The names of the Taxpayers are Willis A. Turner and Irene F The letter advising the...

Fantastic news! We've Found the answer you've been seeking!

Transcribed Image Text:

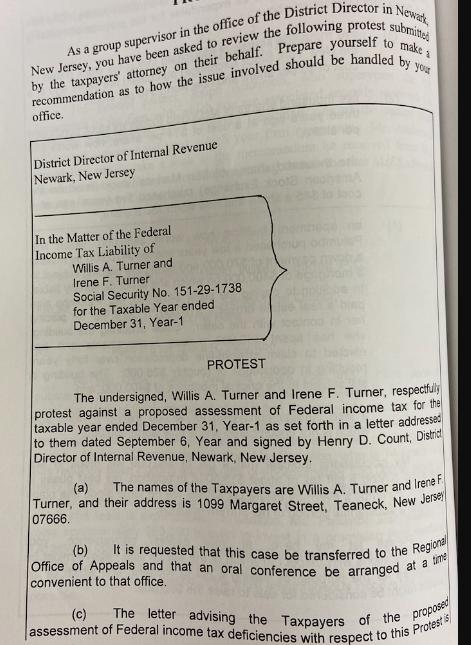

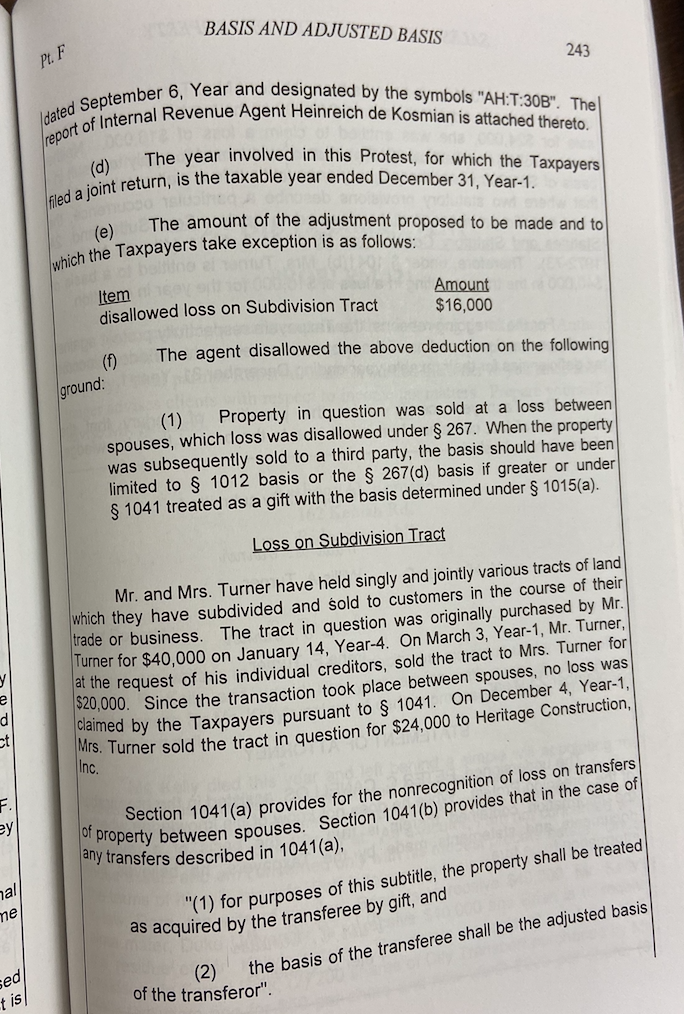

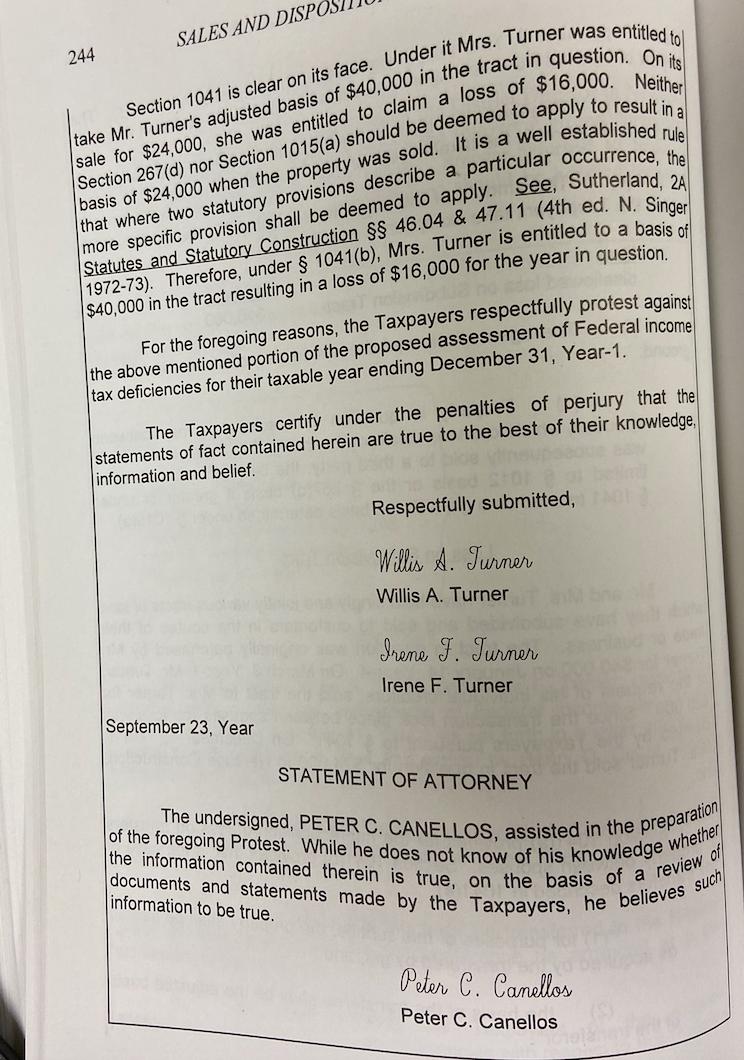

The names of the Taxpayers are Willis A. Turner and Irene F The letter advising the Taxpayers of the proposed Turner, and their address is 1099 Margaret Street, Teaneck, New Jersey It is requested that this case be transferred to the Regional office. District Director of Internal Revenue Newark, New Jersey In the Matter of the Federal Income Tax Liability of Willis A. Turner and Irene F. Turner Social Security No. 151-29-1738 for the Taxable Year ended December 31, Year-1 PROTEST The undersigned, Willis A. Turner and Irene F. Turner, respectfuly protest against a proposed assessment of Federal income tax for the taxable year ended December 31, Year-1 as set forth in a letter addressed to them dated September 6, Year and signed by Henry D. Count, Distic Director of Internal Revenue, Newark, New Jersey. (a) 07666. (b) Office of Appeals and that an oral conference be arranged at convenient to that office. (c) /dated September 6, Year and designated by the symbols "AH:T:30B". The BASIS AND ADJUSTED BASIS Pt. F 243 The year involved in this Protest, for which the Taxpayers (d) The amount of the adjustment proposed to be made and to (е) hich the Taxpayers take exception is as follows: beltn Item e disallowed loss on Subdivision Tract Amount $16,000 (f) The agent disallowed the above deduction on the following ground: (1) Property in question was sold at a loss between spouses, which loss was disallowed under § 267. When the property was subsequently sold to a third party, the basis should have been limited to § 1012 basis or the § 267(d) basis if greater or under $ 1041 treated as a gift with the basis determined under § 1015(a). Loss on Subdivision Tract Mr. and Mrs. Turner have held singly and jointly various tracts of land which they have subdivided and sold to customers in the course of their trade or business. The tract in question was originally purchased by Mr. Turner for $40,000 on January 14, Year-4. On March 3, Year-1, Mr. Turner, at the request of his individual creditors, sold the tract to Mrs. Turner for S20,000. Since the transaction took place between spouses, no loss was cialmed by the Taxpayers pursuant to § 1041. On December 4, Year-1, MIS. Turner sold the tract in question for $24,000 to Heritage Construction, d Inc. F. ey Section 1041(a) provides for the nonrecognition of loss on transfers of any transfers described in 1041(a), nal me "(1) for purposes of this subtitle, the property shall be treated as acquired by the transferee by gift, and sed t is (2) of the transferor". the basis of the transferee shall be the adjusted basis The undersigned, PETER C. CANELLOS, assisted in the preparation the information contained therein is true, on the basis of a review of documents and statements made by the Taxpayers, he believes such of the foregoing Protest. While he does not know of his knowledge whether SALES AND DISPO 244 more specific provision shall be deemed to apply. See, Sutherland Statutes and Statutory Construction §§ 46.04 & 47.11 (4th ed. N S A 1972-73). Therefore, under § 1041(b), Mrs. Turner is entitled to a basis ed $40,000 in the tract resulting in a loss of $16,000 for the year in question For the foregoing reasons, the Taxpayers respectfully protest against the above mentioned portion of the proposed assessment of Federal income tax deficiencies for their taxable year ending December 31, Year-1. The Taxpayers certify under the penalties of perjury that the statements of fact contained herein are true to the best of their knowledge, information and belief. Respectfully submitted, Willis A. Turner Willis A. Turner Irene F. Turner Irene F. Turner September 23, Year STATEMENT OF ATTORNEY information to be true. Peter C. Canellos Peter Canellos The names of the Taxpayers are Willis A. Turner and Irene F The letter advising the Taxpayers of the proposed Turner, and their address is 1099 Margaret Street, Teaneck, New Jersey It is requested that this case be transferred to the Regional office. District Director of Internal Revenue Newark, New Jersey In the Matter of the Federal Income Tax Liability of Willis A. Turner and Irene F. Turner Social Security No. 151-29-1738 for the Taxable Year ended December 31, Year-1 PROTEST The undersigned, Willis A. Turner and Irene F. Turner, respectfuly protest against a proposed assessment of Federal income tax for the taxable year ended December 31, Year-1 as set forth in a letter addressed to them dated September 6, Year and signed by Henry D. Count, Distic Director of Internal Revenue, Newark, New Jersey. (a) 07666. (b) Office of Appeals and that an oral conference be arranged at convenient to that office. (c) /dated September 6, Year and designated by the symbols "AH:T:30B". The BASIS AND ADJUSTED BASIS Pt. F 243 The year involved in this Protest, for which the Taxpayers (d) The amount of the adjustment proposed to be made and to (е) hich the Taxpayers take exception is as follows: beltn Item e disallowed loss on Subdivision Tract Amount $16,000 (f) The agent disallowed the above deduction on the following ground: (1) Property in question was sold at a loss between spouses, which loss was disallowed under § 267. When the property was subsequently sold to a third party, the basis should have been limited to § 1012 basis or the § 267(d) basis if greater or under $ 1041 treated as a gift with the basis determined under § 1015(a). Loss on Subdivision Tract Mr. and Mrs. Turner have held singly and jointly various tracts of land which they have subdivided and sold to customers in the course of their trade or business. The tract in question was originally purchased by Mr. Turner for $40,000 on January 14, Year-4. On March 3, Year-1, Mr. Turner, at the request of his individual creditors, sold the tract to Mrs. Turner for S20,000. Since the transaction took place between spouses, no loss was cialmed by the Taxpayers pursuant to § 1041. On December 4, Year-1, MIS. Turner sold the tract in question for $24,000 to Heritage Construction, d Inc. F. ey Section 1041(a) provides for the nonrecognition of loss on transfers of any transfers described in 1041(a), nal me "(1) for purposes of this subtitle, the property shall be treated as acquired by the transferee by gift, and sed t is (2) of the transferor". the basis of the transferee shall be the adjusted basis The undersigned, PETER C. CANELLOS, assisted in the preparation the information contained therein is true, on the basis of a review of documents and statements made by the Taxpayers, he believes such of the foregoing Protest. While he does not know of his knowledge whether SALES AND DISPO 244 more specific provision shall be deemed to apply. See, Sutherland Statutes and Statutory Construction §§ 46.04 & 47.11 (4th ed. N S A 1972-73). Therefore, under § 1041(b), Mrs. Turner is entitled to a basis ed $40,000 in the tract resulting in a loss of $16,000 for the year in question For the foregoing reasons, the Taxpayers respectfully protest against the above mentioned portion of the proposed assessment of Federal income tax deficiencies for their taxable year ending December 31, Year-1. The Taxpayers certify under the penalties of perjury that the statements of fact contained herein are true to the best of their knowledge, information and belief. Respectfully submitted, Willis A. Turner Willis A. Turner Irene F. Turner Irene F. Turner September 23, Year STATEMENT OF ATTORNEY information to be true. Peter C. Canellos Peter Canellos

Expert Answer:

Related Book For

Accounting Principles

ISBN: 978-0470533475

9th Edition

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso

Posted Date:

Students also viewed these accounting questions

-

On January 1. Ruiz Company issued bonds as follows: Face Value: Number of Years: Stated Interest Rate: Interest payments per year 500,000 15 7% Required: 1) Calculate the bond selling price given the...

-

E and F are vector fields given by E = 2xax + ay + yzaz and F = xyax y2ay+ xyzaz. Determine: (a) |E| a t (l, 2, 3) (b) The component of E along F at (1, 2, 3) (c) A vector perpendicular to both E...

-

D & E are equal partners and are closing their drawing accounts on December 31. Each partner had withdrawn $75,000. The correct entry to close their drawing accounts would be a credit to D...

-

Power Company acquired 80 percent of Solar Company's outstanding common stock for $200,000 cash on January 2, 2021. The two companies continued to operate as separate entities after the combination....

-

A 10-year note for $1200, bearing interest at 6% compounded monthly, is discounted at 8% compounded quarterly 3 years, 10 months after the date of issue. Find the proceeds of the note.

-

From the perspective of institutional investors, what are the pros and cons of investing in VC funds?

-

Troubleshooting charts are an excellent tool and should be used in what context?

-

Imax Corporation is a large entertainment technology company, with headquarters in New York and Toronto, and theatres worldwide. Its share price, which was as high as Can.$ 13.89 on the Toronto Stock...

-

In the context of solid-phase extraction (SPE), what are the key factors that influence the selection of stationary phase materials, and how do these factors affect the selectivity and capacity of...

-

You have just been hired as a brand manager at Kelsey-White, an American multinational consumer goods company. Recently the firm invested in the development of K-W Vision, a series of systems and...

-

For inviscid adiabatic flow, prove the relation 1 Dp p Dt in two ways: =-.u 1. by combining the energy and continuity equations; 2. by applying the isentropic relation p = const to a fluid element...

-

If you were examining a sequence of chromosomal DNA, what characteristics would cause you to believe that the sequence contained a transposable element?

-

Meiotic nondisjunction usually occurs during meiosis I. What is not separating properly: bivalents or sister chromatids? What is not separating properly during mitotic nondisjunction?

-

What is meant by the term DNA sequence?

-

Describe how bases interact with each other in the double helix. This description should include the concepts of complementarity, hydrogen bonding, and base stacking.

-

Which of the following terms should not be used to describe a human with three copies of chromosome 12? A. Polyploid B. Triploid C. Aneuploid D. Euploid E. 2n + 1 F. Trisomy 12

-

Jenny's Novelties sells souvenir key chains at the local airport. JN sells these key chains at $12 each. The Variable Cost per chain is $8 and the Total Fixed Costs for teh year amounts to $13,000....

-

Don Griffin worked as an accountant at a local accounting firm for five years after graduating from university. Recently, he opened his own accounting practice, which he operates as a corporation....

-

At Hutchingson Company, checks are not prenumbered because both the purchasing agent and the treasurer are authorized to issue checks. Each signer has access to unissued checks kept in an unlocked...

-

Identify which control activity is violated in each of the following situations, and explain how the situation creates an opportunity for fraud or inappropriate accounting practices. 1. Once a month...

-

Two types of present value tables may be used with the discounted cash flow technique. Identify the tables and the circumstance(s) when each table should be used.

-

Verify that the log-likelihood of model (7.7) is \(\sum_{i=1}^{k}\left[n_{i} \lambda-\exp (\lambda) ight]\). (a) Compute MLE of \(\lambda\). (b) Compute the Pearson chi-square statistic and compare...

-

Think about the general concept of a relationship, not necessarily in a business setting, but just relationships in general between any two parties. What aspects of relationships are inherently...

-

Has transactional selling gone the way of the dinosaur? That is, are there ever any situations in which a transactional approach to selling would be an appropriate approach today? If so, what are...

Study smarter with the SolutionInn App