Question: 2. This question tests your understanding of binomial option pricing. The current price of a stock is $100. The tree is given below. The monthly

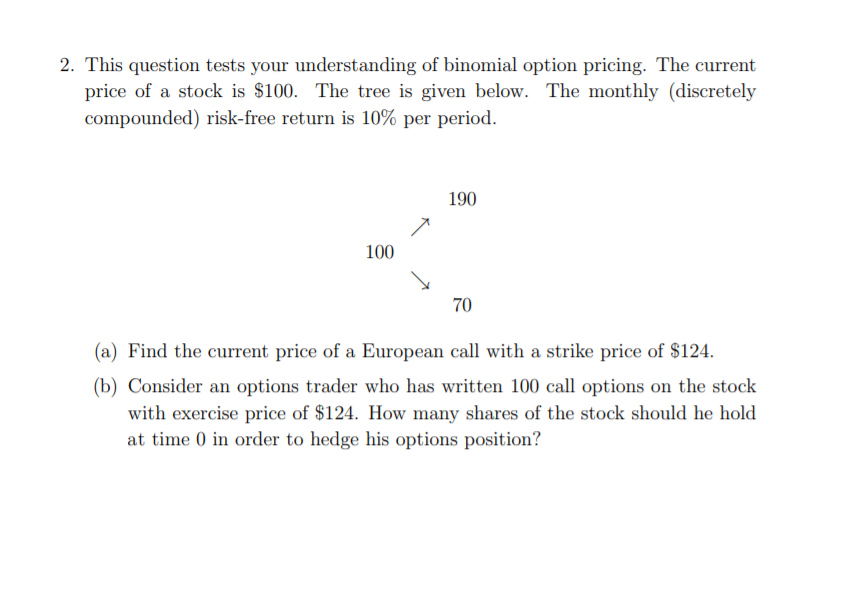

2. This question tests your understanding of binomial option pricing. The current price of a stock is $100. The tree is given below. The monthly (discretely compounded) risk-free return is 10% per period. 190 100 70 (a) Find the current price of a European call with a strike price of $124. (b) Consider an options trader who has written 100 call options on the stock with exercise price of $124. How many shares of the stock should he hold at time 0 in order to hedge his options position

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock