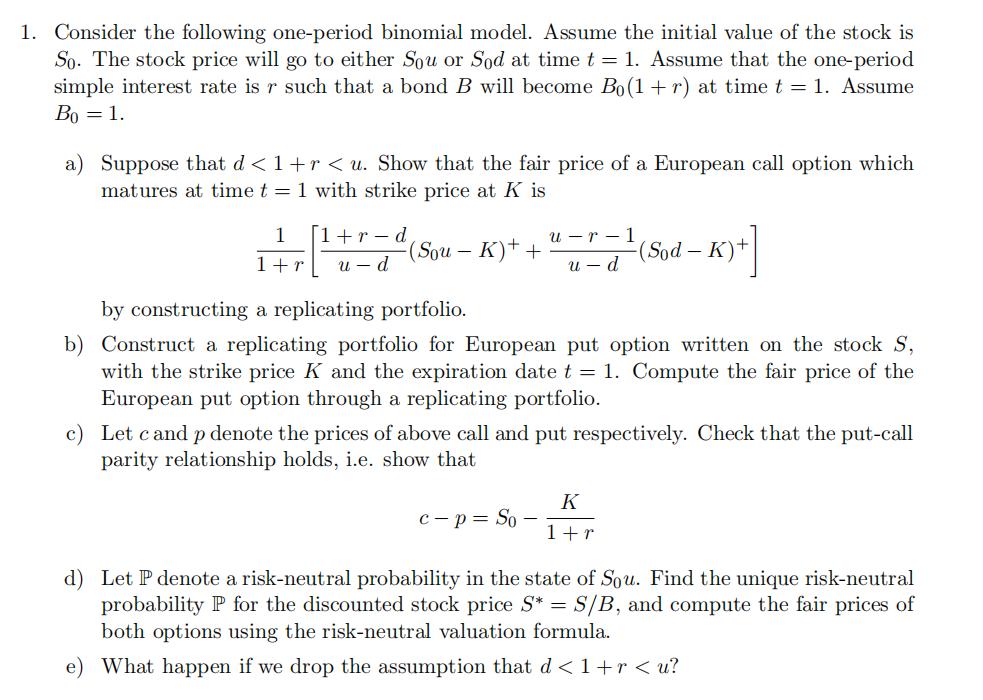

Question: 1. Consider the following one-period binomial model. Assume the initial value of the stock is So. The stock price will go to either Sou

1. Consider the following one-period binomial model. Assume the initial value of the stock is So. The stock price will go to either Sou or Sod at time t = 1. Assume that the one-period simple interest rate is r such that a bond B will become Bo(1+r) at time t = 1. Assume Bo = 1. a) Suppose that d

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock