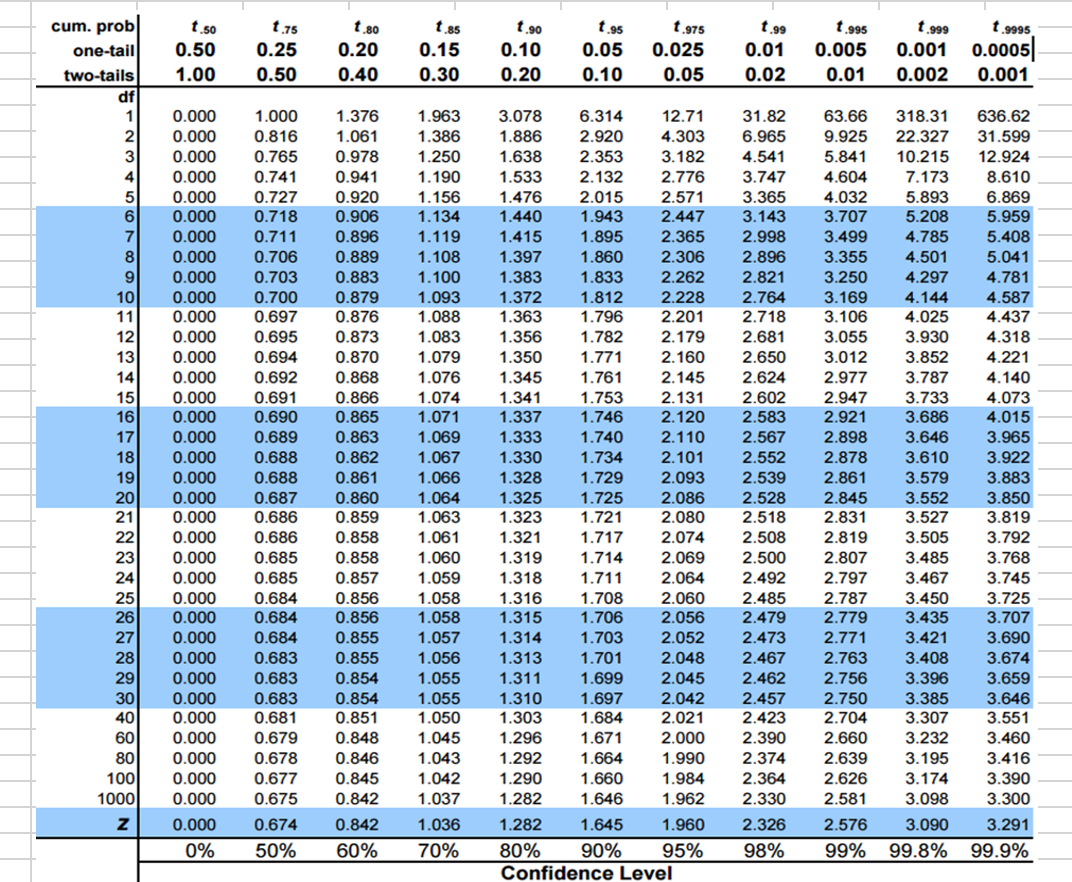

Question: 1.Based on the information ratios calculated in #4 above, is the performance of A & B statistically significantly different from zero at the 95% and

1.Based on the information ratios calculated in #4 above, is the performance of A & B statistically significantly different from zero at the 95% and 99% significance levels?

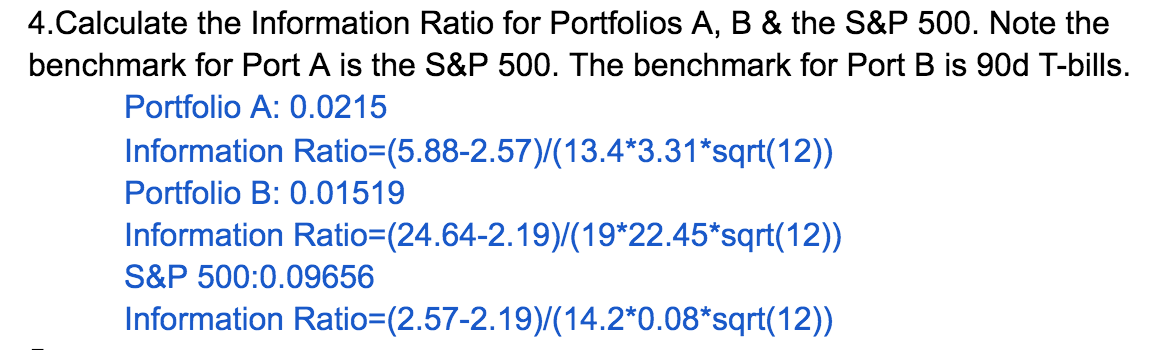

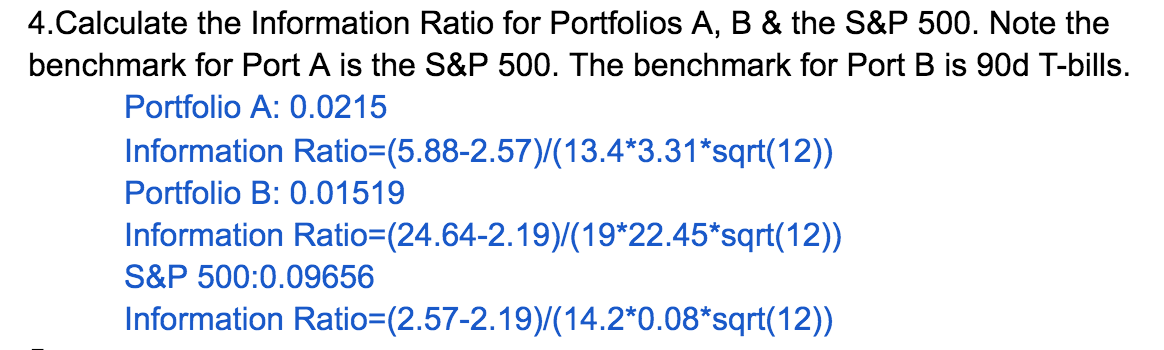

\f4. Calculate the Information Ratio for Portfolios A, B & the S&P 500. Note the benchmark for Port A is the S&P 500. The benchmark for Port B is 90d T-bills. Portfolio A: 0.0215 Information Ratio=(5.88-2.57)/(13.4*3.31*sqrt(12)) Portfolio B: 0.01519 Information Ratio=(24.64-2.19)/(19*22.45*sqrt(12)) S&P 500:0.09656 Information Ratio=(2.57-2.19)/(14.2*0.08*sqrt(12))

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock