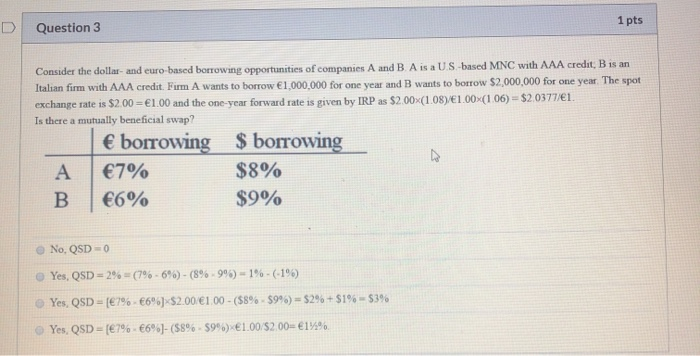

Question: 1 pts D Question 3 Consider the dollar- and euro-based borrowing opportunities of companies A and B. A is a US-based MNC with AAA credit,

1 pts D Question 3 Consider the dollar- and euro-based borrowing opportunities of companies A and B. A is a US-based MNC with AAA credit, B is an Italian firm with AAA credit. Firm A wants to borrow 1,000,000 for one year and B wants to borrow $2,000,000 for one year. The spot exchange rate is $2.00 1.00 and the one-year forward rate is given by IRP as $2.00x(1.08)/E1.00x(106) $2.0377/1 Is there a mutually beneficial swap? borrowing $ borrowing $8% 7% A $9% 6% No, QSD 0 e Yes, QSD 2% - (79 %-6 % ) - (8%-99 % ) - 1 %-(-19%) 1.00-($8% - $9%)= $2% + $19%- $3 % Yes, QSD (E7%- 6 % ) - $2.00 Yes, QSD (79%-6 % ) - ( S8 % - $9% )-1.00 S200- 1% %

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts