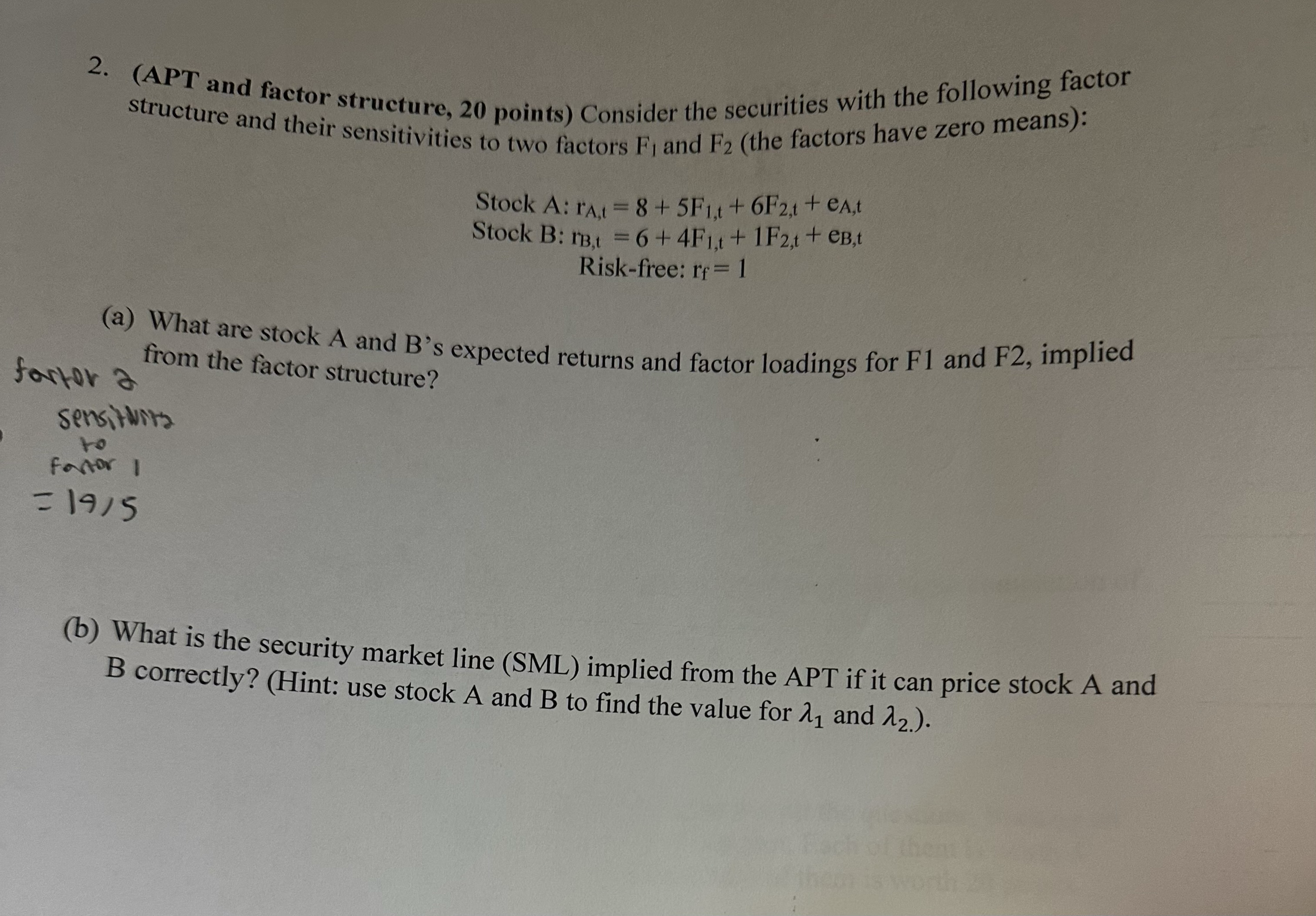

Question: 2. (APT and factor structure, 20 points) Consider the securities with the following factor structure and their sensitivities to two factors F1 and F2

2. (APT and factor structure, 20 points) Consider the securities with the following factor structure and their sensitivities to two factors F1 and F2 (the factors have zero means): Stock A: rA = 8+5F1.t+6F21+ CA,t Stock B: TB, = 6 + 4F1,t + 1F2,t + CB,t Risk-free: rf=1 (a) What are stock A and B's expected returns and factor loadings for F1 and F2, implied from the factor structure? forter a sensitivity to factor I = 19/5 (b) What is the security market line (SML) implied from the APT if it can price stock A and B correctly? (Hint: use stock A and B to find the value for and 2.).

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock