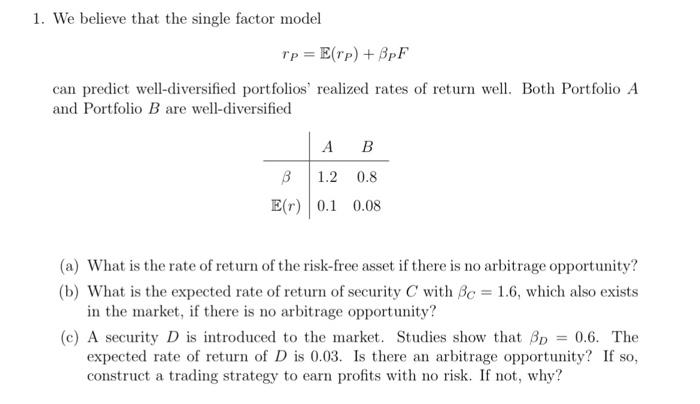

Question: 1. We believe that the single factor model rP=E(rP)+PF can predict well-diversified portfolios' realized rates of return well. Both Portfolio A and Portfolio B are

1. We believe that the single factor model rP=E(rP)+PF can predict well-diversified portfolios' realized rates of return well. Both Portfolio A and Portfolio B are well-diversified (a) What is the rate of return of the risk-free asset if there is no arbitrage opportunity? (b) What is the expected rate of return of security C with C=1.6, which also exists in the market, if there is no arbitrage opportunity? (c) A security D is introduced to the market. Studies show that D=0.6. The expected rate of return of D is 0.03 . Is there an arbitrage opportunity? If so, construct a trading strategy to earn profits with no risk. If not, why

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts