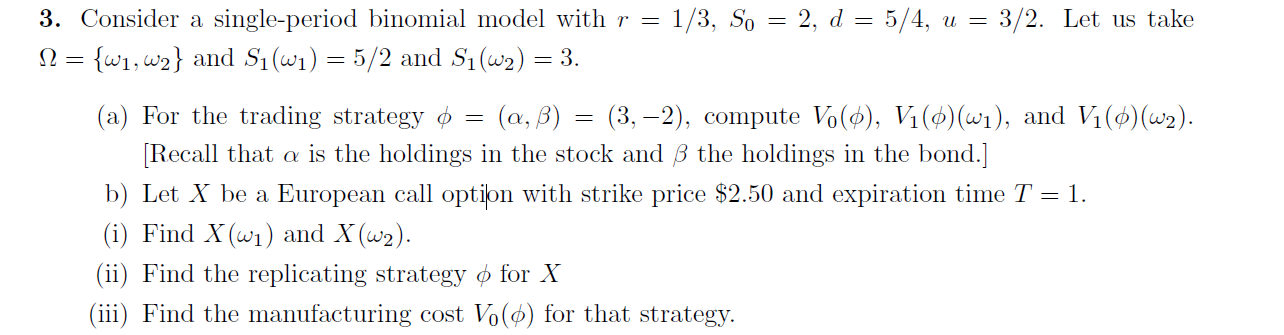

Question: 3. Consider a single-period binomial model with r = 1/3, So = 2, d = 5/4, u = 3/2. Let us take N = {w1,w2}

3. Consider a single-period binomial model with r = 1/3, So = 2, d = 5/4, u = 3/2. Let us take N = {w1,w2} and S(wi) = 5/2 and Si(w2) = 3. (a) For the trading strategy o = (a,b) = (3,-2), compute Vo(d), Vi(0)(wi), and Vi(0)(w2). (Recall that a is the holdings in the stock and the holdings in the bond.] b) Let X be a European call option with strike price $2.50 and expiration time T = 1. (i) Find X(wi) and X(w2). (ii) Find the replicating strategy o for X (iii) Find the manufacturing cost V.(d) for that strategy. 3. Consider a single-period binomial model with r = 1/3, So = 2, d = 5/4, u = 3/2. Let us take N = {w1,w2} and S(wi) = 5/2 and Si(w2) = 3. (a) For the trading strategy o = (a,b) = (3,-2), compute Vo(d), Vi(0)(wi), and Vi(0)(w2). (Recall that a is the holdings in the stock and the holdings in the bond.] b) Let X be a European call option with strike price $2.50 and expiration time T = 1. (i) Find X(wi) and X(w2). (ii) Find the replicating strategy o for X (iii) Find the manufacturing cost V.(d) for that strategy

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts