Question: Please solve. Use excel and show step by step and show formulas. Consider the same situation with 4 assets and the following expected rates of

Please solve. Use excel and show step by step and show formulas.

Please solve. Use excel and show step by step and show formulas.

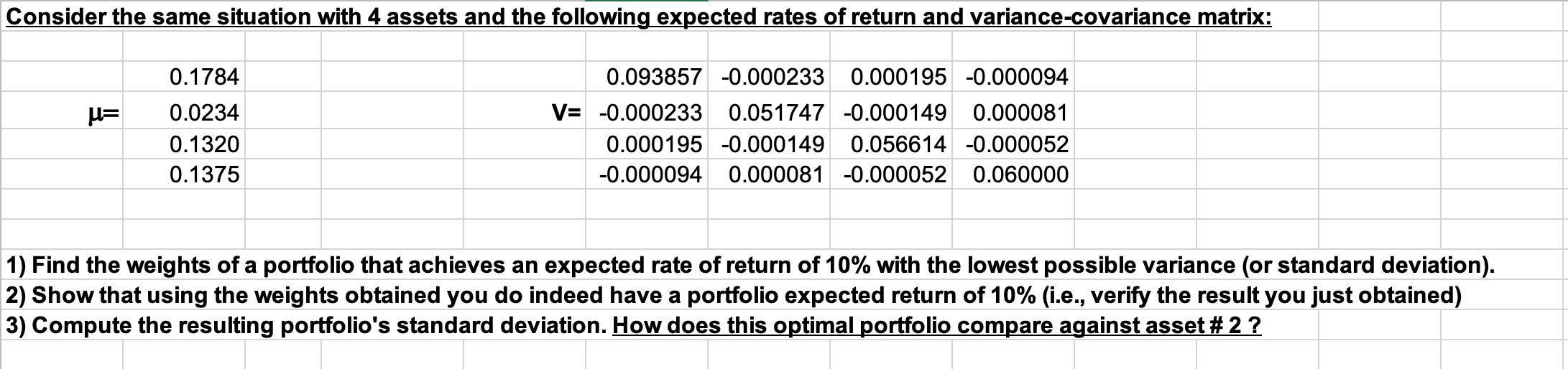

Consider the same situation with 4 assets and the following expected rates of return and variance-covariance matrix: u= 0.1784 0.0234 0.1320 0.1375 0.093857 -0.000233 0.000195 -0.000094 V= -0.000233 0.051747 -0.000149 0.000081 0.000195 -0.000149 0.056614 -0.000052 -0.000094 0.000081 -0.000052 0.060000 1) Find the weights of a portfolio that achieves an expected rate of return of 10% with the lowest possible variance (or standard deviation). 2) Show that using the weights obtained you do indeed have a portfolio expected return of 10% (i.e., verify the result you just obtained) 3) Compute the resulting portfolio's standard deviation. How does this optimal portfolio compare against asset # 2

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts