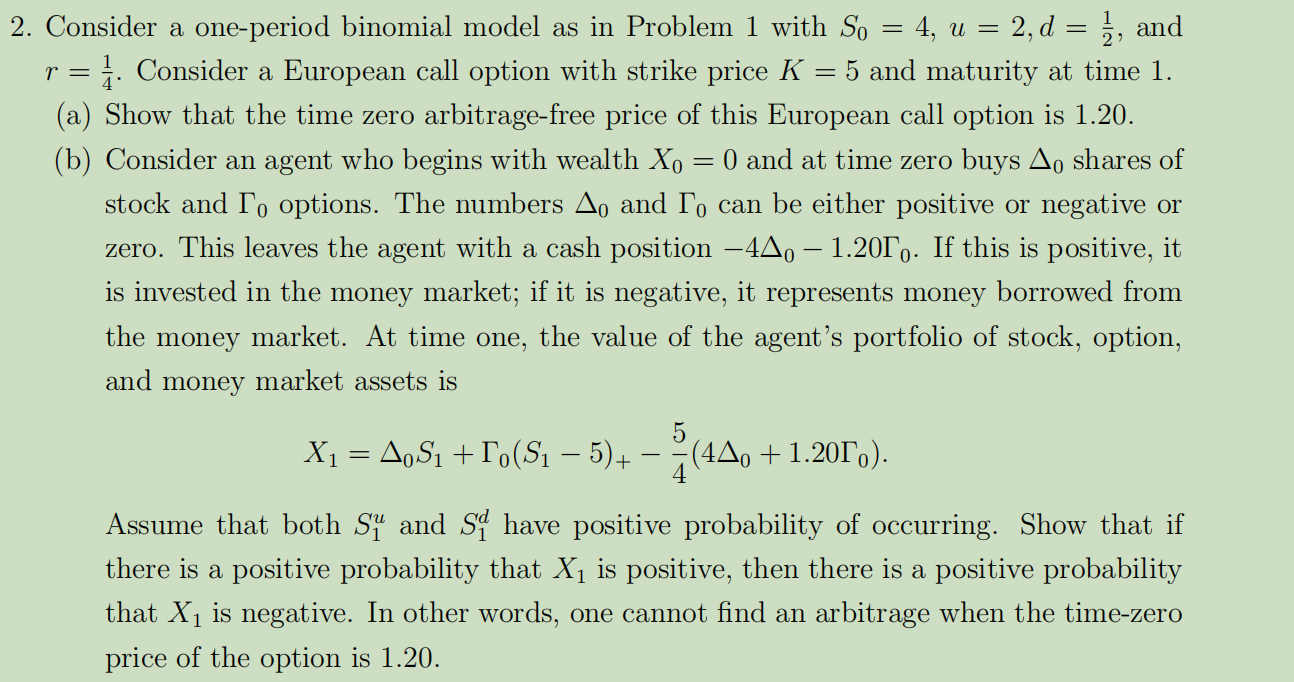

Question: 2. Consider a one-period binomial model as in Problem 1 with SD = 4, u = 2,d = l and 2: 'r = i. Consider

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts