Question: 1 Consider again the same situation with 4 assets and the following expected rates of return and variance - covariance matrix: table [ [

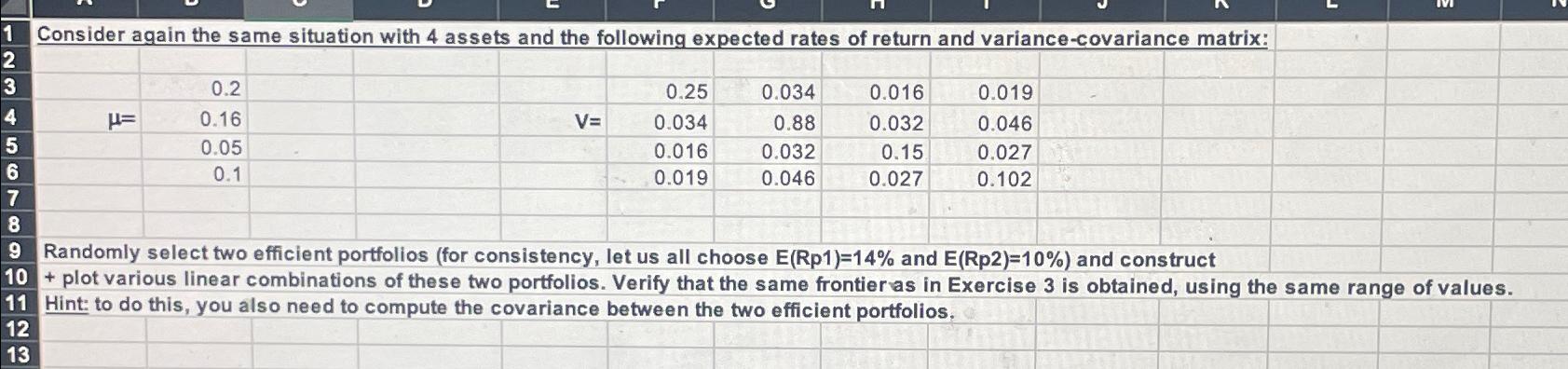

Consider again the same situation with assets and the following expected rates of return and variancecovariance matrix:

table

Randomly select two efficient portfolios for consistency, let us all choose and and construct

plot various linear combinations of these two portfolios. Verify that the same frontieras in Exercise is obtained, using the same range of values.

Hint: to do this, you also need to compute the covariance between the two efficient portfolios.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock