Question: 3. (Implications for asset prices) In this question we consider the special case of the asset- pricing model derived in Topic 4 where the stochastic

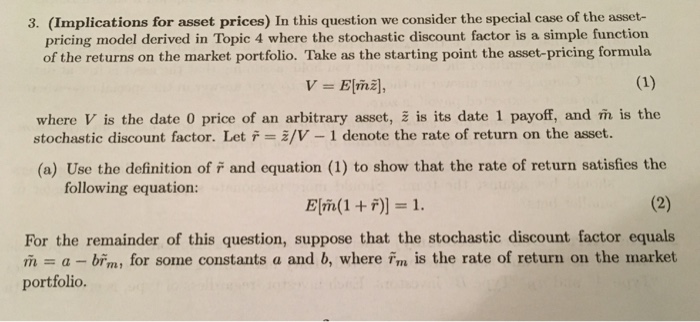

3. (Implications for asset prices) In this question we consider the special case of the asset- pricing model derived in Topic 4 where the stochastic discount factor is a simple function of the returns on the market portfolio. Take as the starting point the asset-pricing formula where V is the date 0 price of an arbitrary asset, is its date 1 payoff, and h is the stochastic discount factor. Let r = z/V-1 denote the rate of return on the asset. (a) Use the definition of r and equation (1) to show that the rate of return satisfies the following equation: For the remainder of this question, suppose that the stochastic discount factor equals ma -brm, for some constants a and b, where im is the rate of return on the market portfolio. 3. (Implications for asset prices) In this question we consider the special case of the asset- pricing model derived in Topic 4 where the stochastic discount factor is a simple function of the returns on the market portfolio. Take as the starting point the asset-pricing formula where V is the date 0 price of an arbitrary asset, is its date 1 payoff, and h is the stochastic discount factor. Let r = z/V-1 denote the rate of return on the asset. (a) Use the definition of r and equation (1) to show that the rate of return satisfies the following equation: For the remainder of this question, suppose that the stochastic discount factor equals ma -brm, for some constants a and b, where im is the rate of return on the market portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts