Question: 19 Using the information in the table below, derive your best estimate of the price of the call option if the underlying share price decreases

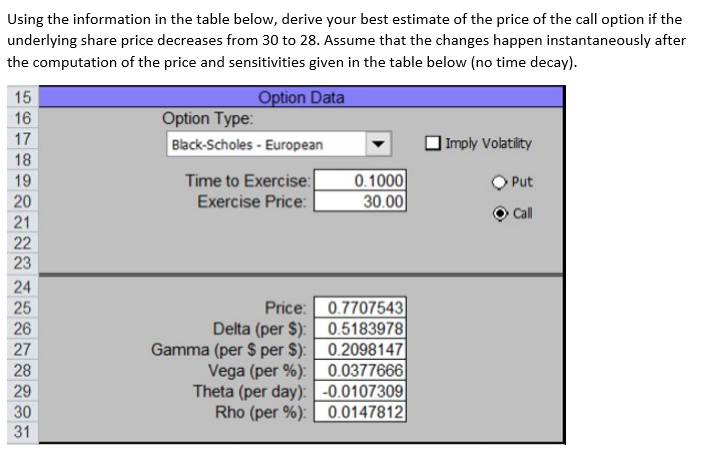

19 Using the information in the table below, derive your best estimate of the price of the call option if the underlying share price decreases from 30 to 28. Assume that the changes happen instantaneously after the computation of the price and sensitivities given in the table below (no time decay). 15 Option Data 16 Option Type: 17 Black-Scholes - European Imply Volatility 18 Time to Exercise: 0.1000 Put 20 Exercise Price: 30.00 Call 21 22 23 24 25 Price: 0.7707543 26 Delta (per $): 0.5183978 27 Gamma (per $ per $): 0.2098147 28 Vega (per %): 0.0377666 29 Theta (per day): -0.0107309 30 Rho (per %): 0.0147812 31

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock