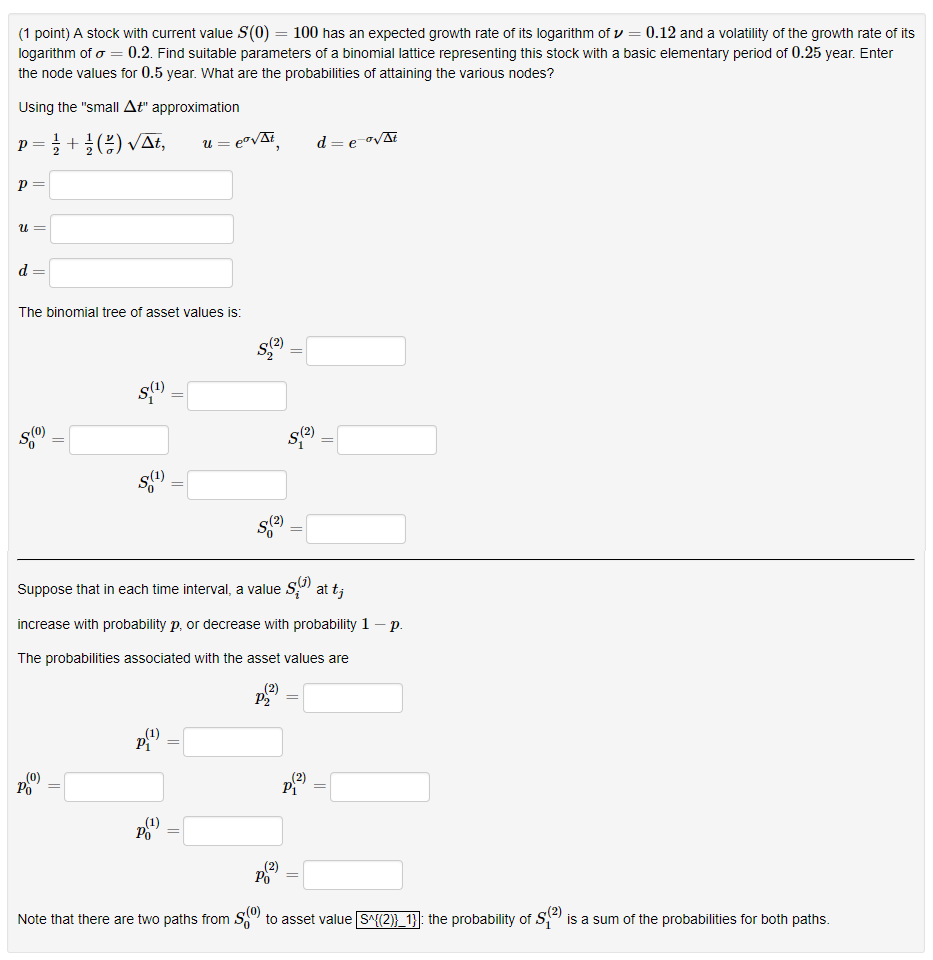

Question: (1 point) A stock with current value S(0) 100 has an expected growth rate of its logarithm of v 0.12 and a volatility of the

(1 point) A stock with current value S(0) 100 has an expected growth rate of its logarithm of v 0.12 and a volatility of the growth rate of its logarithm of 0.2. Find suitable parameters of a binomial lattice representing this stock with a basic elementary period of 0.25 year. Enter the node values for 0.5 year. What are the probabilities of attaining the various nodes? Using the "small At" approximation The binomial tree of asset values is 0 0 0 Suppose that in each time interval, a value S at t increase with probability p, or decrease with probability 1-p The probabilities associated with the asset values are Note that there are two paths from S to asset value2) the probability of s(2 is a sum of the probabilities for both paths

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts