Question: 17.5 Pulij' Example: Do We Need to Regulate Banks to Save Them From Themselves? learning lObjective 1152 Explain how game theory.r can be used to

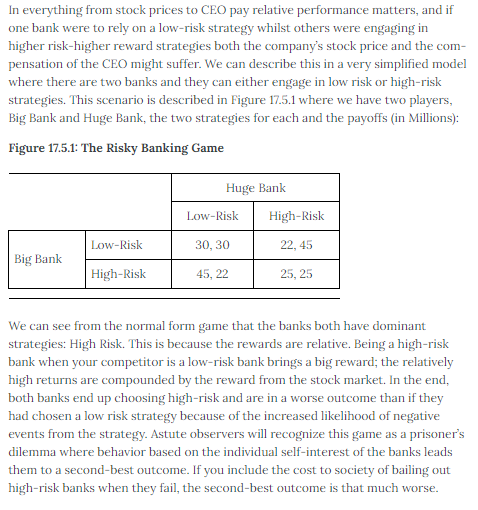

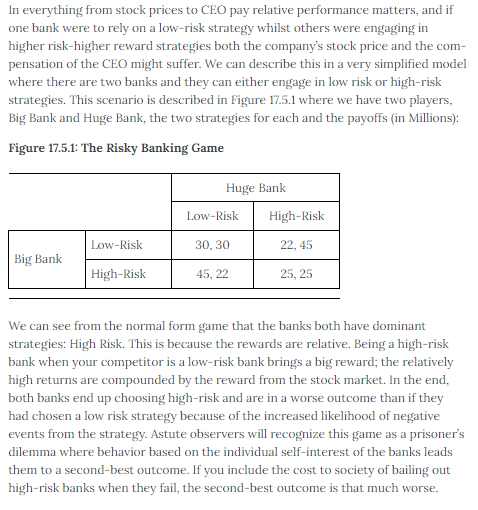

17.5 Pulij' Example: Do We Need to Regulate Banks to Save Them From Themselves? learning lObjective 1152 Explain how game theory.r can be used to understand the banking ctlapse of 2993. In the mid two thousands banks in the United States found themselves struggling to satisfy.r a tremendous demand for mortgages from the market for mortgage back securities: securities that were created from bundles of residential or com mercial mortgages. This, along with the lowinterest rate policy of the Federal Reserve, led to a tremendous housing boom in the United States that evolved into a spetulative investment bubble. The burstng of this bubble led to the housing market crash and, in 2993. to a banking crisis: the failure of major banking institu tions and the unprecedented government bailout of banks. These twin crises led to the worst recession since the great depression. Interestingly, this banking crisis came relatively.r soon after a series of reforms of banking regulations in the United States that gave banks much more freedom in their operations. Most notably was the 1999 repeal of provisions of the Glass Steagall Act. enacted after the beginning of the great depression in 1933, that pro hibited commercial banks from engaging in investment activities. Part of the argument of the time ofthe repeal was that banks should be allowed to innovate and be more exible which would benet consumers. The rationale was increased competition and the discipline of the market would inhibit excessive risktaking and so stringent government regulation was no longer necessary. But the discipline of the market assumes that rewards are absolute that returns are not based on relative perfonnance that the environment is not strategic. Is this an accurate description of modern banking? Probably.r not. In everything from stock prices to CEO pay relative performance matters, and if one bank were to rely on a low-risk strategy whilst others were engaging in higher risk-higher reward strategies both the company's stock price and the com- pensation of the CEO might suffer. We can describe this in a very simplified model where there are two banks and they can either engage in low risk or high-risk strategies. This scenario is described in Figure 17.5.1 where we have two players, Big Bank and Huge Bank, the two strategies for each and the payoffs (in Millions): Figure 17.5.1: The Risky Banking Game Huge Bank Low-Risk High-Risk Low-Risk 30, 30 22, 45 Big Bank High-Risk 45, 22 25, 25 We can see from the normal form game that the banks both have dominant strategies: High Risk. This is because the rewards are relative. Being a high-risk bank when your competitor is a low-risk bank brings a big reward; the relatively high returns are compounded by the reward from the stock market. In the end, both banks end up choosing high-risk and are in a worse outcome than if they had chosen a low risk strategy because of the increased likelihood of negative events from the strategy. Astute observers will recognize this game as a prisoner's dilemma where behavior based on the individual self-interest of the banks leads them to a second-best outcome. If you include the cost to society of bailing out high-risk banks when they fail, the second-best outcome is that much worse.Can policy correct the situation and lead to a mutually benecial outcome? The answer in this case is a resounding 'yes.' If p-::-licy makers take away the ability of the banks to engage in highrisk strategies, the bad equilibrium will disappear and only.r the low-risk, lowrisk outcome will remain. The banks are better off and be- cause the adverse effects of highrisk strategies going bad are taken away, society benets as well. Exploring tbe Policy Question 1. I||."|.fl'|y do you think That banks were so 1willing to engage in risky bets in the early Ends? 2. Do you think That government regulation restricting their strategy choices is appropriate in cases Twhere society has to pay for risky bets gone bad

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts