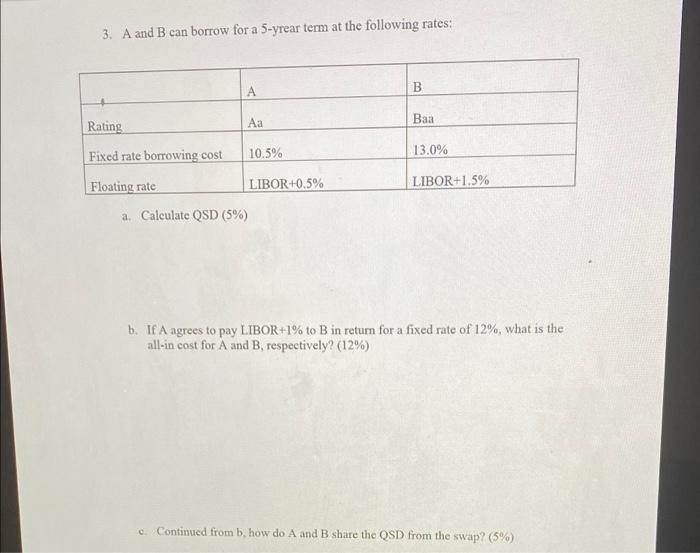

Question: 3. A and B can borrow for a 5-yrear term at the following rates: Rating Fixed rate borrowing cost Floating rate A Aa 10.5% a.

3. A and B can borrow for a 5-yrear term at the following rates: Rating Fixed rate borrowing cost Floating rate A Aa 10.5% a. Calculate QSD (5%) LIBOR+0.5% B Baa 13.0% LIBOR+1.5% b. If A agrees to pay LIBOR+1% to B in return for a fixed rate of 12%, what is the all-in cost for A and B, respectively? (12%) c. Continued from b, how do A and B share the QSD from the swap? (5%)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock