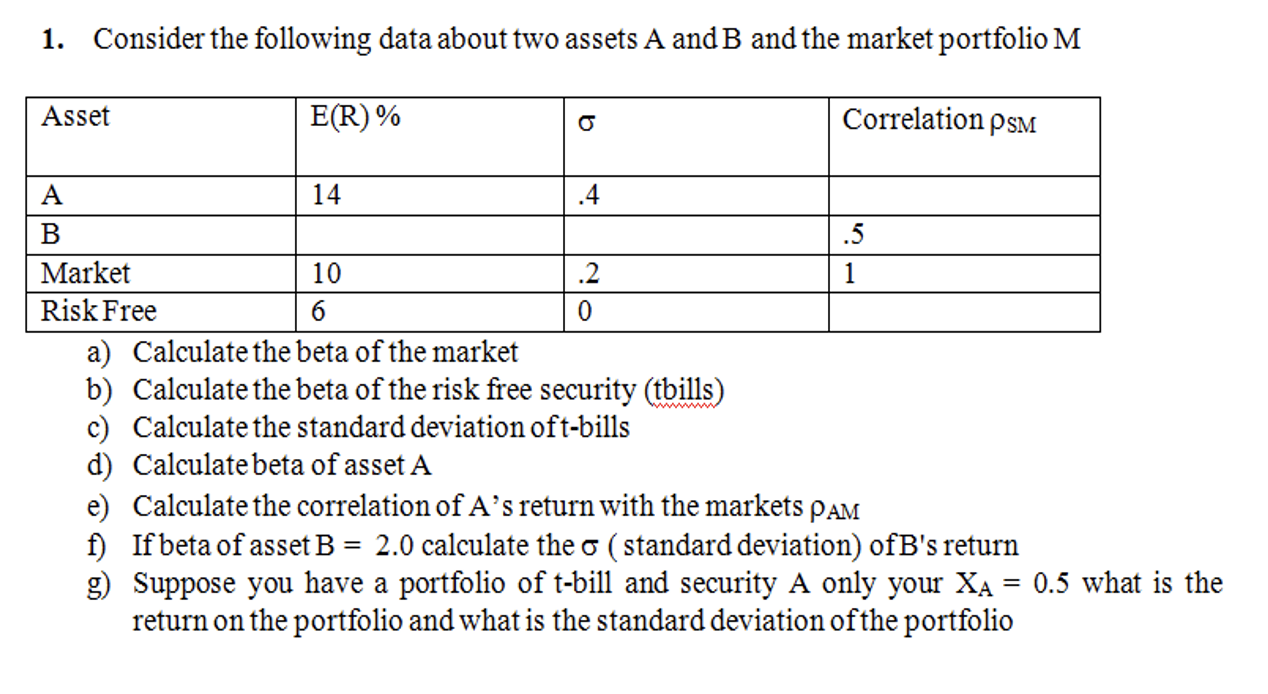

Question: 1. Consider the following data about two assets A and B and the market portfolio M a) Calculate the beta of the market b) Calculate

1. Consider the following data about two assets A and B and the market portfolio M a) Calculate the beta of the market b) Calculate the beta of the risk free security (tbills) c) Calculate the standard deviation of t-bills d) Calculate beta of asset A e) Calculate the correlation of A's return with the markets AM f) If beta of asset B=2.0 calculate the ( standard deviation) of B 's return g) Suppose you have a portfolio of t-bill and security A only your XA=0.5 what is the return on the portfolio and what is the standard deviation of the portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock