Question: 3. Now, we form a portfolio with two assets. Both are risky asset. How can we get the return and the variance of this portfolio?

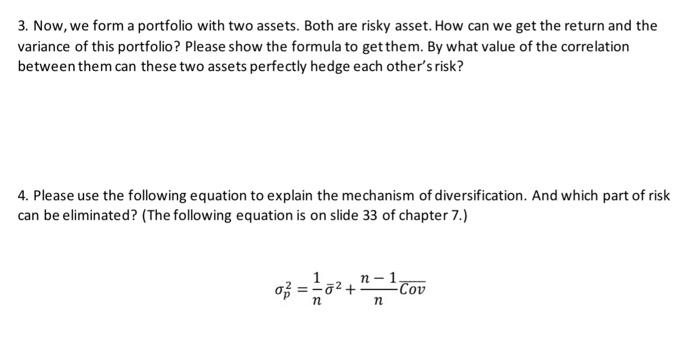

3. Now, we form a portfolio with two assets. Both are risky asset. How can we get the return and the variance of this portfolio? Please show the formula to get them. By what value of the correlation between them can these two assets perfectly hedge each other's risk? 4. Please use the following equation to explain the mechanism of diversification. And which part of risk can be eliminated? (The following equation is on slide 33 of chapter 7.) op n-1 72 + COV n n

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock