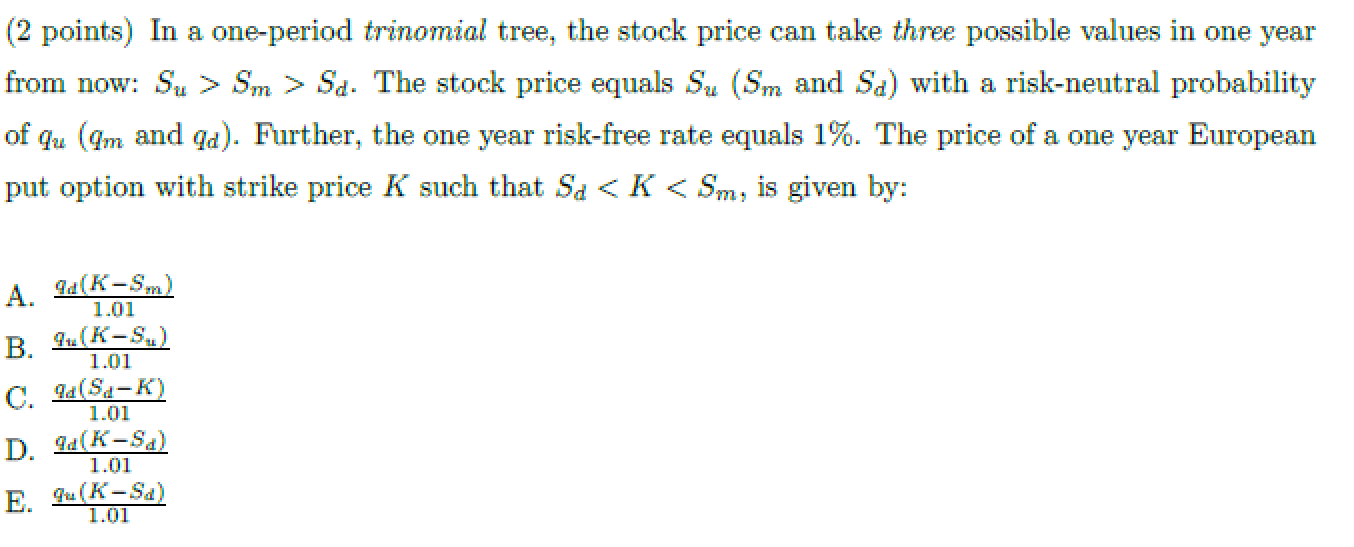

Question: ( 2 points ) In a one - period trinomial tree, the stock price can take three possible values in one year from now: S

points In a oneperiod trinomial tree, the stock price can take three possible values in one year

from now: The stock price equals and : with a riskneutral probability

of and Further, the one year riskfree rate equals The price of a one year European

put option with strike price such that given :

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock