Question: 3 . Consider an option on a stock ( A B C ) that pays no dividend. The option has the following characteristics:

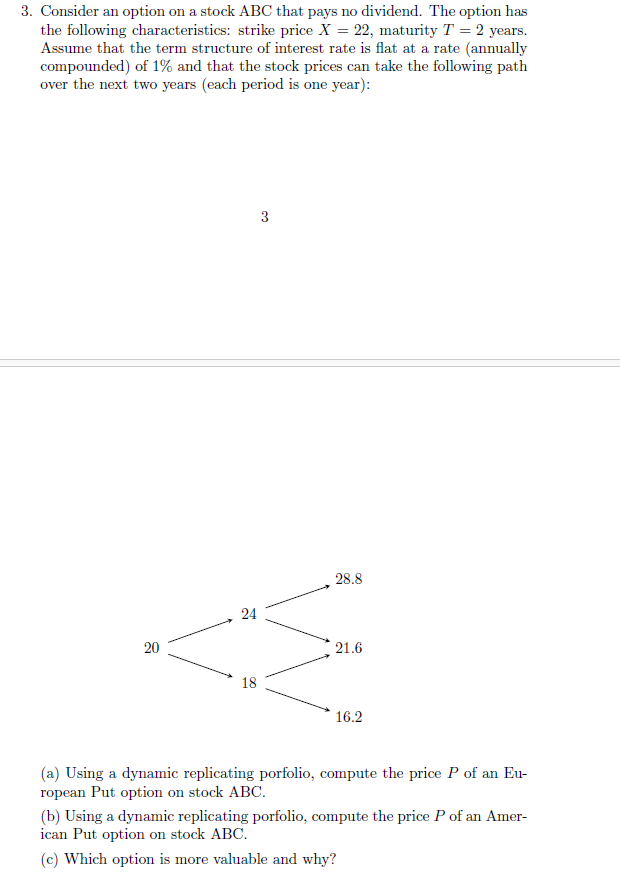

Consider an option on a stock A B C that pays no dividend. The option has the following characteristics: strike price X maturity T years. Assume that the term structure of interest rate is flat at a rate annually compounded of and that the stock prices can take the following path over the next two years each period is one year:

a Using a dynamic replicating porfolio, compute the price P of an European Put option on stock ABC

b Using a dynamic replicating porfolio, compute the price P of an American Put option on stock ABC

c Which option is more valuable and why?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock