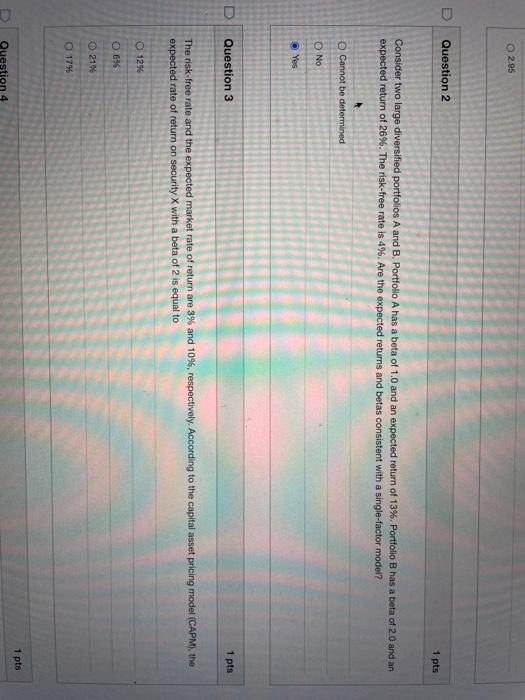

Question: 2.95 D Question 2 1 pts Consider two large diversified portfolios A and B. Portfolio A has a beta of 1.0 and an expected return

2.95 D Question 2 1 pts Consider two large diversified portfolios A and B. Portfolio A has a beta of 1.0 and an expected return of 13%. Portfolio B has a beta of 2.0 and an expected return of 26%. The risk-free rate is 4%. Are the expected returns and betas consistent with a single-factor model? O Cannot be determined No Yes Question 3 1 pts The risk-free rate and the expected market rate of return are 3% and 10%, respectively. According to the capital asset pricing model (CAPM), the expected rate of return on security X with a beta of 2 is equal to O 1296 O 6% 21% 17% 1 pts Question 4

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock