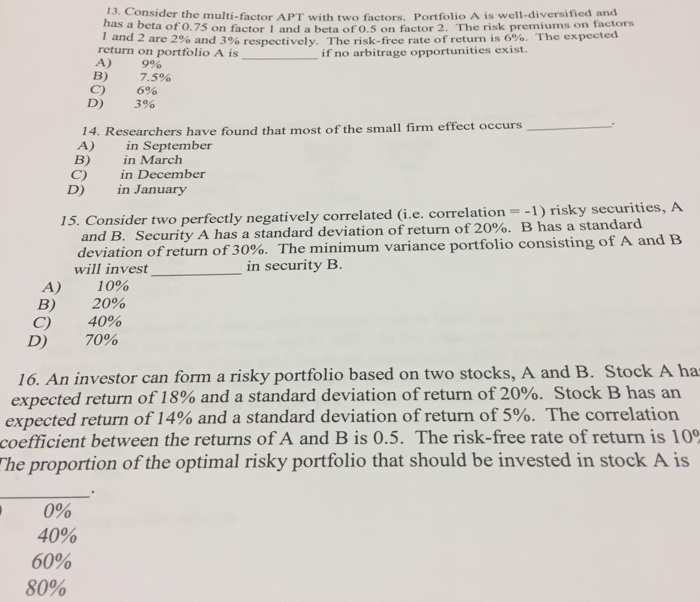

Question: Please answer all four if you can, thank you 13. Consider the multi-factor APT with two factors. Portfolio A is well-diversified and has a beta

Please answer all four if you can, thank you

Please answer all four if you can, thank you 13. Consider the multi-factor APT with two factors. Portfolio A is well-diversified and has a beta of 0.75 on factor 1 and a beta of 0.5 on factor 2. The risk premiums on Tactors 1 and 2 are 2% and 3% respectively. The risk-free rate of return is 6%. The ex return on portfolio A is if no arbitrage opportunities exist 9% 7.5% C) D) 6% 3% 14. Researchers have found that most of the small firm effect occurs A) in September B) in March in December C) D) in January Consider two perfectly negatively correlated and B. i.e. correlation1) risky securities, A Security A has a standard deviation of return of 20%, B has a standard deviation ofreturn of 30%. T he minimum variance portfolio consisting of A and B will invest in security B A) B) C) 10% 20% 40% D) 70% 16. An investor can form a risky portfolio based on two stocks, A and B. Stock A ha expected return of 18% and a standard deviation of return of 20%. Stock B has an expected return of 14% and a standard deviation of return of 5%. The correlation coefficient between the returns of A and B is 0.5. The risk-free rate of return is 10 he proportion of the optimal risky portfolio that should be invested in stock A is 1S 40% 60% 80%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts